Downloaded 1,758 times

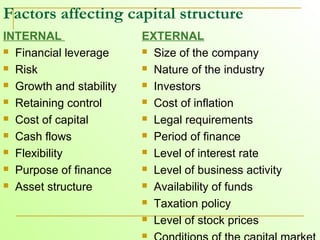

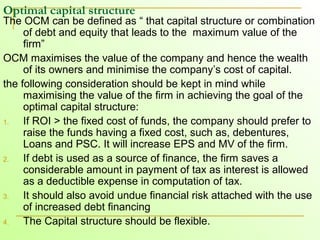

The capital structure of a company refers to the composition of its long-term financing, including loans, reserves, shares, and bonds. A company's capital structure is influenced by both internal factors like financial leverage, risk tolerance, and growth plans as well as external factors like industry norms, availability of funds, and tax policies. An optimal capital structure maximizes the value of the company by balancing the use of debt financing which increases earnings per share but also increases financial risk. The point of indifference is the earnings level at which earnings per share remains the same regardless of the debt-to-equity mix. Leverage refers to using fixed-cost funds to increase returns to owners, either through financial leverage of long-term debt or operating