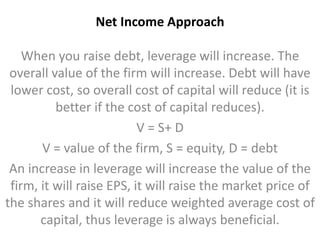

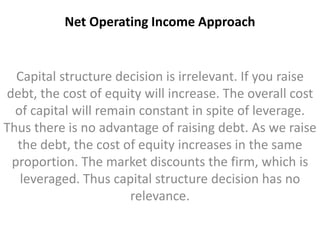

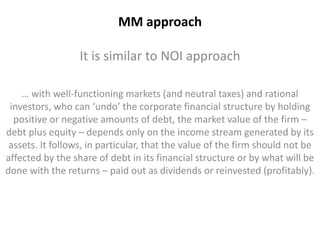

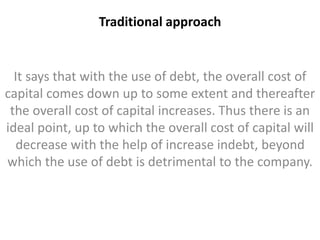

Capital structure refers to the combination of capital (equity, debt, preference shares) used to finance a company. There are various theories on how capital structure affects a company's value and cost of capital. The net income approach argues that leverage always increases value by lowering the overall cost of capital. The net operating income and MM approaches argue capital structure is irrelevant as the costs of equity and debt offset each other. The traditional approach finds an optimal capital structure that minimizes costs up to a point, after which more debt increases risks.