1. 1QFY2011 Result Update | Metals

August 2, 2010

Sarda Energy and Minerals ACCUMULATE

CMP Rs260

Performance highlights Target Price Rs290

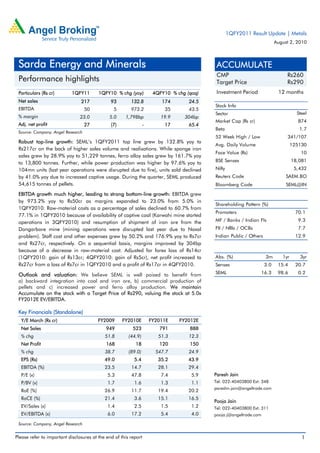

Particulars (Rs cr) 1QFY11 1QFY10 % chg (yoy) 4QFY10 % chg (qoq) Investment Period 12 months

Net sales 217 93 132.8 174 24.5

Stock Info

EBITDA 50 5 973.2 35 43.5

Sector Steel

% margin 23.0 5.0 1,798bp 19.9 304bp

Market Cap (Rs cr) 874

Adj. net profit 27 (7) - 17 65.4

Beta 1.7

Source: Company, Angel Research

52 Week High / Low 341/107

Robust top-line growth: SEML’s 1QFY2011 top line grew by 132.8% yoy to

Avg. Daily Volume 125130

Rs217cr on the back of higher sales volume and realisations. While sponge iron

Face Value (Rs) 10

sales grew by 28.9% yoy to 51,229 tonnes, ferro alloy sales grew by 161.7% yoy

BSE Sensex 18,081

to 13,800 tonnes. Further, while power production was higher by 97.6% yoy to

104mn units (last year operations were disrupted due to fire), units sold declined Nifty 5,432

by 41.0% yoy due to increased captive usage. During the quarter, SEML produced Reuters Code SAEM.BO

54,615 tonnes of pellets. Bloomberg Code SEML@IN

EBITDA growth much higher, leading to strong bottom-line growth: EBITDA grew

by 973.2% yoy to Rs50cr as margins expanded to 23.0% from 5.0% in

Shareholding Pattern (%)

1QFY2010. Raw-material costs as a percentage of sales declined to 60.7% from

Promoters 70.1

77.1% in 1QFY2010 because of availability of captive coal (Karwahi mine started

operations in 3QFY2010) and resumption of shipment of iron ore from the MF / Banks / Indian Fls 9.3

Dongarbore mine (mining operations were disrupted last year due to Naxal FII / NRIs / OCBs 7.7

problem). Staff cost and other expenses grew by 50.2% and 176.9% yoy to Rs7cr Indian Public / Others 12.9

and Rs27cr, respectively. On a sequential basis, margins improved by 304bp

because of a decrease in raw-material cost. Adjusted for forex loss of Rs14cr

(1QFY2010: gain of Rs13cr; 4QFY2010: gain of Rs5cr), net profit increased to Abs. (%) 3m 1yr 3yr

Rs27cr from a loss of Rs7cr in 1QFY2010 and a profit of Rs17cr in 4QFY2010. Sensex 3.0 15.4 20.7

Outlook and valuation: We believe SEML is well poised to benefit from SEML 16.3 98.6 0.2

a) backward integration into coal and iron ore, b) commercial production of

pellets and c) increased power and ferro alloy production. We maintain

Accumulate on the stock with a Target Price of Rs290, valuing the stock at 5.0x

FY2012E EV/EBITDA.

