Downloaded 13,593 times

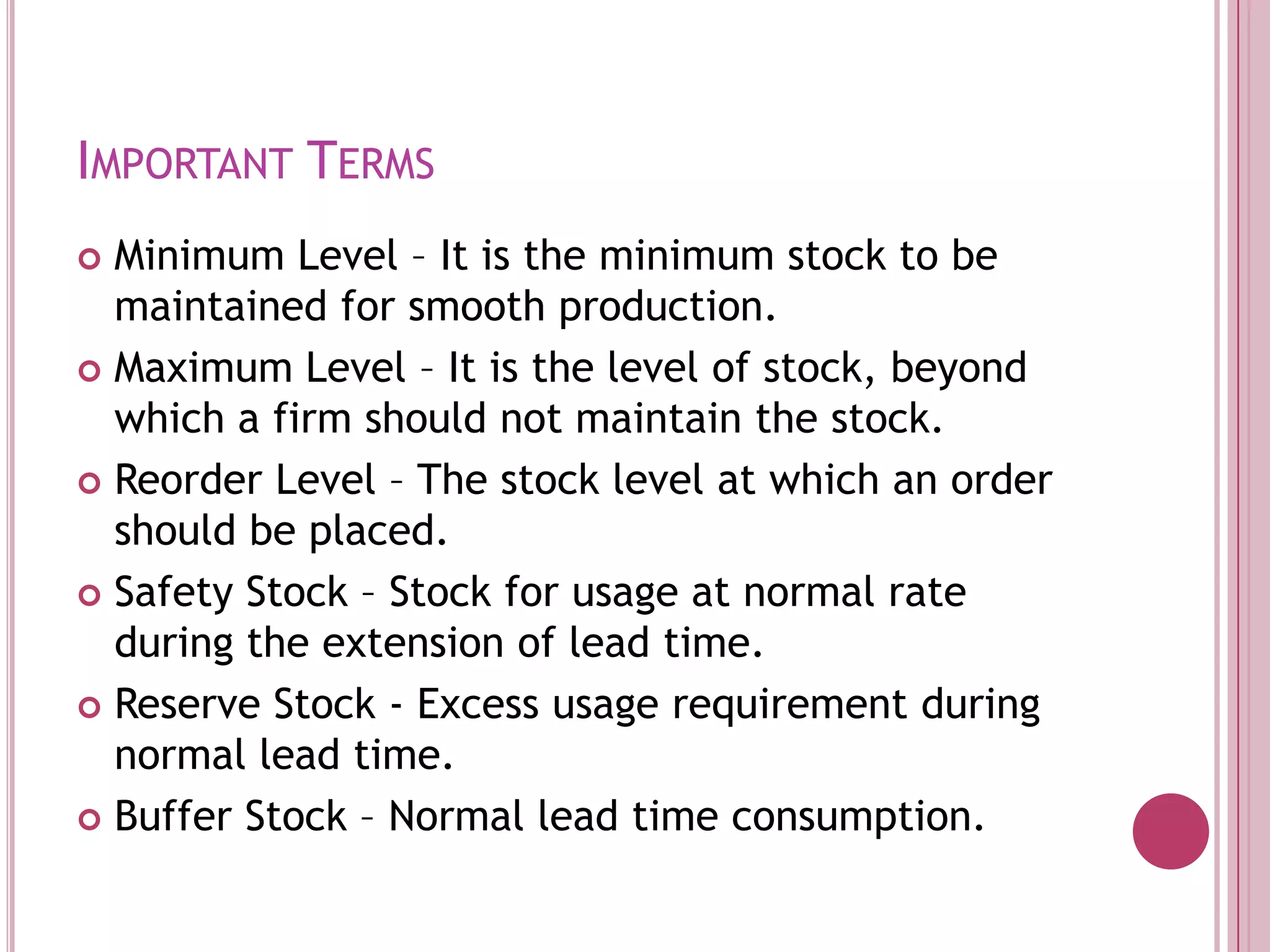

