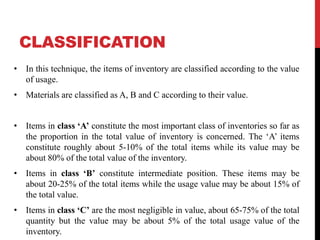

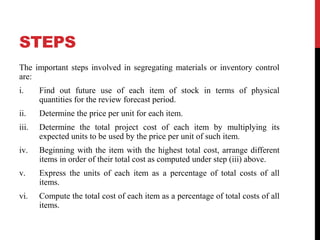

The document discusses inventory control as a critical aspect of materials management aimed at maintaining production efficiency while minimizing investment in materials. It outlines various methods, including ABC analysis, which categorizes inventory items based on their monetary value and importance, helping prioritize management efforts. The document also highlights the advantages and disadvantages of ABC analysis in controlling inventory, emphasizing effective resource allocation and potential limitations.