1. 1QFY2011 Result Update | Automobile

July 23, 2010

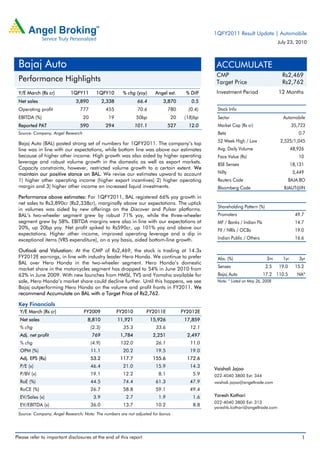

Bajaj Auto ACCUMULATE

CMP Rs2,469

Performance Highlights Target Price Rs2,762

Y/E March (Rs cr) 1QFY11 1QFY10 % chg (yoy) Angel est. % Diff Investment Period 12 Months

Net sales 3,890 2,338 66.4 3,870 0.5

Operating profit 777 455 70.6 780 (0.4) Stock Info

EBITDA (%) 20 19 50bp 20 (18)bp Sector Automobile

Reported PAT 590 294 101.1 527 12.0 Market Cap (Rs cr) 35,723

Source: Company, Angel Research Beta 0.7

52 Week High / Low 2,525/1,045

Bajaj Auto (BAL) posted strong set of numbers for 1QFY2011. The company’s top

line was in line with our expectations, while bottom line was above our estimates Avg. Daily Volume 48,926

because of higher other income. High growth was also aided by higher operating Face Value (Rs) 10

leverage and robust volume growth in the domestic as well as export markets.

BSE Sensex 18,131

Capacity constraints, however, restricted volume growth to a certain extent. We

maintain our positive stance on BAL. We revise our estimates upward to account Nifty 5,449

1) higher other operating income (higher export incentives) 2) higher operating Reuters Code BAJA.BO

margin and 3) higher other income on increased liquid investments. Bloomberg Code BJAUT@IN

Performance above estimates: For 1QFY2011, BAL registered 66% yoy growth in

net sales to Rs3,890cr (Rs2,338cr), marginally above our expectations. The uptick

Shareholding Pattern (%)

in volumes was aided by new offerings on the Discover and Pulsar platforms.

BAL’s two-wheeler segment grew by robust 71% yoy, while the three-wheeler Promoters 49.7

segment grew by 58%. EBITDA margins were also in line with our expectations at MF / Banks / Indian Fls 14.7

20%, up 20bp yoy. Net profit spiked to Rs590cr, up 101% yoy and above our FII / NRIs / OCBs 19.0

expectations. Higher other income, improved operating leverage and a dip in

exceptional items (VRS expenditure), on a yoy basis, aided bottom-line growth. Indian Public / Others 16.6

Outlook and Valuation: At the CMP of Rs2,469, the stock is trading at 14.3x

FY2012E earnings, in line with industry leader Hero Honda. We continue to prefer Abs. (%) 3m 1yr 3yr

BAL over Hero Honda in the two-wheeler segment. Hero Honda’s domestic

Sensex 2.5 19.0 15.2

market share in the motorcycles segment has dropped to 54% in June 2010 from

62% in June 2009. With new launches from HMSI, TVS and Yamaha available for Bajaj Auto 17.2 110.5 NA*

sale, Hero Honda’s market share could decline further. Until this happens, we see Note: * Listed on May 26, 2008

Bajaj outperforming Hero Honda on the volume and profit fronts in FY2011. We

recommend Accumulate on BAL with a Target Price of Rs2,762.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net sales 8,810 11,921 15,926 17,859

