Log your LOA pain with Pension Lab's brilliant campaign

Bhushan Steel

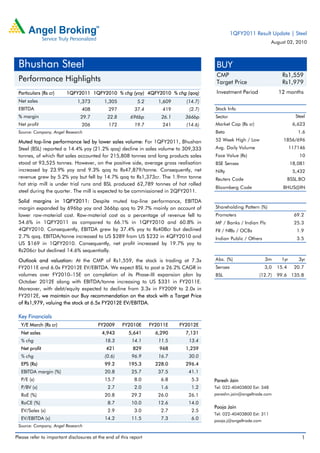

1. 1QFY2011 Result Update | Steel

August 02, 2010

Bhushan Steel BUY

CMP Rs1,559

Performance Highlights Target Price Rs1,979

Particulars (Rs cr) 1QFY2011 1QFY2010 % chg (yoy) 4QFY2010 % chg (qoq) Investment Period 12 months

Net sales 1,373 1,305 5.2 1,609 (14.7)

EBITDA 408 297 37.4 419 (2.7) Stock Info

% margin 29.7 22.8 696bp 26.1 366bp Sector Steel

Net profit 206 172 19.7 241 (14.6) Market Cap (Rs cr) 6,623

Source: Company, Angel Research Beta 1.6

Muted top-line performance led by lower sales volume: For 1QFY2011, Bhushan 52 Week High / Low 1856/696

Steel (BSL) reported a 14.4% yoy (21.2% qoq) decline in sales volume to 309,333 Avg. Daily Volume 117146

tonnes, of which flat sales accounted for 215,808 tonnes and long products sales Face Value (Rs) 10

stood at 93,525 tonnes. However, on the positive side, average gross realisation BSE Sensex 18,081

increased by 23.9% yoy and 9.3% qoq to Rs47,879/tonne. Consequently, net Nifty 5,432

revenue grew by 5.2% yoy but fell by 14.7% qoq to Rs1,373cr. The 1.9mn tonne Reuters Code BSSL.BO

hot strip mill is under trial runs and BSL produced 62,789 tonnes of hot rolled

Bloomberg Code BHUS@IN

steel during the quarter. The mill is expected to be commissioned in 2QFY2011.

Solid margins in 1QFY2011: Despite muted top-line performance, EBITDA

margin expanded by 696bp yoy and 366bp qoq to 29.7% mainly on account of Shareholding Pattern (%)

lower raw-material cost. Raw-material cost as a percentage of revenue fell to Promoters 69.2

54.6% in 1QFY2011 as compared to 66.1% in 1QFY2010 and 60.8% in MF / Banks / Indian Fls 25.3

4QFY2010. Consequently, EBITDA grew by 37.4% yoy to Rs408cr but declined FII / NRIs / OCBs 1.9

2.7% qoq. EBITDA/tonne increased to US $289 from US $232 in 4QFY2010 and Indian Public / Others 3.5

US $169 in 1QFY2010. Consequently, net profit increased by 19.7% yoy to

Rs206cr but declined 14.6% sequentially.

Outlook and valuation: At the CMP of Rs1,559, the stock is trading at 7.3x Abs. (%) 3m 1yr 3yr

FY2011E and 6.0x FY2012E EV/EBITDA. We expect BSL to post a 26.2% CAGR in Sensex 3,0 15.4 20.7

volumes over FY2010–15E on completion of its Phase-III expansion plan by BSL (12.7) 99.6 135.8

October 2012E along with EBITDA/tonne increasing to US $331 in FY2011E.

Moreover, with debt/equity expected to decline from 3.3x in FY2009 to 2.0x in

FY2012E, we maintain our Buy recommendation on the stock with a Target Price

of Rs1,979, valuing the stock at 6.5x FY2012E EV/EBITDA.

Key Financials

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net sales 4,943 5,641 6,290 7,131

% chg 18.3 14.1 11.5 13.4

Net profit 421 829 968 1,259

% chg (0.6) 96.9 16.7 30.0

EPS (Rs) 99.2 195.3 228.0 296.4

EBITDA margin (%) 20.8 25.7 37.5 41.1

P/E (x) 15.7 8.0 6.8 5.3 Paresh Jain

P/BV (x) 2.7 2.0 1.6 1.2 Tel: 022-40403800 Ext: 348

RoE (%) 20.8 29.2 26.0 26.1 pareshn.jain@angeltrade.com

RoCE (%) 8.7 10.0 12.6 14.0

Pooja Jain

EV/Sales (x) 2.9 3.0 2.7 2.5

Tel: 022-40403800 Ext: 311

EV/EBITDA (x) 14.2 11.5 7.3 6.0 pooja.j@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

4. Bhushan Steel | 1QFY2011 Result Update

Result highlights

Muted top-line performance led by lower sales volume

BSL’s sales volume declined by 14.4% yoy and 21.2% qoq to 309,333 tonnes, of

which flat sales accounted for 215,808 tonnes and long products sales stood at

93,525 tonnes. However, on the positive side, average gross realisation increased

by 23.9% yoy and 9.3% qoq to Rs47,879/tonne. Consequently, net revenue grew

by 5.2% yoy but fell by 14.7% qoq to Rs1,373cr. The 1.9mn tonne hot strip mill is

under trial runs and BSL produced 62,789 tonnes of hot rolled steel during the

quarter. The mill is expected to be commissioned in 2QFY2011.

