Downloaded 387 times

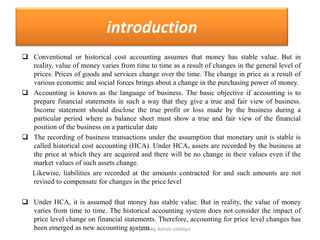

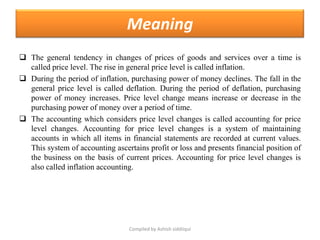

This document discusses accounting for price level changes. It explains that historical cost accounting assumes stable monetary values but prices actually change over time due to inflation and deflation. Accounting for price level changes considers how general, specific, and relative price changes impact financial statements. Shortcomings of historical cost accounting in inflationary periods are outlined. Suggested techniques to adjust for inflation include creating reserves, revaluing assets, using LIFO inventory valuation, and current value accounting.