% chg (2.3) 35.3 33.6 12.1

Adj. net profit 769 1,784 2,251 2,497

% chg (4.9) 132.0 26.1 11.0

OPM (%) 11.1 20.2 19.5 19.0

Adj. EPS (Rs) 53.2 117.7 155.6 172.6

P/E (x) 46.4 21.0 15.9 14.3

Vaishali Jajoo

P/BV (x) 19.1 12.2 8.1 5.9 022-4040 3800 Ext: 344

RoE (%) 44.5 74.4 61.3 47.9 vaishali.jajoo@angeltrade.com

RoCE (%) 26.7 58.8 59.1 49.4

EV/Sales (x) 3.9 2.7 1.9 1.6 Yaresh Kothari

022-4040 3800 Ext: 313

EV/EBITDA (x) 36.0 13.7 10.2 8.8

yareshb.kothari@angeltrade.com

Source: Company, Angel Research; Note: The numbers are not adjusted for bonus

Please refer to important disclosures at the end of this report 1

3. Bajaj Auto | 1QFY2011 Result Update

Top line marginally above expectations, volumes up by 70%: BAL reported 66.4%

yoy jump in top line to Rs3,890cr (Rs2,338cr), mainly driven by the substantial

70% yoy increase in total volumes. Discover 100 and Pulsar have been the primary

game-changer brands for BAL. Average realisation recorded a decline of about

2.4% yoy during the quarter, primarily due to higher contribution of low-end bikes

(Discover) in the sales mix.

The company’s domestic motorcycle sales grew 71% (as against the industry

growth of 24%) in 1QFY2011. Higher sales in the three-wheeler segment at

99,918 units (63,242) also supported healthy revenue growth. BAL exported

323,899 (178,295) vehicles, an increase of 81.7% yoy in 1QFY2011. During the

quarter, production constraints limited sales to a certain extent. The company

expects motorcycle capacity of 300,000units/month to go on stream from

2QFY2011.

In terms of volume market share, the company improved its position in the two-

wheeler category by 524bp yoy to 20.8% (15.5%) in 1QFY2011, largely owing to

a 745bp yoy increase in the motorcycle segment’s market share to 27% (19.5%).

However, the three-wheeler segment’s market share declined to 36.4% (41.2%) in

1QFY2011.

Exhibit 3: Volume-driven sales growth Exhibit 4: Market share across categories

(Rs cr) (%) (%)

5,000 100 60

90.2

4,000

75 41.2 40.6 40.9

45 37.5

66.4 36.4

64.4

3,000

50 26.8 27.5 27.0

30 22.6

2,000 19.5

25 15 21.1 21.2 20.8

1,000 17.8 17.7

5.1 15.5

0 0

0

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Net Sales (LHS) Net Sales Growth (RHS) Three-wheelers Motorcycles Total Two-wheelers

Source: Company, Angel Research Source: Company, SIAM, Angel Research

EBITDA expands marginally by 50bp: During 1QFY2011, BAL’s operating margin

expanded marginally by 50bp yoy to 20%, largely in line with our estimates.

However, the company reported a 289bp qoq decline in EBITDA margin, largely

on account of the 275bp qoq increase in raw-material costs, which accounted for

67.9% of net sales.

The increase in margin on a yoy basis was on account of a decline in other

expenditure and staff costs by 158bp and 392bp, respectively, during the quarter.

Higher volumes of sportier motorcycles, effective cost management and focused

sales promotional activities helped the company to perform better than the industry

at the operating front. Thus, overall, the operating profit for the quarter increased

by 70.6% yoy to Rs777cr (Rs455cr), which largely came in line with our estimates.

July 23, 2010 3

4. Bajaj Auto | 1QFY2011 Result Update

Exhibit 5: 20% EBITDA margin guidance achieved Exhibit 6: Net profit up 101%, beats estimates

(%) (Rs cr) (%)

80 800 20

68.0 70.7

64.8 67.7

64.7 15.6 15.2

14.0 14.4

60 600 12.6 15

40 400 10

22.0 22.0 22.9 20.0

19.5

20 200 5

0

0 0

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

EBITDA Margin Raw Material Cost/Sales Net Profit (LHS) Net Profit Margin (RHS)

Source: Company, Angel Research Source: Company, Angel Research

Bottom line at Rs590cr, beats estimates: BAL recorded net profit growth of 101%

yoy to Rs590cr (Rs294cr), which was higher than our expectation by 12%, primarily

owing to higher other income of Rs81.7cr (Rs23.1cr). Other income comprised

treasury income earned on liquid assets of ~Rs3,700cr. Further, improved

operating leverage, lower depreciation, reduced tax rate and a dip in exceptional

items (VRS expenditure), on a yoy basis, aided bottom-line growth.

Conference call: Key highlights

Scenario: The two-wheeler industry continues to perform exceedingly well.

Demand is expected to increase further with the festival season approaching.

