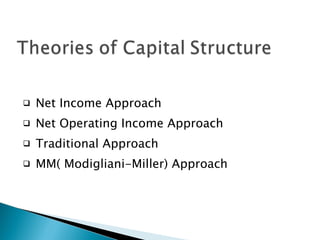

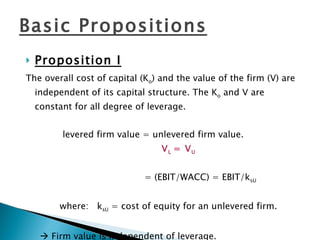

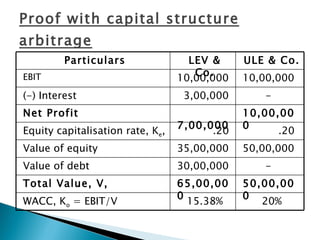

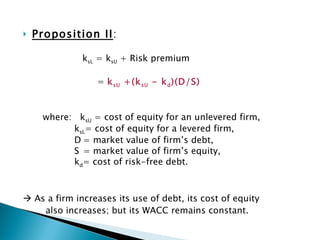

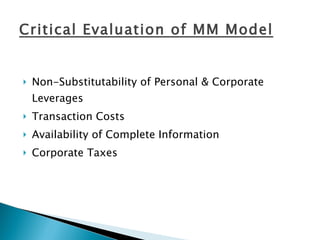

The document discusses different approaches to capital structure and the Modigliani-Miller model. It summarizes key assumptions of the MM model, including that capital markets are perfect, leverage at the personal and corporate level are substitutes, and there are no taxes or transaction costs. The MM model shows that firm value and cost of capital are independent of capital structure.