Exhibit 5: Net revenue grew by 5.2% yoy

2,000 60

1,609

1,600 1,429 1,373 40

1,305 1,298

1,200

(Rs cr)

20

(%)

800

0

400

0 (20)

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Net revenue (RHS) yoy change (LHS)

Source: Company, Angel Research

EBITDA margin expands by 696bp yoy

Despite muted top-line performance, EBITDA margin expanded by 696bp yoy and

366bp qoq to 29.7% mainly on account of lower raw-material cost. Raw-material

cost as a percentage of revenue fell to 54.6% in 1QFY2011 as compared to

66.1% in 1QFY2010 and 60.8% in 4QFY2010. Consequently, EBITDA grew by

37.4% yoy to Rs408cr. EBITDA/tonne increased to US $289 from US $232 in

4QFY2010 and US $169 in 1QFY2010.

Exhibit 6: EBITDA margin expands by 696bp yoy Exhibit 7: EBITDA/tonne at US $289 in 1QFY2011

500 35 350

419 408

390 30 289

400 300

343

25 233 232

297 250

300 209

(US $/tonne)

20

(Rs cr)

200

(%)

169

200 15

150

10

100 100

5

0 0 50

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

0

EBITDA (RHS) EBITDA margin (LHS) 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Source: Company, Angel Research Source: Company, Angel Research

August 02, 2010 4

5. Bhushan Steel | 1QFY2011 Result Update

Net profit came in at Rs206cr

While interest expense increased by 60.4% yoy and 43.0% qoq to Rs79cr, interest

income fell by 82.8% yoy and 88.9% qoq to Rs6cr. Consequently, net profit

increased by 19.7% yoy to Rs206cr but declined 14.6% sequentially.

Exhibit 8: Net profit grew by 19.7% yoy in 1QFY2011

300 18

241

250 227 15

206

189

200 172 12

(Rs cr)

150 9

(%)

100 6

50 3

0 0

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Net profit (RHS) Net profit margin (LHS)

Source: Company, Angel Research

August 02, 2010 5

6. Bhushan Steel | 1QFY2011 Result Update

Investment rationale

Entering a new orbit

BSL has undertaken an expansion plan in Orissa to increase its foothold in the

industry. The project is being executed in three phases, with Phase-I already

commissioned in FY2007 and Phase-II being commissioned recently. Post the

completion of Phase-II, the company's primary steel-making capacity will increase

to 2.2mn tonnes. Moreover, with the commissioning of its new HR plant in

2QFY2011E, BSL is moving from being a steel converter to a leading primary

producer of steel, extending its presence in the steel value chain. Phase-III is

currently under execution and is expected to come on stream by 3QFY2013E. On

completion of Phase-III, BSL's primary capacity will increase to 4.7mn tonnes,

making it one of the leading steel producers.

Volume growth sweetened by increasing EBITDA/tonne

With the commissioning of BSL's Phase-III expansion plan, we expect sales volume

to grow at a 26.2% CAGR over FY2010–15E, much higher than its peers. Despite

BSL not being integrated, cost of production is expected to be low due to a) its

unique combination of BF-EAF technology to produce steel and b) lower

conversion costs. The usage of BF-EAF technology will result in lower coal costs.

Hence, we expect EBITDA to register a 42.3% CAGR over FY2010–12E through a

combination of BF-EAF technology and low conversion cost. Thus, BSL is expected

to earn EBITDA/tonne of US $331 in FY2011E and US $345 in FY2012E.

Exhibit 9: Volumes to grow at 26.2% CAGR (FY10-15E) Exhibit 10: EBITDA/tonne at US $331 in FY2011

5.0 120

400 Captive usage of HR to lower cost

4.0 Post Phase-III

90

expansion 300

(mn tonnes)

3.0

(US $/tonne)

60

(%)

2.0 200

30

1.0 100

0.0 0

FY10 FY11E FY12E FY13E FY14E FY15E 0

FY06 FY09 FY12E FY15E

Sales Volume (LHS) Volume growth (RHS)

Source: Company, Angel Research Source: Company, Angel Research

Top supplier of niche auto-grade products

Over the years, BSL has been shifting its customer base from the trade segment to

OEMs/exports. We believe growing investments by foreign OEMs and the strategic

alliance with Sumitomo Metal will complement the company’s OEM relationships

and will likely help BSL mitigate demand risks.

August 02, 2010 6

7. Bhushan Steel | 1QFY2011 Result Update

Outlook and Valuation

At the CMP of Rs1,559, the stock is trading at 7.3x FY2011E and 6.0x FY2012E

EV/EBITDA. We expect BSL to register a 26.2% CAGR in volumes over

FY2010–15E on completion of its Phase-III expansion plan by October 2012 along

with EBITDA/tonne increasing to US $331 in FY2011E. Moreover, with debt/equity

expected to decline from 3.3x in FY2009 to 2.0x in FY2012E, we maintain our Buy

recommendation on the stock with a Target Price of Rs1,979, valuing the stock at

6.5x FY2012E EV/EBITDA. At our target price, the stock would trade at 1.2x EV/IC.

Exhibit 11: Key assumptions

Key assumptions FY11E FY12E

Revenue/tonne (Rs) 39,696 37,786

Sales volume (mn tonnes) 1.6 1.9

Source: Angel Research

Exhibit 12: EV/EBITDA band

45,000

17x

40,000

35,000 14x

30,000

11x

25,000

(Rs cr)

20,000 8x

15,000

5x

10,000

5,000

0

Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

Source: Bloomberg, Angel Research

Exhibit 13: P/E band

4,500

17x

4,000

3,500

3,000 12x

2,500

(Rs)

2,000

7x

1,500

1,000

500 2x

0

Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

Source: Bloomberg, Angel Research

August 02, 2010 7

13. Bhushan Steel | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Bhushan Steel

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

August 02, 2010 13