Digital Transformation in the PLM domain - distrib.pdf

JK Tyre 4QFY2010 Results Below Estimates

1. 4QFY2010 Result Update I Automobile

May 26, 2010

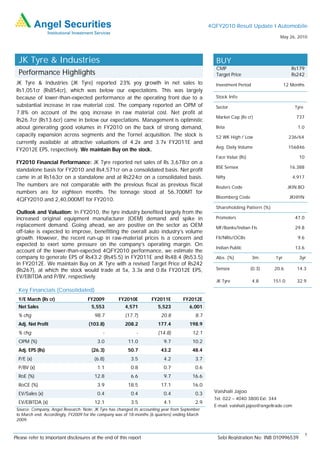

JK Tyre & Industries BUY

CMP Rs179

Performance Highlights Target Price Rs242

JK Tyre & Industries (JK Tyre) reported 23% yoy growth in net sales to Investment Period 12 Months

Rs1,051cr (Rs854cr), which was below our expectations. This was largely

because of lower-than-expected performance at the operating front due to a Stock Info

substantial increase in raw material cost. The company reported an OPM of Sector Tyre

7.8% on account of the qoq increase in raw material cost. Net profit at

Market Cap (Rs cr) 737

Rs26.7cr (Rs13.6cr) came in below our expectations. Management is optimistic

about generating good volumes in FY2010 on the back of strong demand, Beta 1.0

capacity expansion across segments and the Tornel acquisition. The stock is 52 WK High / Low 236/64

currently available at attractive valuations of 4.2x and 3.7x FY2011E and

Avg. Daily Volume 156846

FY2012E EPS, respectively. We maintain Buy on the stock.

Face Value (Rs) 10

FY2010 Financial Performance: JK Tyre reported net sales of Rs 3,678cr on a

BSE Sensex 16,388

standalone basis for FY2010 and Rs4,571cr on a consolidated basis. Net profit

came in at Rs163cr on a standalone and at Rs224cr on a consolidated basis. Nifty 4,917

The numbers are not comparable with the previous fiscal as previous fiscal Reuters Code JKIN.BO

numbers are for eighteen months. The tonnage stood at 56,700MT for

Bloomberg Code JKI@IN

4QFY2010 and 2,40,000MT for FY2010.

Shareholding Pattern (%)

Outlook and Valuation: In FY2010, the tyre industry benefited largely from the

increased original equipment manufacturer (OEM) demand and spike in Promoters 47.0

replacement demand. Going ahead, we are positive on the sector as OEM MF/Banks/Indian FIs 29.8

off-take is expected to improve, benefitting the overall auto industry’s volume

growth. However, the recent run-up in raw-material prices is a concern and FII/NRIs/OCBs 9.6

expected to exert some pressure on the company’s operating margin. On

Indian Public 13.6

account of the lower-than-expected 4QFY2010 performance, we estimate the

company to generate EPS of Rs43.2 (Rs45.5) in FY2011E and Rs48.4 (Rs53.5) Abs. (%) 3m 1yr 3yr

in FY2012E. We maintain Buy on JK Tyre with a revised Target Price of Rs242

(Rs267), at which the stock would trade at 5x, 3.3x and 0.8x FY2012E EPS, Sensex (0.3) 20.6 14.3

EV/EBITDA and P/BV, respectively.

JK Tyre 4.8 151.0 32.9

Key Financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 5,553 4,571 5,523 6,001

% chg 98.7 (17.7) 20.8 8.7

Adj. Net Profit (103.8) 208.2 177.4 198.9

% chg - - (14.8) 12.1

OPM (%) 3.0 11.0 9.7 10.2

Adj. EPS (Rs) (26.3) 50.7 43.2 48.4

P/E (x) (6.8) 3.5 4.2 3.7

P/BV (x) 1.1 0.8 0.7 0.6

RoE (%) 12.8 6.6 9.7 16.6

RoCE (%) 3.9 18.5 17.1 16.0

EV/Sales (x) 0.4 0.4 0.4 0.3 Vaishali Jajoo

Tel: 022 – 4040 3800 Ext: 344

EV/EBITDA (x) 12.1 3.5 4.1 2.9

E-mail: vaishali.jajoo@angeltrade.com

Source: Company, Angel Research; Note: JK Tyre has changed its accounting year from September

to March end. Accordingly, FY2009 for the company was of 18-months (6 quarters) ending March

2009.

