Download to read offline

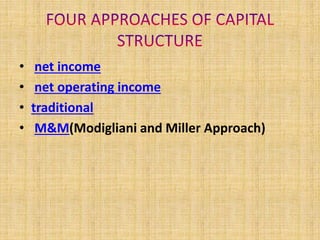

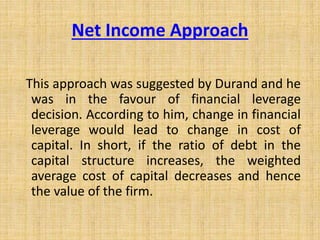

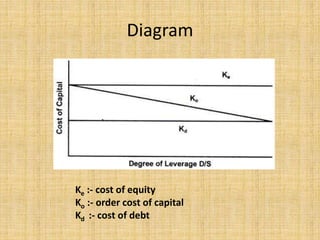

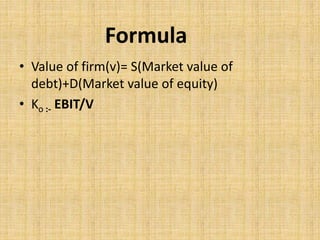

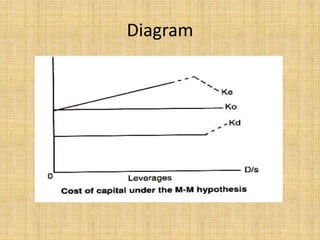

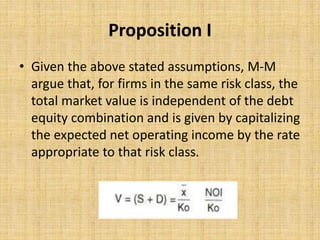

- Capital structure refers to the proportion of different types of capital (equity, debt, preference shares) that make up a company's total financing. It influences the value of a firm. - Three main approaches to capital structure are the net income approach, net operating income approach, and traditional approach. The Modigliani-Miller approach argues that the value and cost of capital of a firm are unaffected by its capital structure under certain assumptions. - The net income approach suggests that increasing debt lowers the weighted average cost of capital and increases firm value. The net operating income approach argues that leverage does not affect total firm value. The traditional approach proposes an optimal debt-equity mix that maximizes firm value.