However, the industry is facing constraints on the supply front from ancillary

manufacturers and original equipment manufacturers (such as manufacturers

of bearings and tyre tubes). Capacity constraints are limiting two-wheeler

production to a certain extent. Further, meeting demand is a concern with

current inventory at lower levels. However, post the festival season, demand is

expected to come down to normal levels.

Production: The company expects to sell four million units during FY2011E in

the two-wheeler and three-wheeler categories. The additional two-wheeler

capacity by 100,000 units/month from the Pantnagar plant is expected to go

on full stream from 3QFY2011E. During 1QFY2011, the company produced

~73,000 units/month and expects to ramp it up to ~85,000 units/month by

2QFY2011E. Of the additional capacity that has gone on stream, ~30%

would be utilised towards production of Platina and the remaining for Discover

and Pulsar. The company sees a potential of ~200,000 units/month for

Discover and Pulsar and ~35,000 units/month for Platina. Currently, BAL is

running out of stock for Discover 100, Discover 150 and Pulsar 150.

On the three-wheeler front, the company is seeing additional demand

30,000–35,000 units from Tamil Nadu as the permit system in the state has

been abolished. Even on the exports front, demand remains robust. However,

the company intends to meet the domestic demand with priority and maintain

a balance between exports and domestic sales. With TVS Motor entering the

three-wheeler space, the market has become competitive and BAL continues to

lose market share; however, overall sales volumes for the company continue

to increase.

July 23, 2010 4

5. Bajaj Auto | 1QFY2011 Result Update

Price increases: In April and June 2010, BAL increased prices across its two-

wheeler brands (Platina, Discover and Pulsar) by Rs500–1,500. In the three-

wheeler segment, prices were increased by Rs2,000 in April 2010. The

company has also increased prices in the export market. Going forward, BAL

seems comfortable and does not feel any need to take action on the pricing

front.

Raw-material cost: BAL expects raw-material costs to decline marginally in

2QFY2011E qoq. However, the raw-material cost pressure is expected to be

higher on a yoy basis. The company has re-negotiated raw-material contracts

(steel and aluminium) at reduced price levels compared to 1QFY2011.

EBITDA margins: As per the management, EBITDA margins of ~20% look

extremely comfortable. EBITDA margins, which came in at 20% for

1QFY2011, were impacted by higher raw-material costs and increased labour

cost due to average yearly wage hike of ~12%. Going ahead, the company is

optimistic about maintaining margins at current levels, as raw-material prices

have cooled down in 1QFY2011 and the impact of labour cost is not expected

to recur. However, EBITDA margins can show a marginal contraction for the

full year because of administration cost and advertising spend, which were

not accounted for in 1QFY2011.

Exports: On the exports front, BAL seems to be extremely bullish and is

targeting one million units for FY2011E. However, looking at the exports

performance for 1QFY2011 (323,899 units, up ~82% yoy), the company may

easily surpass its guidance by ~200,000 units. The company is seeing robust

demand from the Sri Lankan, Egyptian, Colombian, Bangladeshi and African

markets. Within Africa, BAL is witnessing major demand from Nigeria. The

company expects Africa to be the major growth driver for exports and sees

demand growing by 20–25% for FY2011E, while demand from other countries

could be up by 10–15%. BAL enjoys higher margins (~3–4%) from exports

compared to domestic sales. The company has also taken a price increase in

the exports market post July 2010, which would also fetch higher realisations

in the remaining quarters of the current fiscal.

Capital expenditure: BAL expects overall capital investment in the range of

Rs225cr–250cr during FY2011E. The investment would be towards capacity

expansion, research and development and development of new platform for

the four-wheeler project with Renault and Nissan. The overall capacity

available for production by the end of FY11E is expected to be five million

units. It also intends to develop a multi functional platform through which it

can manufacture commercial vehicles (substitute for three-wheeler cargo) and

passenger cars. The development of the new platform will entail an investment

of Rs500cr in a phased manner.

July 23, 2010 5

6. Bajaj Auto | 1QFY2011 Result Update

Subsidiary update: The Indonesian subsidiary, which suffered an overall loss

of Rs38cr (adj. for extraordinary gains) in FY2010, suffered a loss of Rs6cr

during 1QFY2011. The company expects the Indonesian subsidiary to

break-even by FY2012E. It is targeting sales units of 25,000 during FY2011E.