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. JK Tyre & Industries I 4QFY2010 Result Update

Exhibit 1: 4QFY2009 Financial Performance (Standalone)

Y/E March (Rs cr) 4QFY10 4QFY09 % chg FY10 FY09 % chg

Net Sales (include Other

1,050.6 854.2 23.0 3,691.6 4,922.1 (25.0)

Op. Inc.)

Consumption of Raw

711.2 592.3 20.1 2,332.9 3,395.3 (31.3)

Material

(% of Sales) 67.7 69.3 63.2 69.0

Staff Costs 63.1 44.7 40.9 254.0 295.0 (13.9)

(% of Sales) 6.0 5.2 6.9 6.0

Purchases of Traded Goods 6.0 4.6 30.7 36.8 71.9 (48.8)

(% of Sales) 0.6 0.5 1.0 1.5

Other Expenses 188.2 140.8 33.6 648.4 848.2 (23.6)

(% of Sales) 17.9 16.5 17.6 17.2

Total Expenditure 968.4 782.4 23.8 3,272.1 4,610.4 (29.0)

Operating Profit 82.2 71.8 14.5 419.5 311.8 34.6

OPM 7.8 8.4 11.4 6.3

Interest 18.7 31.2 (40.1) 88.7 157.8 (43.8)

Depreciation 22.3 19.4 14.7 86.0 113.4 (24.2)

Other Income (3.0) 0.3 (976.5) 0.8 1.3 (39.5)

PBT (excl. Extr. Items) 38.3 21.5 77.8 245.7 41.9 486.2

Extr. Income/(Expense) - - - - - -

PBT (incl. Extr. Items) 38.3 21.5 77.8 245.7 41.9 486.2

(% of Sales) 3.6 2.5 6.7 0.9

Provision for Taxation 11.5 7.9 46.2 82.2 22.9 259.6

(% of PBT) 30.1 36.6 33.5 54.5

Reported PAT 26.7 13.6 96.1 163.5 19.0 758.1

PATM 2.5 1.6 4.4 0.4

Equity capital (cr) 41.1 41.1 41.1 41.1

EPS (Rs) 6.5 3.3 96.1 39.8 4.6 758.1

Source: Company, Angel research

Marginal top-line growth; strike affects sales: JK Tyre reported 23% yoy growth in

net sales to Rs1,051cr (Rs854cr) in 4QFY2010. In tonnage terms, the company

registered 11.2% yoy growth in volume to 56,700MT in 4QFY2010 (51,500MT in

3QFY2010 and 51,000MT in 4QFY2009). JK Tyre announced a hike in prices in

3QFY2010 and 4QFY2010 to pass-through the raw-material cost increase. An

average of ~5% hike across the segments was applicable from January 2009 to

abbreviate the increase in raw-material costs. The average procurement price of

rubber in 4QFY2010 stood at Rs145/Kg compared to Rs119/Kg in 3QFY2010.

OPM below expectation due to increased raw material cost: The company’s

operating profit increased 14.5% yoy to Rs82.2cr (Rs71.8cr). However, on a qoq

basis, OPM dropped by 449bp yoy to 7.8% (11.7% in 3QFY2010), which was below

our estimates. This was primarily on account of the 586bp qoq jump in raw-material

cost. The company attributed the substantial contraction in OPM to change in

product mix and higher rubber prices. OPM growth was also partially arrested by

the spike in other expenditure, which comprised discounts and other selling and

distribution expenses. The company also hiked prices by 5% in 4QFY2010 and has

guided on subsequent price hikes in the event of increasing rubber prices.

Management has guided to sustain margins of 10–10.5% in FY2011E.

Net profit below expectations at Rs26.7cr: For 4QFY2010, JK Tyre recorded a

96.1% yoy increase in net profit to Rs26.7cr (Rs13.6cr), which was below our

estimates, primarily on account of a low base of last year and significant payback in

working capital loans leading to a fall in interest costs (debt on books of standalone

entity is Rs860cr).

