Downloaded 32 times

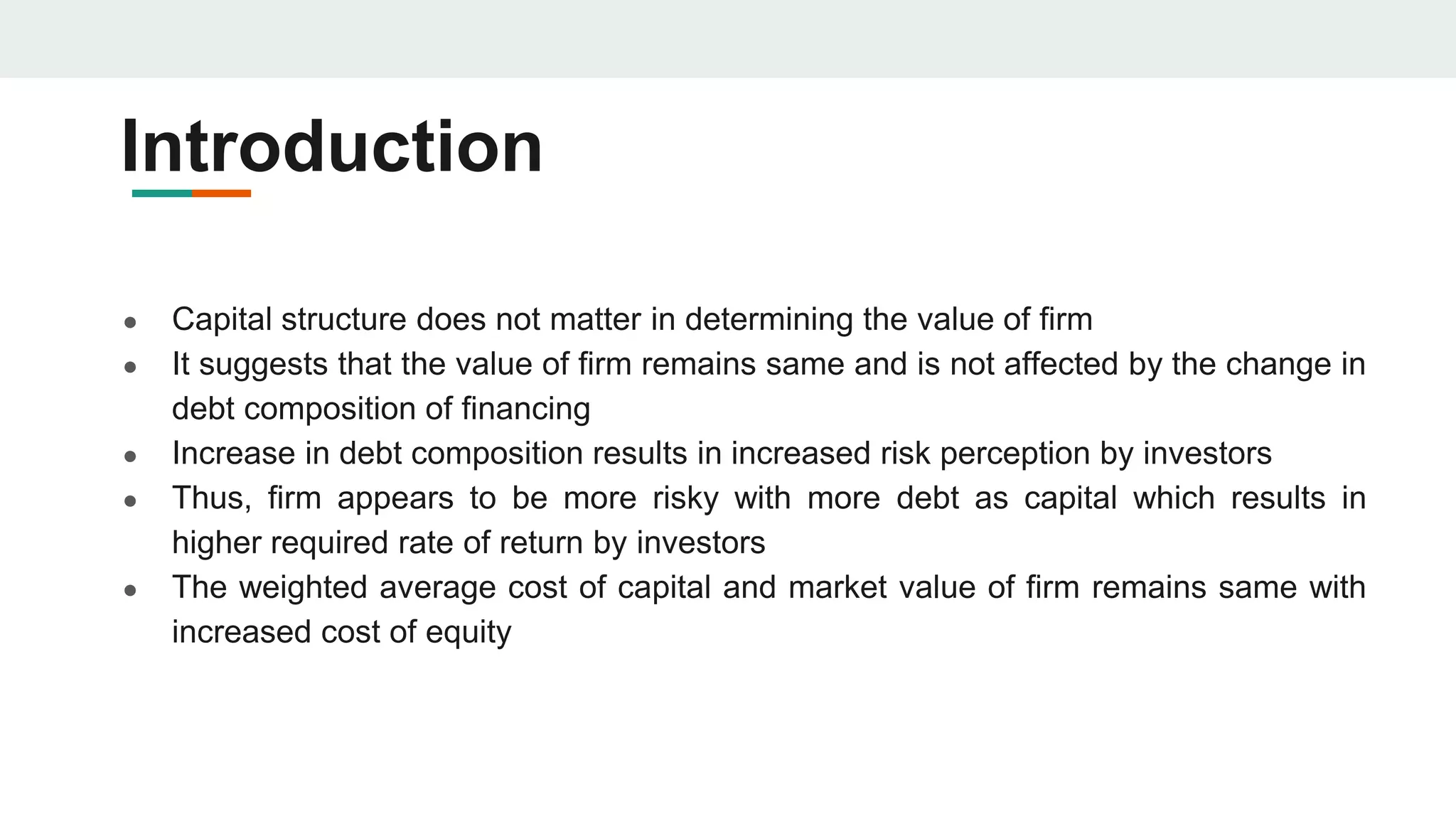

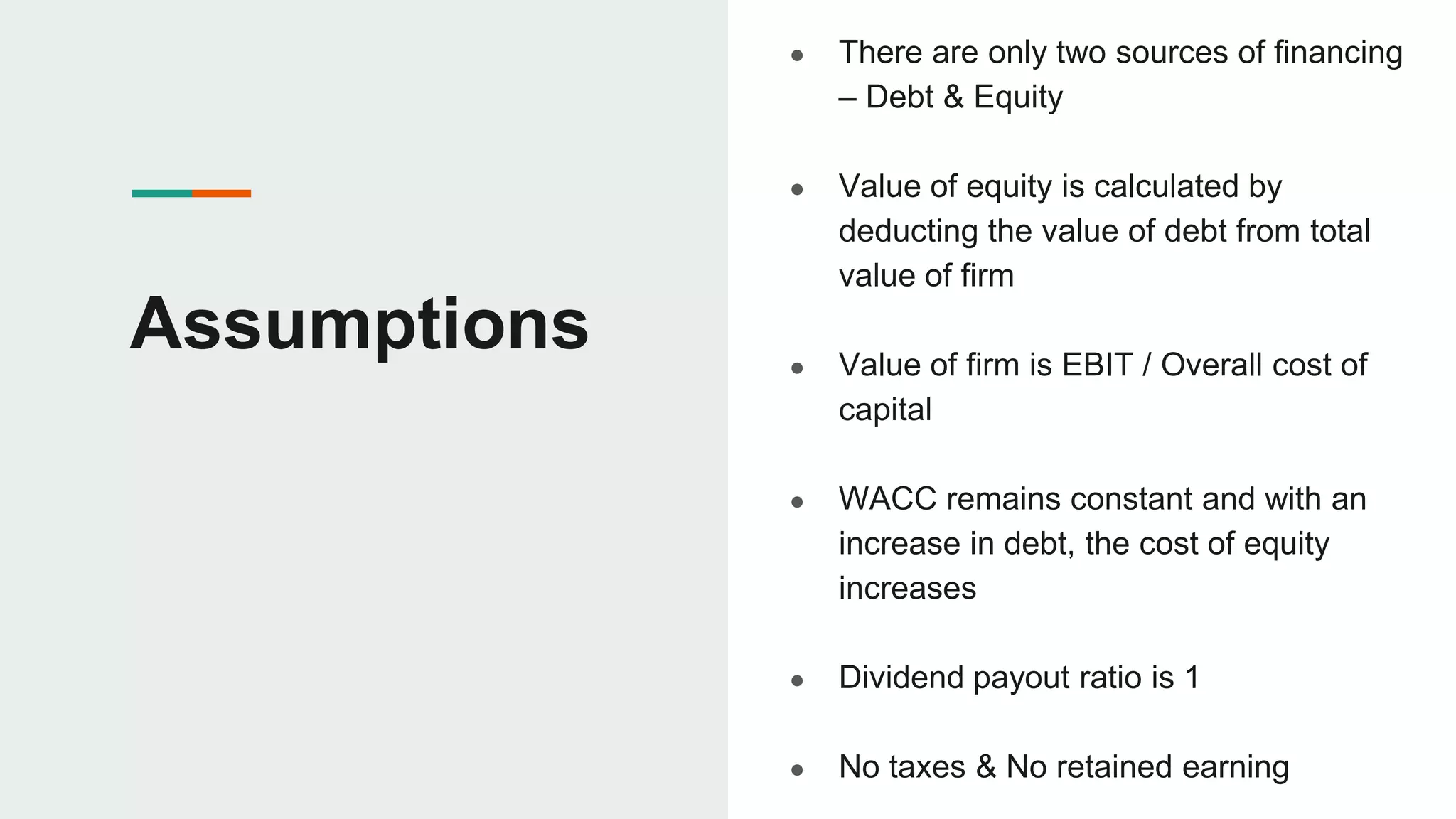

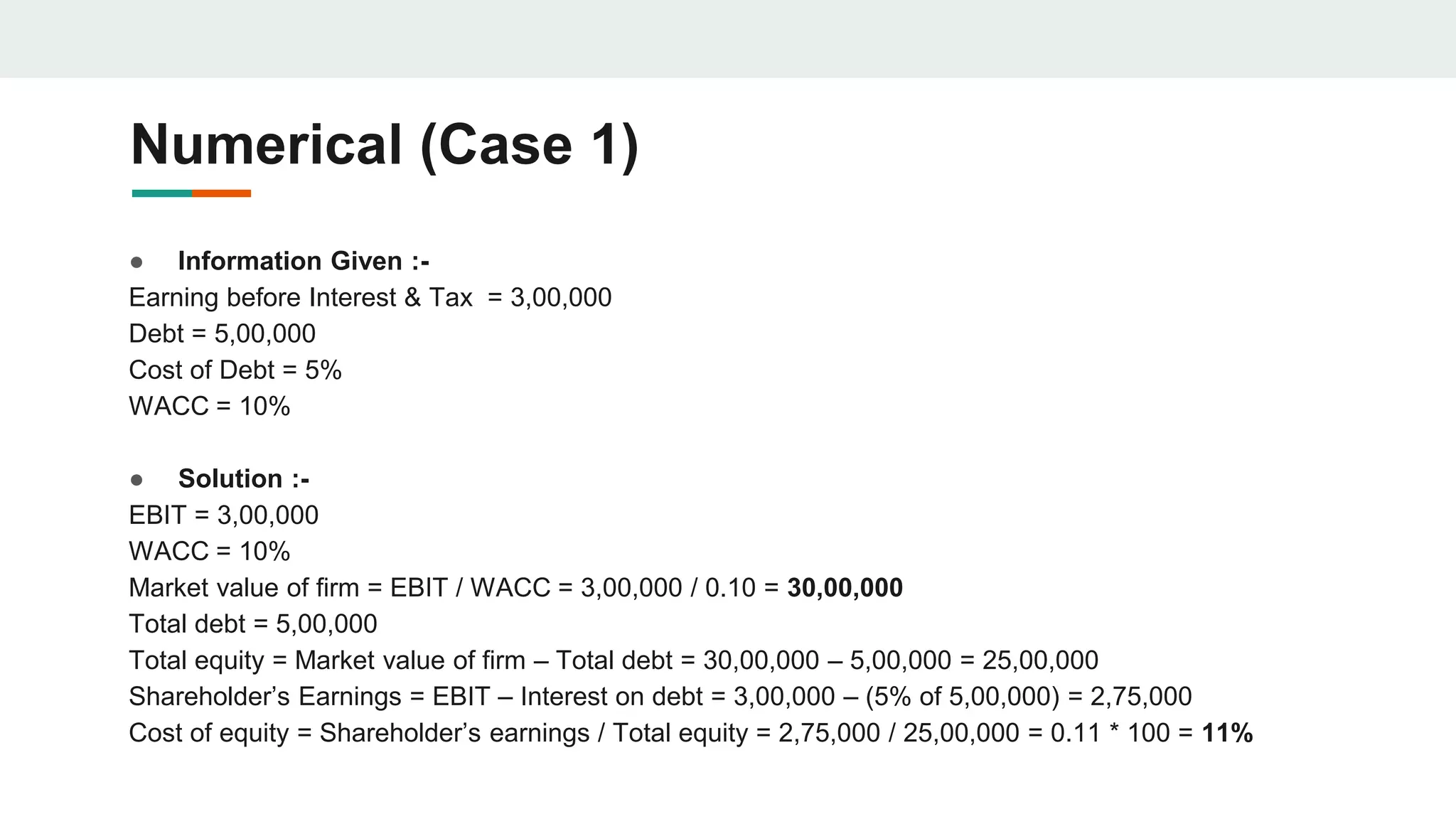