Key Financials (Standalone)

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 949 523 791 888

% chg 51.8 (44.9) 51.3 12.3

Net Profit 168 18 120 150

% chg 38.7 (89.0) 547.7 24.9

EPS (Rs) 49.0 5.4 35.2 43.9

EBITDA (%) 23.5 14.7 28.1 29.4

P/E (x) 5.3 47.8 7.4 5.9 Paresh Jain

P/BV (x) 1.7 1.6 1.3 1.1 Tel: 022-40403800 Ext: 348

pareshn.jain@angeltrade.com

RoE (%) 26.9 11.7 19.4 20.2

RoCE (%) 21.4 3.6 15.1 16.5

Pooja Jain

EV/Sales (x) 1.4 2.5 1.5 1.2 Tel: 022-40403800 Ext: 311

EV/EBITDA (x) 6.0 17.2 5.4 4.0 pooja.j@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Sarda Energy | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 performance (Standalone)

Y/E March (Rs cr) 1QFY11 1QFY10 yoy % FY10 FY09 yoy %

Net sales 217 93 132.8 523 949 (44.9)

Raw material 131 72 83.3 369 618 (40.3)

% of net sales 60.7 77.1 70.6 65.1

Power & Fuel 1 2 (52.5) 4 5 (16.1)

% of net sales 0.4 2.1 0.8 0.6

Staff cost 7 5 50.2 19 17 12.5

% of net sales 3.5 5.4 3.7 1.8

Other expenditure 27 10 176.9 53 86 (37.7)

% of net sales 12.5 10.5 10.2 9.0

Total expenditure 167 88 88.8 446 726 (38.5)

% of net sales 77.0 95.0 85.3 76.5

Operating profit 50 5 973.2 77 223 (65.6)

OPM(%) 23.0 5.0 14.7 23.5

Other operating income 0 0 - 0 0 -

EBIDTA 50 5 973.2 77 223 (65.6)

EBITDA margins (%) 23.0 5.0 14.7 23.5

Interest 3 2 58.9 13 5 177.1

Depreciation 14 8 67.2 39 28 39.1

Other income 1 0 196.5 7 4 97.4

Exceptional items (14) 13 - 45 (45) -

PBT 21 8 170.4 77 149 (48.3)

% of net sales 9.5 8.2 14.8 15.7

Tax 7 2 321.6 14 26 (46.1)

% of PBT 33.2 21.3 18.1 17.4

Adj. PAT 27 (7) - 18 168 (89.0)

% of net sales 12.7 (7.0) 3.5 17.7

FDEPS (Rs) 8.1 (1.9) - 5.4 49.0 (88.9)

Source: Company, Angel Research

Other key highlights

SEML’s pellet plant started commercial production from April 2010. During the

quarter, the plant produced 54,615 tonnes.

Average realisation for sponge iron, ferro alloy and power was ~Rs16,000,

Rs59,000 and Rs4.22, respectively.

The company has shipped 150,000 tonnes of iron ore fines from its mines to

the plant. Mining operations are expected to restart post monsoons.

During the quarter, SEML was also involved in trading activity. It purchased

and resold ~Rs30cr of ferro alloy and manganese ore, which contributed

~Rs3.0cr to the operating profit.

August 2, 2010 2

4. Sarda Energy | 1QFY2011 Result Update

Result highlights

Robust top-line growth

SEML’s 1QFY2011 top line grew by 132.8% yoy to Rs217cr on the back of higher

sales volume and realisations. While sponge iron sales grew by 28.9% yoy to

51,229 tonnes, ferro alloy sales grew by 161.7% yoy to 13,800 tonnes. Further,

while power production was higher by 97.6% yoy to 104mn units (last year

operations were disrupted due to fire), units sold declined by 41.0% yoy due to

increased captive usage. During the quarter, SEML produced 54,615 tonnes of

pellets.

Exhibit 5: Quarterly revenue trend

250 150

217

200 174 100

154

150 50

(Rs cr)

(%)

102

93

100 0

50 (50)

0 (100)

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Net revenue (LHS) yoy change (RHS)

Source: Company, Angel Research

EBITDA growth much higher, leading to strong bottom-line growth

EBITDA grew by 973.2% yoy to Rs50cr as margins expanded to 23.0% from 5.0%

in 1QFY2010. Raw-material costs as a percentage of sales declined to 60.7% from

77.1% in 1QFY2010 because of availability of captive coal (Karwahi mine started

operations in 3QFY2010) and resumption of shipment of iron ore from the

Dongarbore mine (mining operations were disrupted last year due to Naxal

problem). Staff cost and other expenses grew by 50% and 177% yoy to Rs7cr and

Rs27cr, respectively. On a sequential basis, margins improved by 304bp because

of a decrease in raw-material cost.