May 26, 2010 2

3. JK Tyre & Industries I 4QFY2010 Result Update

Conference Call Highlights

Rubber prices touching new highs

JK Tyre will continue to face pressure on the margin front due to increasing rubber

prices. Average rubber price for the company during 4QFY2010 was nearly

Rs145/Kg as against Rs119/Kg in 3QFY2010. Rubber prices are currently trading at

Rs155–158/Kg. Average rubber price for the company for FY2010 was Rs110/kg.

On account of the monsoon season, the company has maintained rubber inventory

for 45 days. Almost the entire inventory is at a price of Rs145/Kg. Given that rubber

prices have increased further, prices of petroleum products are witnessing a

downtrend, which should help the company protect margins to some extent.

Therefore, the company expects EBITDA margins to be maintained at 10–10.5% for

FY2011E.

Exhibit 2: Natural Rubber Price Trend (Rs119/Kg)

160

140

120

100

80

60

40

20

0

Q1FY05

Q2FY05

Q3FY05

Q4FY05

Q1FY06

Q2FY06

Q3FY06

Q4FY06

Q1FY07

Q2FY07

Q3FY07

Q4FY07

Q1FY08

Q2FY08

Q3FY08

Q4FY08

Q1FY09

Q2FY09

Q3FY09

Q4FY09

Q1FY10

Q2FY10

Q3FY10

Q4FY10

Average Prices (Rs. Per kg)

Source: Bloomberg, Angel research

JK Tyre has initiated a 4% price increase, which will be in effect from June 1, 2010,

for the replacement category. This raise comes on the back of a 6.7% increase in

prices in FY2010. Normally it takes three months for the price increase to pass on to

the OEM segment. Net sales realisation for the company increased about 1.5% for

4QFY2010. The entire price hike did not reflect into sales realisation because of the

sales mix. Average net sales realisation is likely to increase by 2–2.5% in FY2011.

Capacity expansion plans

Currently, JK Tyre is running at almost full capacity and is partially unable to meet

increasing OEM demand. Therefore, the company has major expansion plans on

the anvil across segments, with most of the capacities coming on board from

2011E–2012E. The company’s total capacity post the expansions is slated at

12.6mn tyres annually. The company incurred a capex of Rs315cr for FY2010 and

has lined up a capex of Rs750cr for FY2011E. The company has overall capital

expenditure plans of Rs930cr in the next two years, out of which Rs776cr is for a

Greenfield facility at Chennai, which could be operational by 2012. This facility will

produce 25 lakh passenger car radials, 2 lakh bus radials and 2 lakh truck radials.

The remaining capex will be used for expanding the facility at the Mysore plant from

8 lakh to 10 lakh radials at a cost of Rs154 cr. The expansion is expected to be

completed by March 2011. Consequently, the company’s domestic capacity will

reach 1.25cr tyres a year in 2012.

JK Tyre is currently expanding its off-road tyre (ultra large-size tyre) capacity by

3,000 tyres a year to 42,000 tyres per year, primarily for Bharat Earth Movers

(BEML), at a cost of Rs120cr. The company has, in fact, delivered the first batch of its

ultra large-size tyres to BEML ahead of schedule.

May 26, 2010 3

4. JK Tyre & Industries I 4QFY2010 Result Update

JK Tyre has completed its truck and bus radial (T&BR) capacity expansion plan, with

an investment of Rs315cr, and will have increased capacity from 307,000 tyres to

800,000 tyres per year by October 2010. This capacity has been running at almost

100% capacity utilisation in November and December 2009. Therefore,

management plans to increase its radial capacity by another 4 lakh tyres to 12 lakh

tyres per year over the next three years.

Update on Tornel operations

JK Tyre had acquired Tornel, Mexico, in June 2008 for a consideration of nearly

Rs270cr through a 100% special purpose vehicle. According to management,

Tornel, which has a total capacity of 6.6mn tonnes per year, recorded a turnover of

around Rs1,000cr in CY2009, net profit of nearly Rs60cr and debt of Rs150cr–

160cr in books as on December 31, 2009. Tornel’s operations turned EPS accretive

for JK Tyre in its first year of operation. Tornel contributed positively to the sales and

profitability of the company on a consolidated basis. Net sales for Tornel were up

10% for FY2010. The company continues to operate in a challenging environment.

