Downloaded 47 times

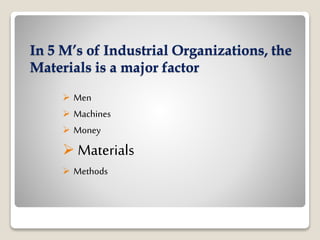

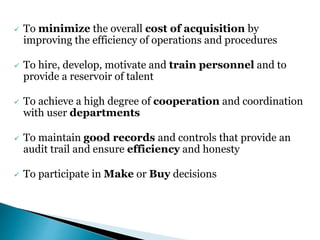

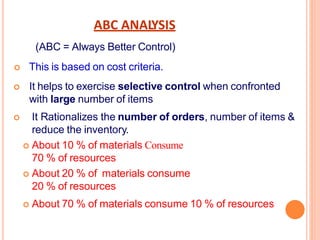

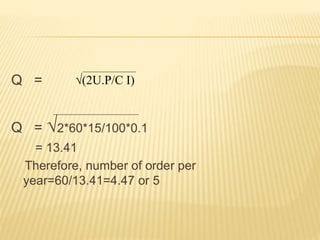

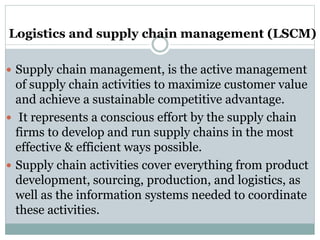

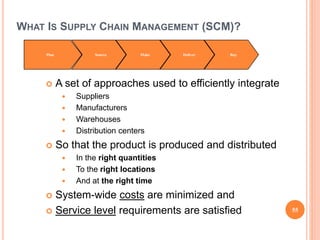

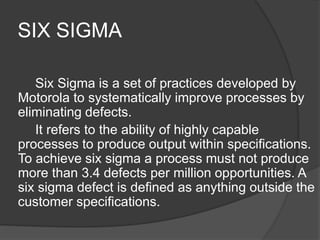

![20000050020

19950050019

19900050018

19850050017

19800050016

19750050015

19700050014

19650050013

196000150012

194500150011

193000175010

19125027509

18850040008

18450045007

18000050006

17500075005

16750075004

160000200003

140000500002

90000900001

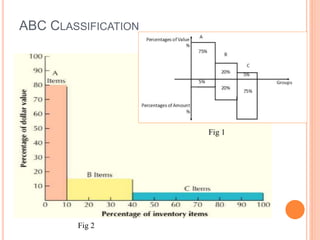

CUMMULATIVECUMMULATIVE

COSTCOST [Rs.]

ANNUAL COSTANNUAL COST

[Rs.]

ITEMITEM COST %COST %ITEM %ITEM %

70 %70 %

20 %20 %

10 %10 %

10 %10 %

20 %20 %

70 %70 %

ABC

A

N

A

L

Y

S

I

S

WORK

SHEET](https://image.slidesharecdn.com/unit-iii-materialmgmtvj-201225053624/85/Material-Management-Inventory-Control-QC-Techniques-20-320.jpg)