Exhibit 6: Quarterly margins trend

60 25

50

50 20

40 35

31 15

(Rs cr)

30

(%)

10

20

10 6 5

5

0 0

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

EBITDA (LHS) EBITDA margin (RHS)

Source: Company, Angel Research

August 2, 2010 4

5. Sarda Energy | 1QFY2011 Result Update

Adjusted for forex loss of Rs14cr (1QFY2010: gain of Rs13cr; 4QFY2010: gain of

Rs5cr), net profit increased to Rs27cr from a loss of Rs7cr in 1QFY2010 and a

profit of Rs17cr in 4QFY2010.

Exhibit 7: Quarterly net profit trend

30 27 15

25

10

20 17

15 13

5

(Rs cr)

10

(%)

5 0

0

(5)

(5)

(4)

(10) (7) (10)

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Adj. Net profit(LHS) Adj. Net margin (RHS)

Source: Company, Angel Research

Investment rationale

Captive iron ore, coal to lower costs: We expect SEML to earn incremental EBITDA

of Rs33cr and Rs36cr in FY2011E and FY2012E, respectively, on account of

securing coal from its captive mines. Moreover, SEML has started shipping iron ore

from its Dongarbore mines, which was affected by Naxal activities last year.

Pellet production to lower raw-material costs: SEML has started commercial

production of its 0.6mn tonne pellet plant in April 2010. Over the last six months,

management has successfully resolved most of the structural problems. We expect

the plant to operate at 45% and 50% utilisation levels in FY2011E and FY2012E,

thereby resulting in savings of Rs88cr and Rs105cr, respectively.

Uptick in ferro alloy prices and volume, increasing power production: Ferro alloy

prices have increased to Rs65,000/tonne from Rs51,000/tonne in December

2009. Sales volumes are likely to increase by 58.5% in FY2011E. Further, we

expect power generation to increase by 40.6% yoy as last year’s operations were

disrupted by fire. SEML is expanding its power capacity by a) 50% to 90MW at its

Raipur plant and b) by setting up an 80MW plant near its coal mine; we have not

factored these expansions in our estimates, as they are subject to regulatory

approvals.

August 2, 2010 5

6. Sarda Energy | 1QFY2011 Result Update

Outlook and valuation

We believe SEML is well poised to benefit from: a) backward integration into coal

and iron ore, b) commercial production of pellets and c) increased power and

ferro alloy production. We expect the full benefits of captive coal to reflect in

FY2011E as the coal mine started operations in 3QFY2010. Moreover, an uptick

in ferro alloy prices accompanied by 58.5% jump in volumes and 40.6% increase

in power generation are expected to boost EBITDA by 189.6% yoy in FY2011E to

Rs222cr. We maintain Accumulate on the stock with a Target Price of Rs290,

valuing the stock at 5.0x FY2012E EV/EBITDA.

Exhibit 8: Key assumptions

FY11E FY12E

Sales volume (tonnes)

Sponge iron 214,653 222,980

Steel billets 20,000 30,000

Ferro alloys 57,471 61,456

Power (mn units) 111 97

Average realisation (Rs)

Sponge iron 18,700 19,250

Steel billets 26,700 27,250

Ferro alloys 60,000 65,000

Power 4.0 4.0

Average cost (Rs)

Iron ore 3,596 3,604

Coal/coke 1,752 1,775

Manganese ore 11,000 11,550

Source: Company, Angel Research

Exhibit 9: EPS - Angel forecast vs. consensus

Year (%) Angel forecast Bloomberg consensus Variation (%)

FY11E 35.2 41.5 (15.2)

FY12E 43.9 55.6 (20.9)

Source: Bloomberg, Angel Research

August 2, 2010 6

13. Sarda Energy | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Sarda Energy

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

August 2, 2010 13