It faces cost pressures on the raw-material front on account of increased rubber

prices and because of the depreciation of Mexican pesos versus the US dollar.

Tornel is currently operating at a 60–70% utilisation level.

Management outlook

Management is positive about the auto industry’s growth, including the commercial

vehicle and the passenger vehicle segments, and has planned capacity expansions

to meet the demand arising from the uptrend in the auto industry in general. With

new international players entering the compact car segment particularly,

management expects the industry to witness ~18% annual growth in the passenger

car radial segment over the next couple of years. Management is also optimistic on

an upturn in the CV cycle and off-take from its strong clients, Ashok Leyland and

Tata Motors. Further, management expects the T&BR segment to register 8–10%

annual growth over the next couple of years.

The acquisition of Tornel, which is majorly into truck, LCV, farm and industrial tyres

in the bias category and truck, LCV and high-speed passenger car tyres, has given

JK Tyre a strong hold in the South American market, which will help increase

contribution from the company’s international business.

Debt levels for the company as in March 2010 have gone down from Rs1,100cr to

Rs860cr on a standalone basis, and from Rs1,382cr to Rs1,158cr on a consolidated

basis. The company continues to maintain cash at a normal level of Rs50–60cr.

Production volumes for JK Tyre for FY2011E could be up by 20–25% as demand

from passenger cars, trucks and buses remains robust. Currently, demand for tyres

is exceeding the supply. The company should also benefit from full capacity

utilisation at the Kankroli tyre plant in FY2011E. The disruption in operations last

year due to the illegal strike by workmen led to a decline of Rs300cr in sales and a

loss of Rs30–35cr at the EBITDA level.

May 26, 2010 4

5. JK Tyre & Industries I 4QFY2010 Result Update

Outlook and Valuation

In FY2010, the tyre industry benefited largely from the substantial increase in OEM

demand and spike in replacement demand. Going ahead, we are positive on the

sector as OEM off-take is expected to improve, benefitting the overall auto industry’s

volume growth. However, the recent run-up in raw-material prices is a concern and

expected to exert some pressure on the company’s operating margin. On account of

the lower-than-expected 4QFY2010 performance, we estimate the company to

register EPS of Rs43.2 (Rs45.5) in FY2011E and Rs48.4 (Rs53.5) in FY2012E.

Exhibit 3: One year forward EV/EBITDA Band

5,000

4,400 8x

3,800

3,200 6x

EV (Rs cr)

2,600

4x

2,000

1,400

2x

800

200

Sep-02

Sep-03

Sep-04

Sep-05

Sep-06

Sep-07

Sep-08

Sep-09

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

May-03

May-04

May-05

May-06

May-07

May-08

May-09

May-10

Source: C-line, Angel Research

We believe that strong demand, prevailing high-capacity utilisation levels and higher

investment requirements will help the Indian tyre industry to arrest the sharp decline

in margins despite the upward move in input costs (rubber and carbon black). Thus,

we maintain a Buy view on JK Tyre with a revised Target Price of Rs242 (Rs267), at

which the stock would trade at 5x, 3.3x and 0.8x FY2012E EPS, EV/EBITDA and

P/BV, respectively.