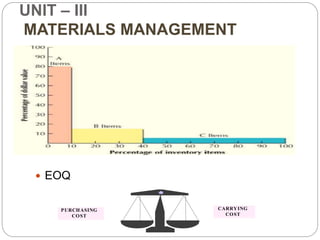

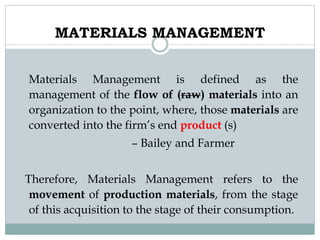

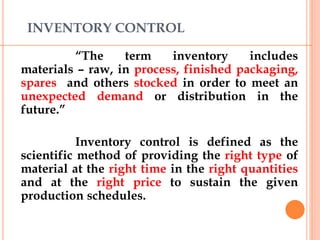

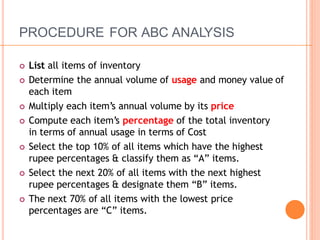

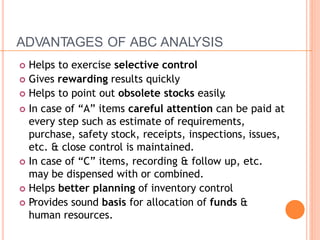

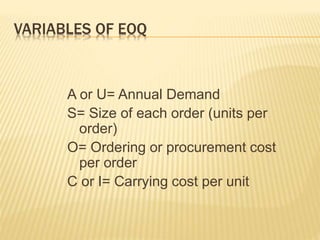

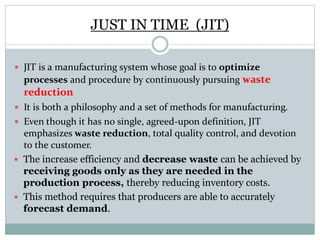

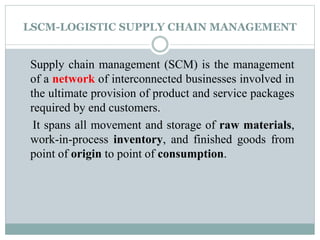

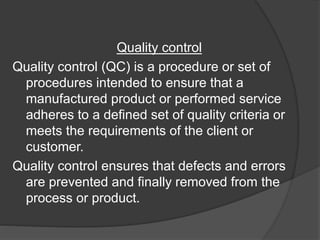

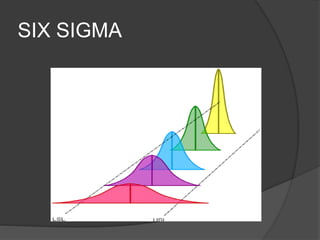

![Algebraic Method of determining EOQ:

STEP -1: Find out the total ordering cost per year

A * O [Annual Demand x Ordering

Cost]

S Size of each order

STEP -2: Find out the carrying cost per year

S * C C Carrying cost per unit

2

EOQ is one where total ordering cost is equal to

total carrying cost

A * O S * C

S 2

Therefore, EOQ = √(2AO/C) or √(2U.P/C I)](https://image.slidesharecdn.com/unit-iii-materialmgmtvj-201225053624/85/Material-Management-Inventory-Control-QC-Techniques-31-320.jpg)

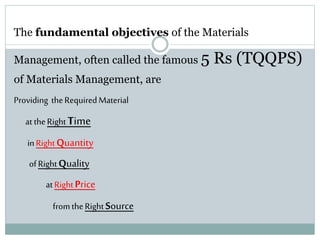

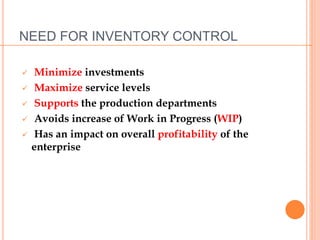

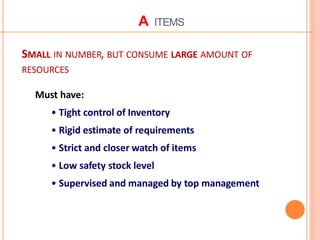

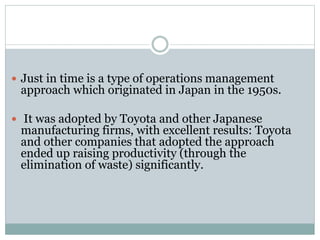

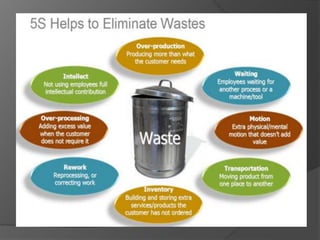

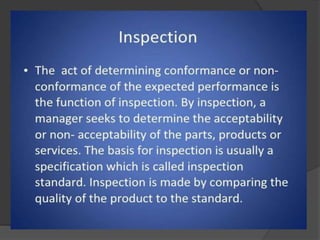

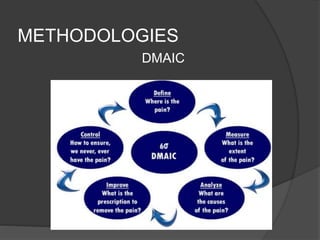

![BENEFITS OF JIT

Quality consciousness

Reduced scrap

Reduced cycle times

Smoother flow of production]

Low inventory

High productivity

High worker participation

Reduced space requirements](https://image.slidesharecdn.com/unit-iii-materialmgmtvj-201225053624/85/Material-Management-Inventory-Control-QC-Techniques-51-320.jpg)

This document provides an overview of materials management concepts including objectives of materials management, inventory control techniques, ABC analysis, economic order quantity, and Just in Time. The key points covered are: - Materials management aims to ensure the right materials are available at the right time, place, quantity and cost. Objectives include minimizing costs while maintaining quality and continuity of supply. - Inventory control techniques help manage inventory levels and costs. ABC analysis categorizes items into A, B, C to focus control efforts. Economic order quantity models balancing ordering and carrying costs to determine optimal order sizes. - Just in Time aims to optimize processes through continuous waste reduction and pursuing only what is needed, when it is needed in the production