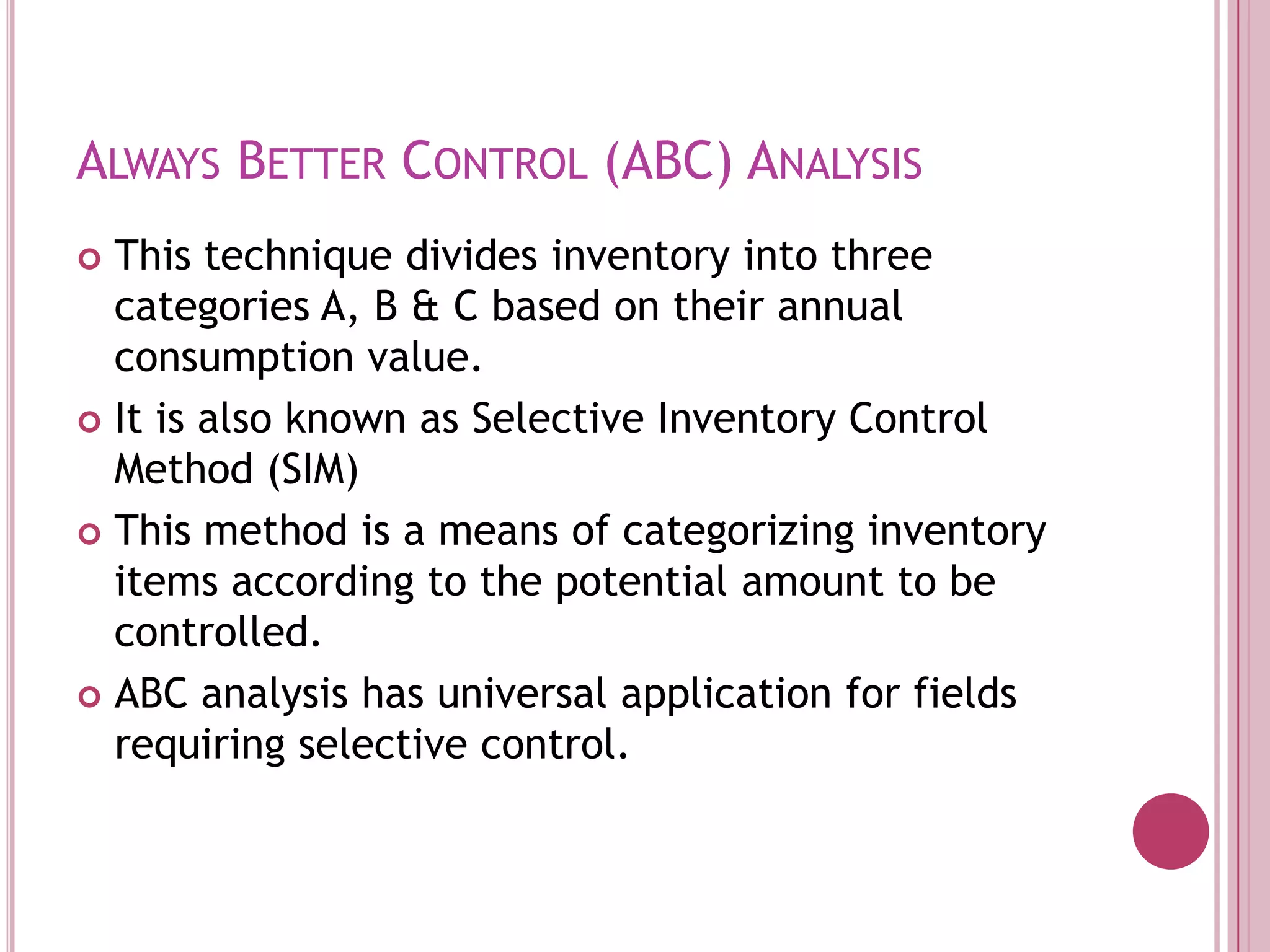