May 26, 2010 5

6. JK Tyre & Industries I 4QFY2010 Result Update

Profit & Loss Statement (Consolidated) Rs cr

Y/E March FY2007 FY2009* FY2010 FY2011E FY2012E

Gross sales 3,196 6,109 4,849 5,939 6,595

Less: Excise duty 400.6 556.2 278.6 415.7 593.5

Net Sales 2,795 5,553 4,571 5,523 6,001

Total operating income 2,795 5,553 4,571 5,523 6,001

% chg 7.9 - - 20.8 8.7

Total Expenditure 2,540 5,388 4,069 4,988 5,392

Net Raw Materials 1,854 3,956 2,841 3,645 3,961

Other Mfg costs 298.1 643.4 795.6 624.1 666.2

Personnel 176.7 382.0 432.1 331.4 351.1

Other 211.7 407.0 - 386.6 414.1

EBITDA 254.7 164.9 502.0 535.8 609.1

% chg 68.4 - - 6.7 13.7

(% of Net Sales) 9.1 3.0 11.0 9.7 10.2

Depreciation & Amortisation 75.4 122.5 99.6 124.1 169.1

EBIT 179.2 42.4 402.4 411.7 440.1

% chg 123.3 - - 2.3 6.9

(% of Net Sales) 6.4 0.8 8.8 7.5 7.3

Interest & other Charges 91.1 171.2 115.7 154.6 150.8

Other Income 12.6 53.9 14.9 15.8 16.7

(% of PBT) 12.5 (71.7) 4.7 5.8 5.5

Share in profit of Associates - - - - -

Recurring PBT 100.7 (74.9) 301.5 272.9 306.0

% chg 363.5 - - (9.5) 12.1

Extraordinary Expense/(Inc.) (0.2) 0.2 (15.6) - -

PBT (reported) 100.9 (75.1) 317.1 272.9 306.0

Tax 34.0 32.9 93.3 95.5 107.1

(% of PBT) 33.7 (43.8) 29.4 35.0 35.0

PAT (reported) 66.9 (108.1) 223.8 177.4 198.9

Less: Minority interest (MI) (2.7) (4.1) - - -

PAT after MI (reported) 69.6 (104.0) 223.8 177.4 198.9

ADJ. PAT 69.4 (103.8) 208.2 177.4 198.9

% chg - - - (14.8) 12.1

(% of Net Sales) 2.5 (1.9) 4.6 3.2 3.3

Basic EPS (Rs) 22.6 (26.3) 50.7 43.2 48.4

Fully Diluted EPS (Rs) 22.5 (25.3) 50.7 43.2 48.4

% chg - - - (14.8) 12.1

May 26, 2010 6

7. JK Tyre & Industries I 4QFY2010 Result Update

Balance Sheet (Consolidated) Rs cr

Y/E March FY2007 FY2009* FY2010E FY2011E FY2012E

SOURCES OF FUNDS

Equity Share Capital 30.8 41.1 41.1 41.1 41.1

Preference Capital - - - - -

Reserves& Surplus 513 651 849 1,007 1,184

Shareholders’ Funds 544 692 890 1,048 1,225

Minority Interest - - - - -

Total Loans 915 1,382 1,158 1,508 1,508

Deferred Tax Liability 105.3 112.0 111.7 111.7 111.7

Total Liabilities 1,564 2,186 2,159 2,668 2,845

APPLICATION OF FUNDS

Gross Block 2,156 2,840 3,288 4,002 4,226

Less: Acc. Depreciation 957 1,228 1,328 1,452 1,621

Net Block 1,199 1,612 1,960 2,550 2,605

Capital Work-in-Progress 20.3 290.5 131.5 120.1 84.5

Goodwill - - - - -

Investments 71.4 75.9 75.9 80.0 85.3

Current Assets 1,106 1,334 1,429 1,660 1,905

Cash 30.0 51.3 57.7 (25.0) 74.1

Loans & Advances 137.2 249.6 228.5 303.8 330.1

Other 938 1,033 1,143 1,381 1,500

Current liabilities 840 1,131 1,442 1,748 1,840

Net Current Assets 266 202 (13) (88) 65

Mis. Exp. not written off 8.2 5.2 5.2 5.2 5.2

Total Assets 1,564 2,186 2,159 2,668 2,845

Cash Flow Statement (Consolidated) Rs cr

Y/E March FY2007 FY2009* FY2010E FY2011E FY2012E

Profit before tax 100.9 (75.1) 317.1 272.9 306.0

Depreciation 75.4 122.5 99.6 124.1 169.1

Change in Working Capital 60.8 (171.6) (194.7) (64.1) 33.8

Less: Other income 6.5 (841.1) (112.8) (283.6) (34.7)

