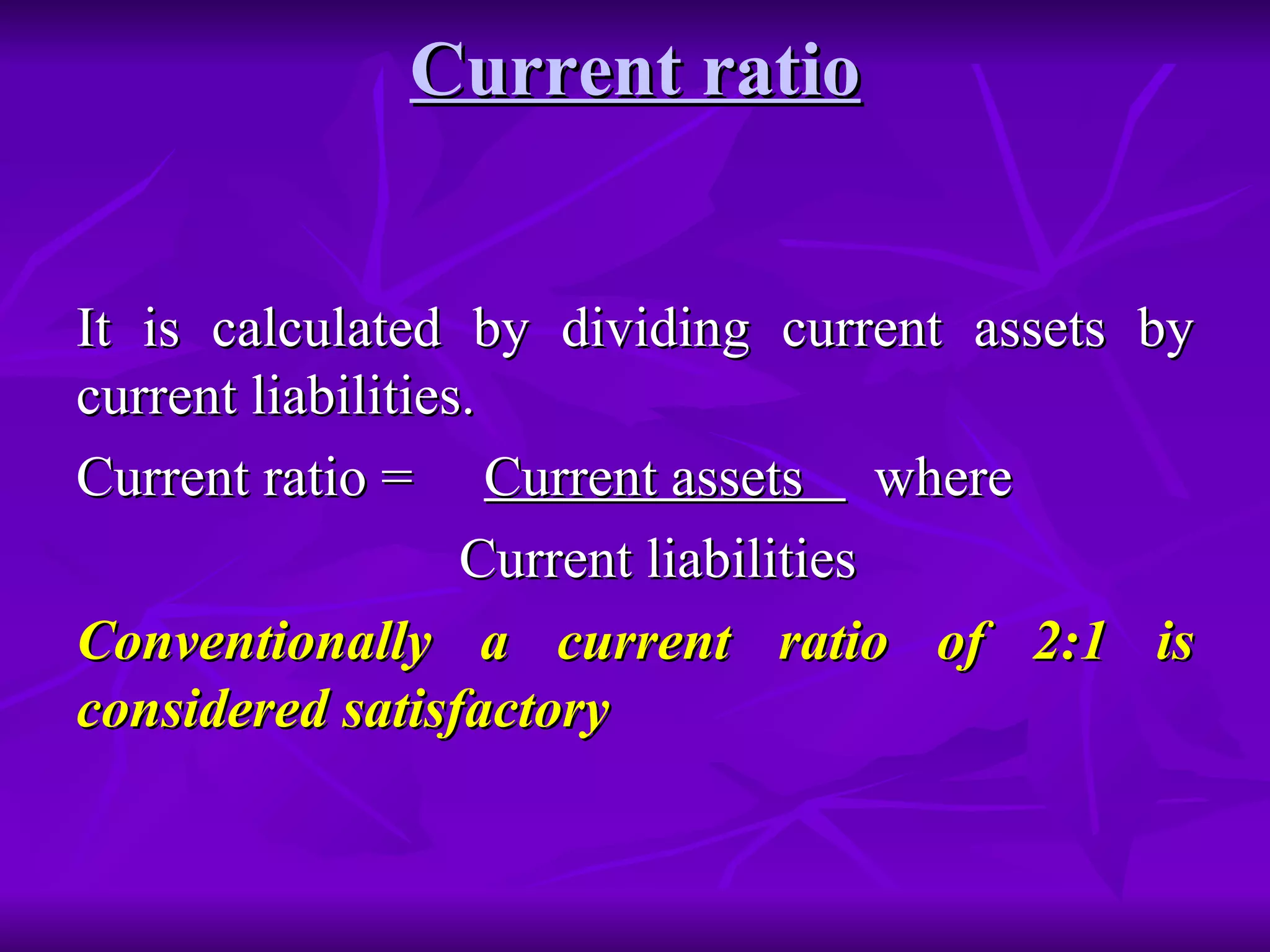

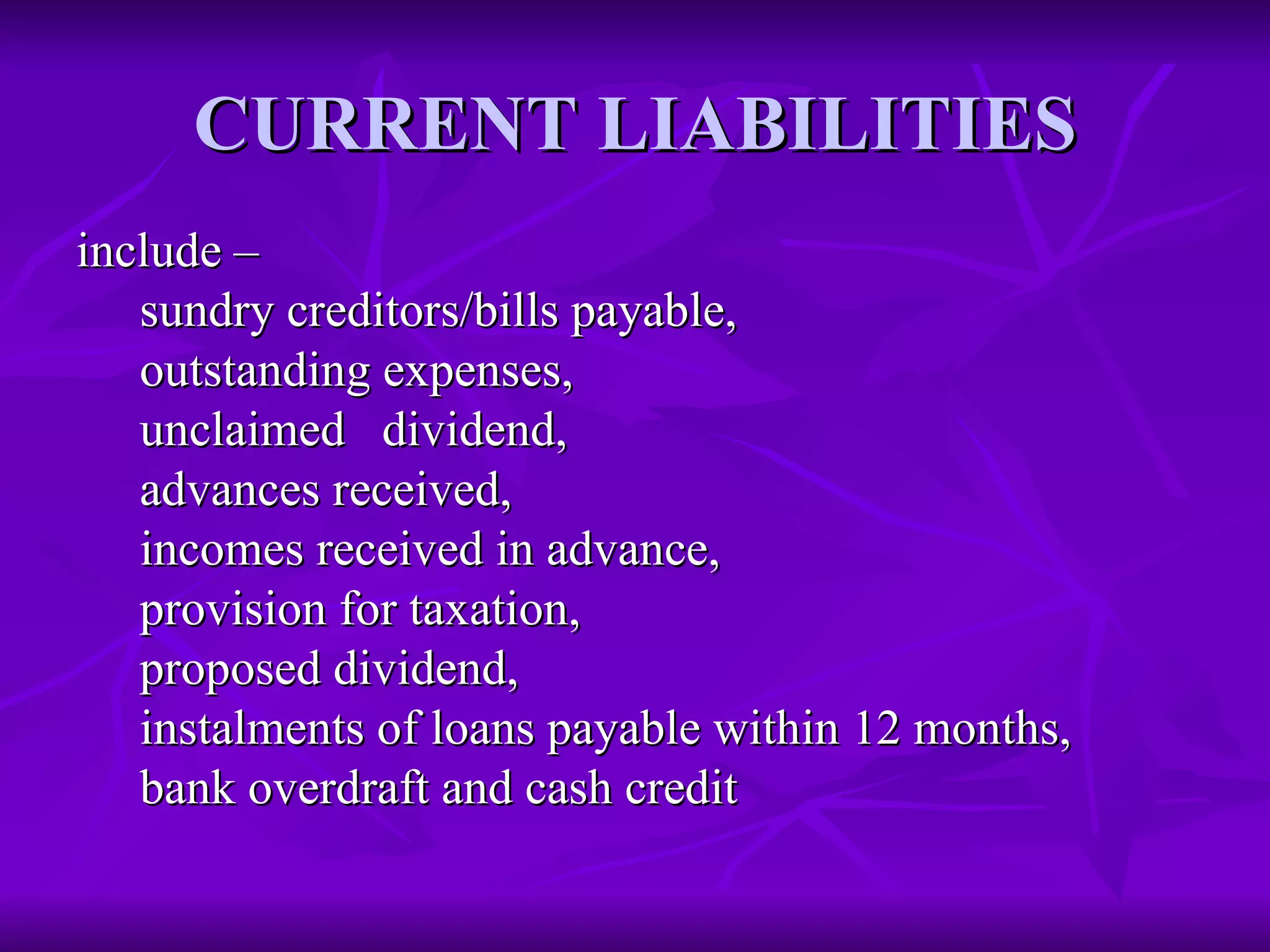

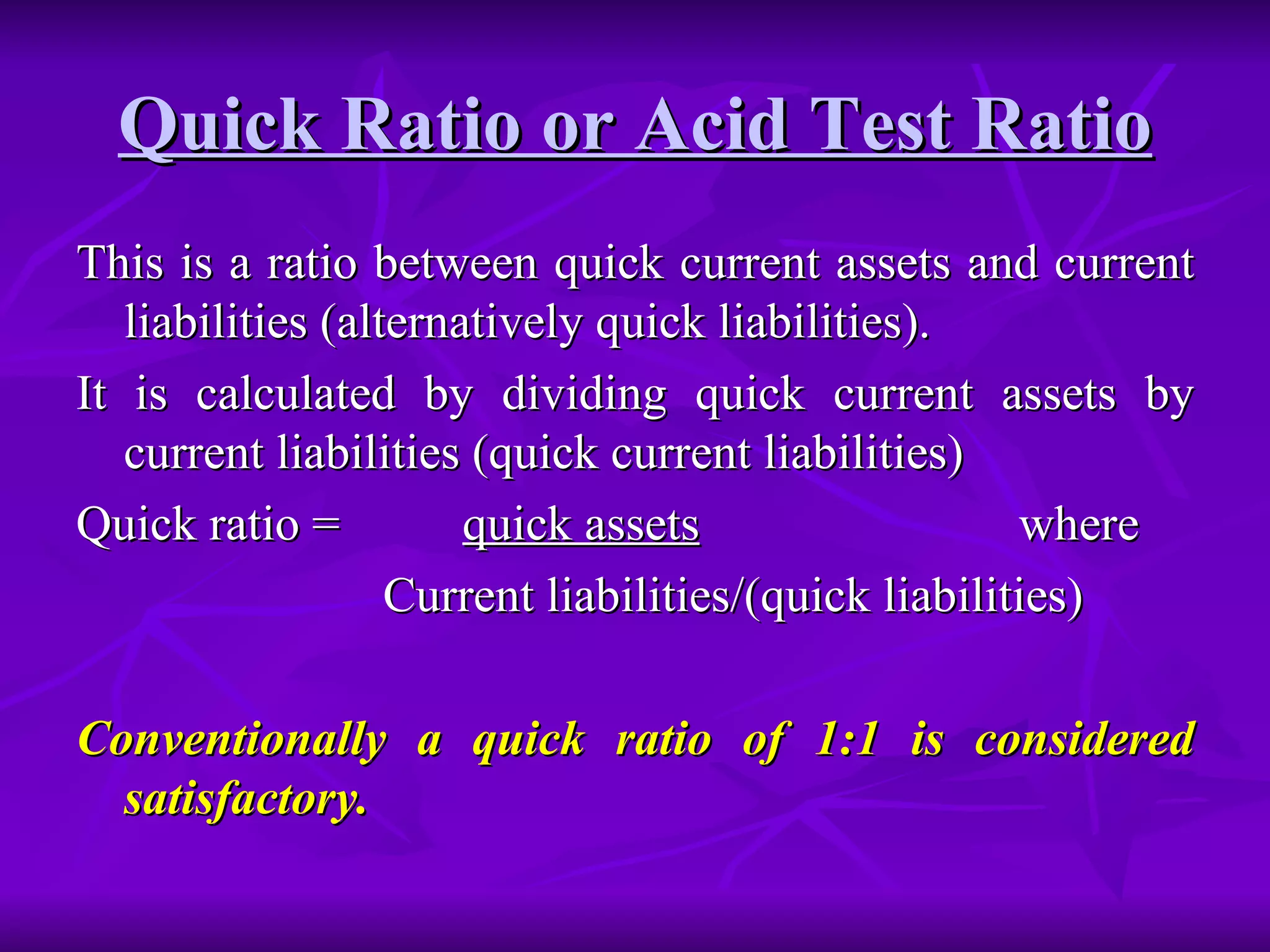

Ratio analysis involves calculating relationships between financial statement items to interpret a firm's financial condition and performance. Ratios can be classified into liquidity, capital structure, profitability, and activity ratios. Liquidity ratios measure short-term solvency, capital structure ratios measure long-term solvency, profitability ratios measure operating efficiency and returns, and activity ratios measure asset utilization and efficiency. Ratios are compared over time, against industry standards, or between firms to identify strengths, weaknesses, and trends.