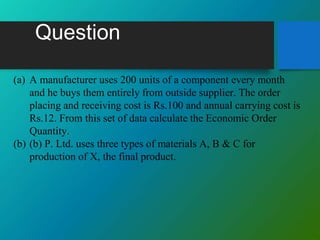

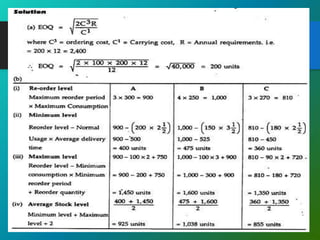

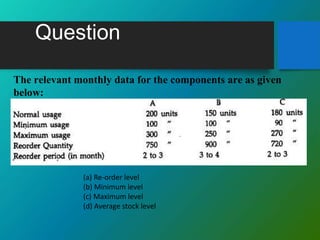

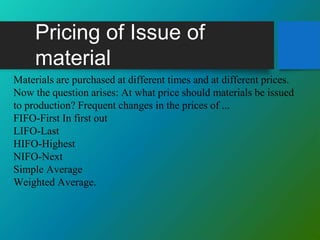

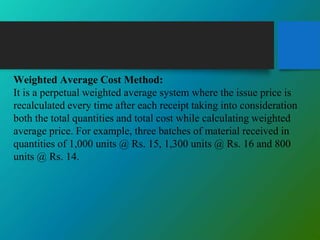

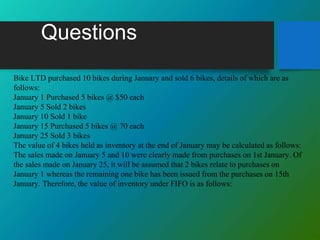

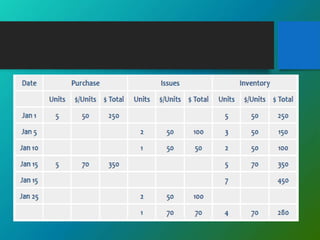

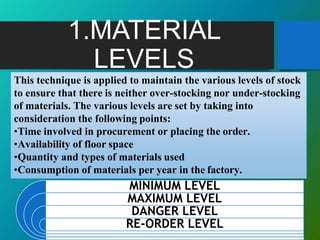

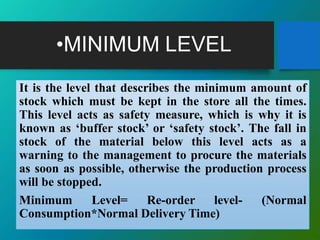

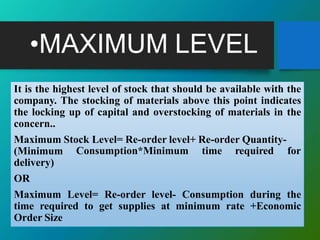

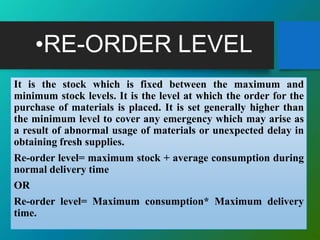

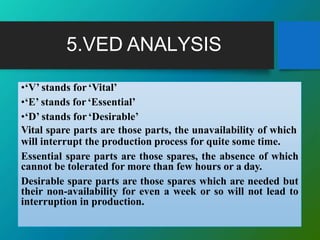

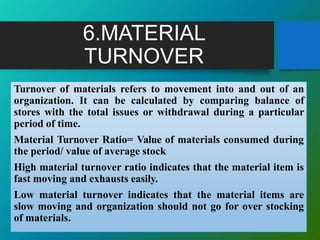

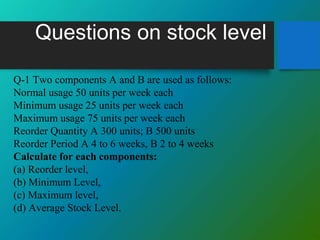

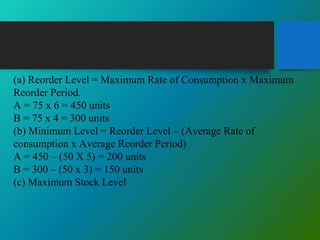

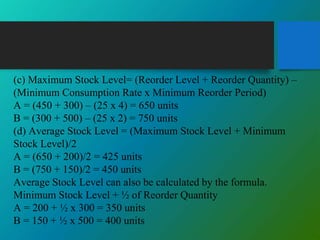

Material control is a system that ensures the efficient procurement, storage, and use of materials. It aims to provide the right quality and quantity of materials at the minimum possible cost. Key aspects of material control include establishing stock levels to prevent understocking or overstocking, using economic order quantities to minimize purchasing costs, and implementing inventory tracking systems. Techniques like ABC analysis prioritize materials based on value and VED analysis categorizes spare parts based on criticality to operations. Material control helps ensure uninterrupted production while optimizing investment in inventory.

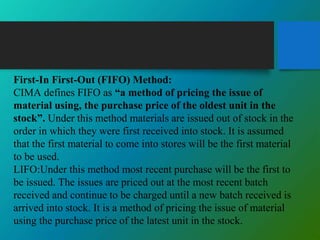

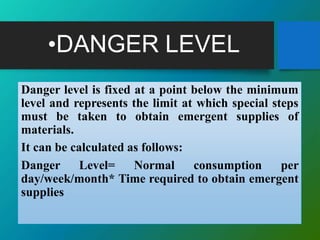

![Ordering Level

Ordering level= Maximum consumption * Lead Time [maximum]

Ordering level= 1,500 * 4

Ordering level= 6,000 Units per week](https://image.slidesharecdn.com/materialcontrol-200920094437/85/Materialcontrol-27-320.jpg)

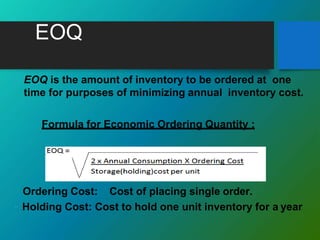

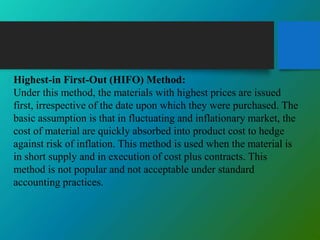

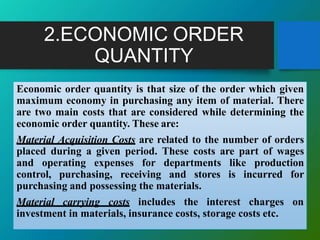

![EOQ

EOQ is also referred to as the optimum lot size. The formula to

calculate the economic order quantity (EOQ) is the square root

of [(2 times the annual demand in units times the incremental cost

to process an order) divided by (the incremental annual cost to

carry one unit in inventory)].](https://image.slidesharecdn.com/materialcontrol-200920094437/85/Materialcontrol-28-320.jpg)