Direct taxes paid 34.0 32.9 93.3 95.5 107.1

Cash Flow from Operations 196.7 683.9 241.5 520.9 436.5

(Inc.)/ Dec. in Fixed Assets (69.7) (954.6) (288.7) (702.8) (188.4)

(Inc.)/ Dec. in Investments (3.8) (4.5) - (4.1) (5.3)

(Inc.)/ Dec. in loans and

advances 7.1 (91.6) (37.7) (75.3) 26.3

Other income 12.6 53.9 14.9 15.8 16.7

Cash Flow from Investing (53.8) (996.8) (311.6) (766.4) (150.6)

Issue of Equity (13.1) 71.0 - - -

Inc./(Dec.) in loans (28.9) 467.5 (224.4) 350.0 -

Dividend Paid (Incl. Tax) 9.7 13.0 16.8 16.8 19.2

Others (120.8) (217.1) 283.9 (204.0) (206.0)

Cash Flow from Financing (153.1) 334.3 76.3 162.8 (186.7)

Inc./(Dec.) in Cash (10.2) 21.4 6.3 (82.7) 99.1

Opening Cash balances 40.2 30.0 51.4 57.7 (25.0)

Closing Cash balances 30.0 51.4 57.7 (25.0) 74.1

May 26, 2010 7

8. JK Tyre & Industries I 4QFY2010 Result Update

Key Ratios

Y/E March FY2007 FY2009* FY2010E FY2011E FY2012E

Valuation Ratio (x)

P/E (on FDEPS) 7.9 (6.8) 3.5 4.2 3.7

P/CEPS 3.9 50.5 2.4 2.4 2.0

P/BV 1.0 1.1 0.8 0.7 0.6

Dividend yield (%) 1.5 1.5 2.0 2.2 2.5

EV/Sales 0.5 0.4 0.4 0.4 0.3

EV/EBITDA 5.4 12.1 3.5 4.1 2.9

EV / Total Assets 0.4 0.3 0.3 0.3 0.3

Per Share Data (Rs)

EPS (Basic) 22.6 (26.3) 50.7 43.2 48.4

EPS (fully diluted) 22.5 (25.3) 50.7 43.2 48.4

Cash EPS 46.2 3.6 75.0 73.4 89.6

DPS 2.7 2.7 3.5 4.0 4.5

Book Value 176.7 168.4 216.7 255.2 298.4

DuPont Analysis

EBIT margin 6.4 0.8 8.8 7.5 7.3

Tax retention ratio 0.7 1.4 0.7 0.7 0.6

Asset turnover (x) 1.8 2.6 2.5 3.0 4.0

ROIC (Post-tax) 7.8 2.9 15.5 14.6 18.8

Cost of Debt (Post Tax) 6.5 17.8 6.4 7.5 6.5

Leverage (x) 1.4 3.6 1.4 1.3 1.2

Operating ROE 9.7 (51.3) 28.5 23.6 34.1

Returns (%)

ROCE (Pre-tax) 11.5 3.9 18.5 17.1 16.0

Angel ROIC (Pre-tax) 11.7 2.0 19.1 15.3 15.9

ROE 7.1 12.8 6.6 9.7 16.6

Turnover ratios (x)

Asset Turnover (Gross Block) 1.3 2.2 1.8 1.5 1.5

Inventory / Sales (days) 56.9 48.7 45.6 45.6 45.6

Receivables (days) 59.6 48.6 45.6 45.6 45.6

Payables (days) 102.5 90.3 95.2 99.8 103.7

Working capital cycle (ex-cash)

(days) 27.0 5.0 3.2 (4.4) (2.2)

Solvency ratios (x)

Net debt to equity 1.5 1.8 1.2 1.4 1.1

Net debt to EBITDA 3.2 7.6 2.0 2.7 2.2

Interest Coverage (EBIT / Interest) 2.0 0.2 3.5 2.7 2.9

Note: * JK Tyre has changed its accounting year from September to March end. Accordingly, FY2009 for the

company was of 18-months (6 quarters) ending March 2009.

May 26, 2010 8

9. JK Tyre & Industries I 4QFY2010 Result Update

Research Team Tel: 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable source believed to be true,

and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly, we

cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel

Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement JK Tyre & Industries

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 26, 2010 9