The company has recently launched Pulsar 150 in Indonesia and it has been

received well in the Indonesian market.

Bajaj Auto is also working with KTM (35.2% stake in KTM) to jointly develop

engines and platforms for production. For the nine months ending May’10,

KTM recorded net profits of Euro 3mn. On the consolidated basis

management has indicated that the net profit for the company for FY12E

would be similar to the profits of the standalone entity.

Exhibit 7: Motorcycles – Volume and market share Exhibit 8: Three-wheelers – Volume and market share

(Units) (%) (Units) (%)

110,000 75

900,000 80

700,000 85,000 50

50

500,000 60,000 25

20

300,000 (10) 35,000 0

100,000 (40) 10,000 (25)

1QFY07

3QFY07

1QFY08

3QFY08

1QFY09

3QFY09

1QFY10

3QFY10

1QFY11

1QFY07

3QFY07

1QFY08

3QFY08

1QFY09

3QFY09

1QFY10

3QFY10

1QFY11

Market Share (RHS) McycleVolume (LHS) % yoy growth(RHS) Market Share (RHS) 3-wheelers Volume (LHS) % yoy growth (RHS)

Source: Company, SIAM, Angel Research Source: Company, SIAM, Angel Research

Investment Arguments

Focus on Discover and Pulsar to improve market share: BAL continues to

witness strong demand in the two-wheeler segment from its strong dual

offering of Discover and Pulsar. The successful launch of

Discover 100cc bike in the executive value segment has improved the

company’s market share to 26.7% (about 15% in June 2009) in June 2010.

BAL is positioning itself in line with its strategy of 'value and price products',

wherein it proposes to tap higher-value bike segments, which have a high

growth potential and fetch better realisations. BAL has also launched new

products in the high-margin 125cc+ segment.

Three-wheeler registering healthy growth: BAL has a strong presence in the

three-wheeler market, with an overall market share (including exports) of

around 57%. BAL still tops the passenger auto-rickshaw segment, which

accounts for around 88% of the three-wheeler market. The three-wheeler

segment fetches higher margins than the company’s two-wheeler business.

BAL has lost some market share in the three-wheeler domestic market, but

improving export volumes have more than compensated to post higher

volume growth. We expect the company’s three-wheeler volumes to grow by

11–12% over FY2010–12E.

July 23, 2010 6

7. Bajaj Auto | 1QFY2011 Result Update

High growth potential in export volumes: BAL registered strong exports CAGR

of 37% during FY2005–10, aided by a 43% CAGR in two-wheeler exports and

a 22% CAGR in three-wheeler exports. Going ahead, with strong traction in

the recent months, we estimate BAL to register a 21% CAGR over

FY2010–12E, driven by higher penetration in the African market. Bajaj has

also hedged around 75% of its FY2011 exports at a USD–INR rate of Rs47.

Hence, any sharp appreciation of the rupee in FY2011 will not have a

significant impact on the company’s margins.

Outlook and Valuation

We maintain our positive stance on BAL. We revise our estimates upward to

account 1) higher other operating income (higher export incentives) 2) higher

operating margin and 3) higher other income on increased liquid investments.

Exhibit 9: Change in estimates

Y/E March (Rs cr) Earlier estimates Revised estimates % chg

FY11E FY12E FY11E FY12E FY11E FY12E

Net sales 14,866 16,836 15,926 17,859 7.1 6.1

OPM (%) 19.4 18.8 19.5 19.0 14 19

EPS (Rs) 142.2 157.1 155.6 172.6 9.4 9.9

Source: Angel Research

At the CMP of Rs2,469, the stock is trading at 14.3x FY2012E earnings, in line with

industry leader Hero Honda. We continue to prefer BAL over

Hero Honda in the two-wheeler segment. Hero Honda’s domestic market share in

the motorcycles segment has dropped to 54% in June 2010 from 62% in June

2009. With new launches from HMSI, TVS and Yamaha available for sale, Hero

Honda’s market share could decline further. Until this happens, we see Bajaj

outperforming Hero Honda on the volume and profit fronts in FY2011. We

recommend Accumulate on BAL with a Target Price of Rs2,762.

July 23, 2010 7

14. Bajaj Auto | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Bajaj Auto

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 23, 2010 14