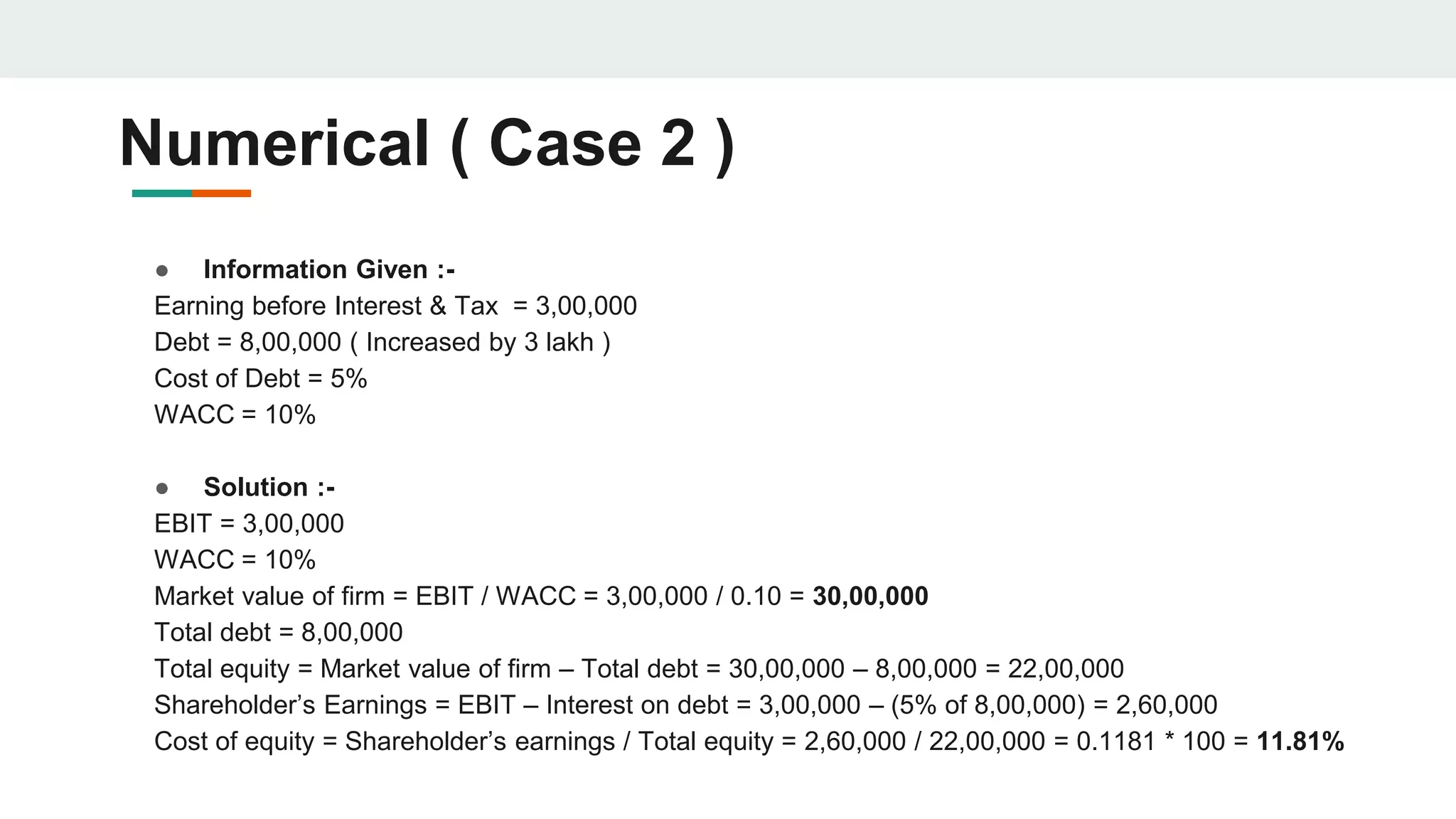

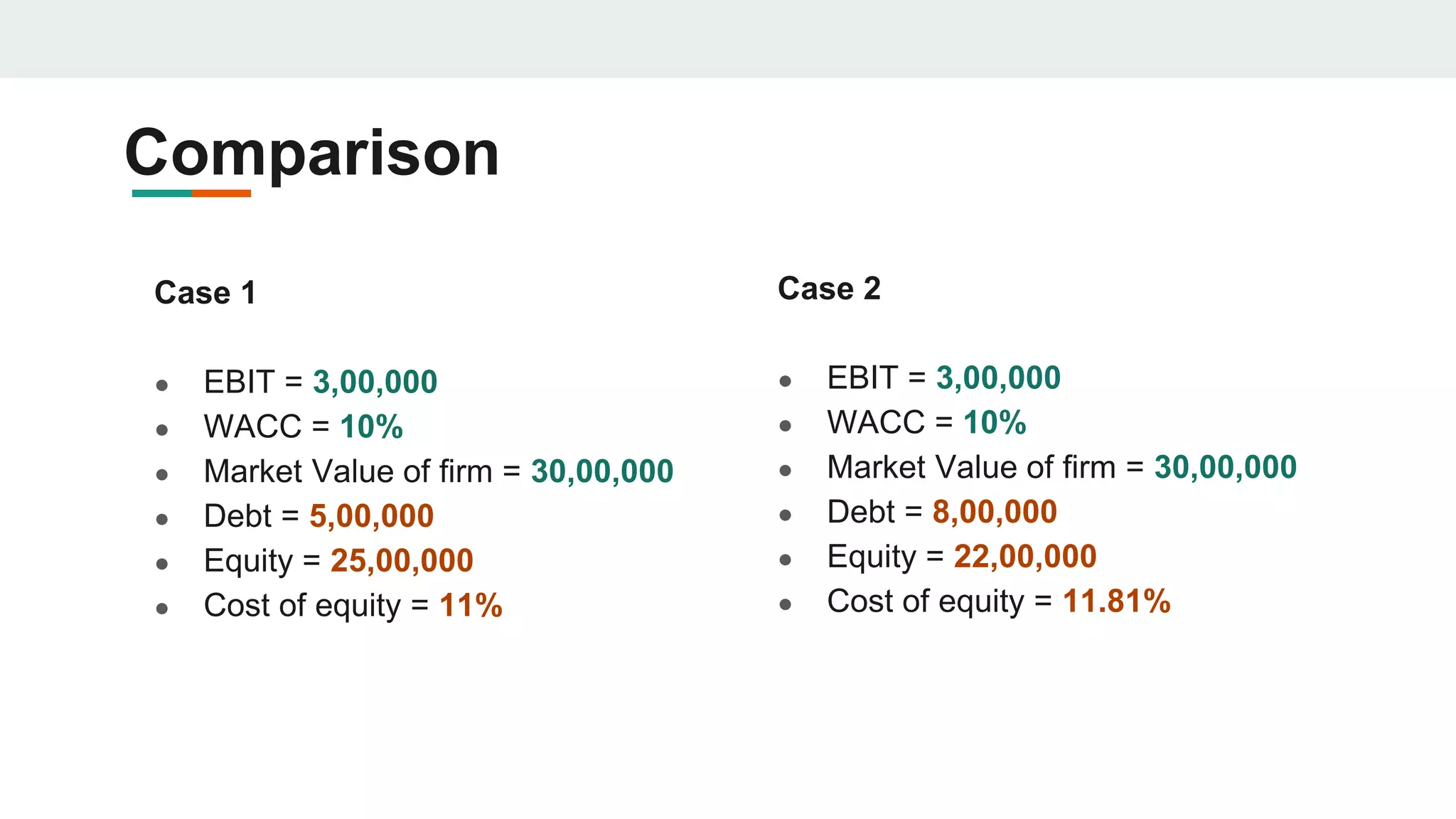

The document discusses capital structure theories, asserting that the value of a firm remains constant regardless of changes in debt composition, although increased debt raises investor risk perception and required returns. It provides numerical examples demonstrating the calculation of market value, total equity, and cost of equity under different debt scenarios, ultimately comparing two cases with varying debt levels. The analysis concludes that while total market value remains unchanged, the cost of equity increases with higher debt levels.