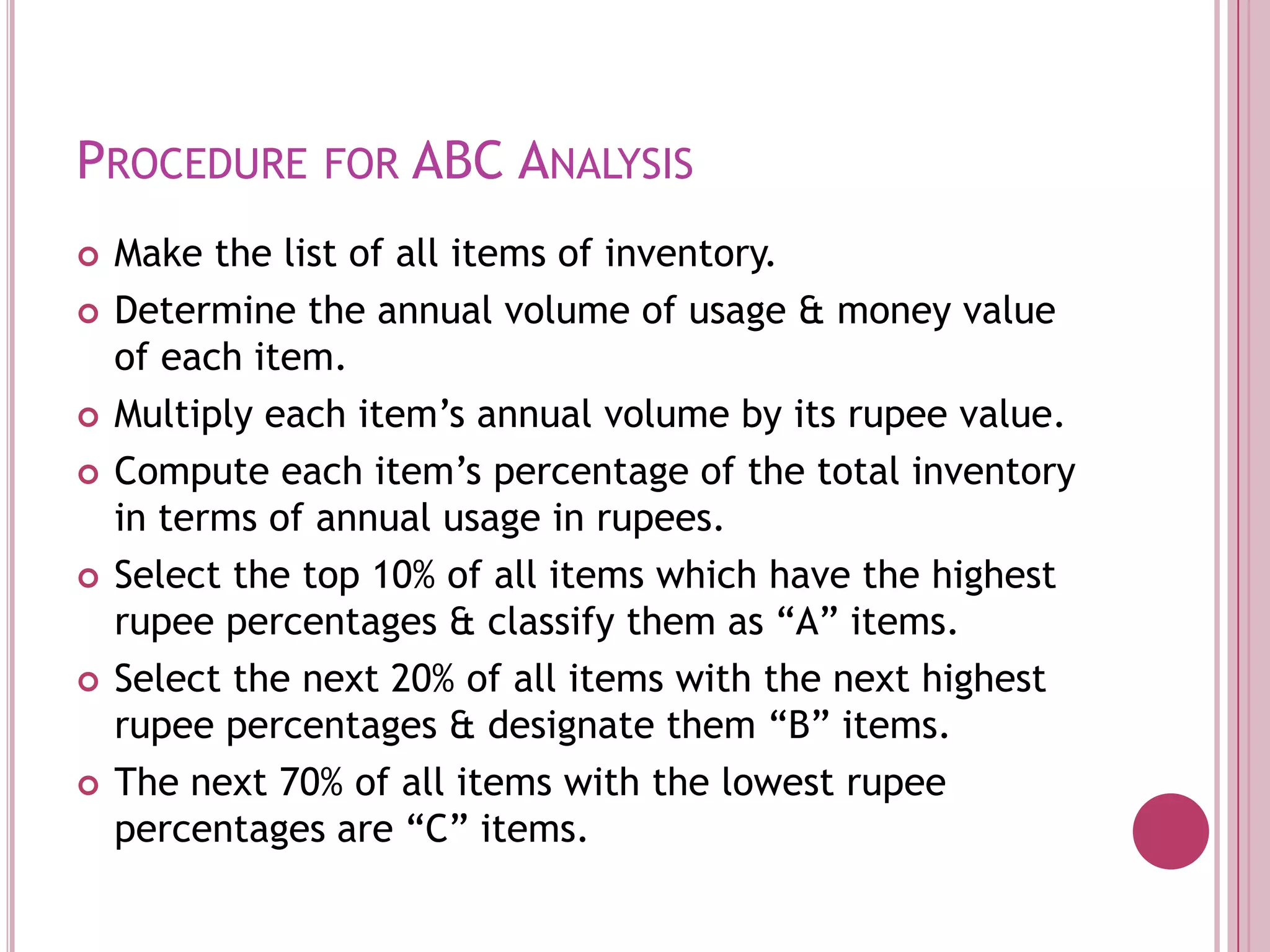

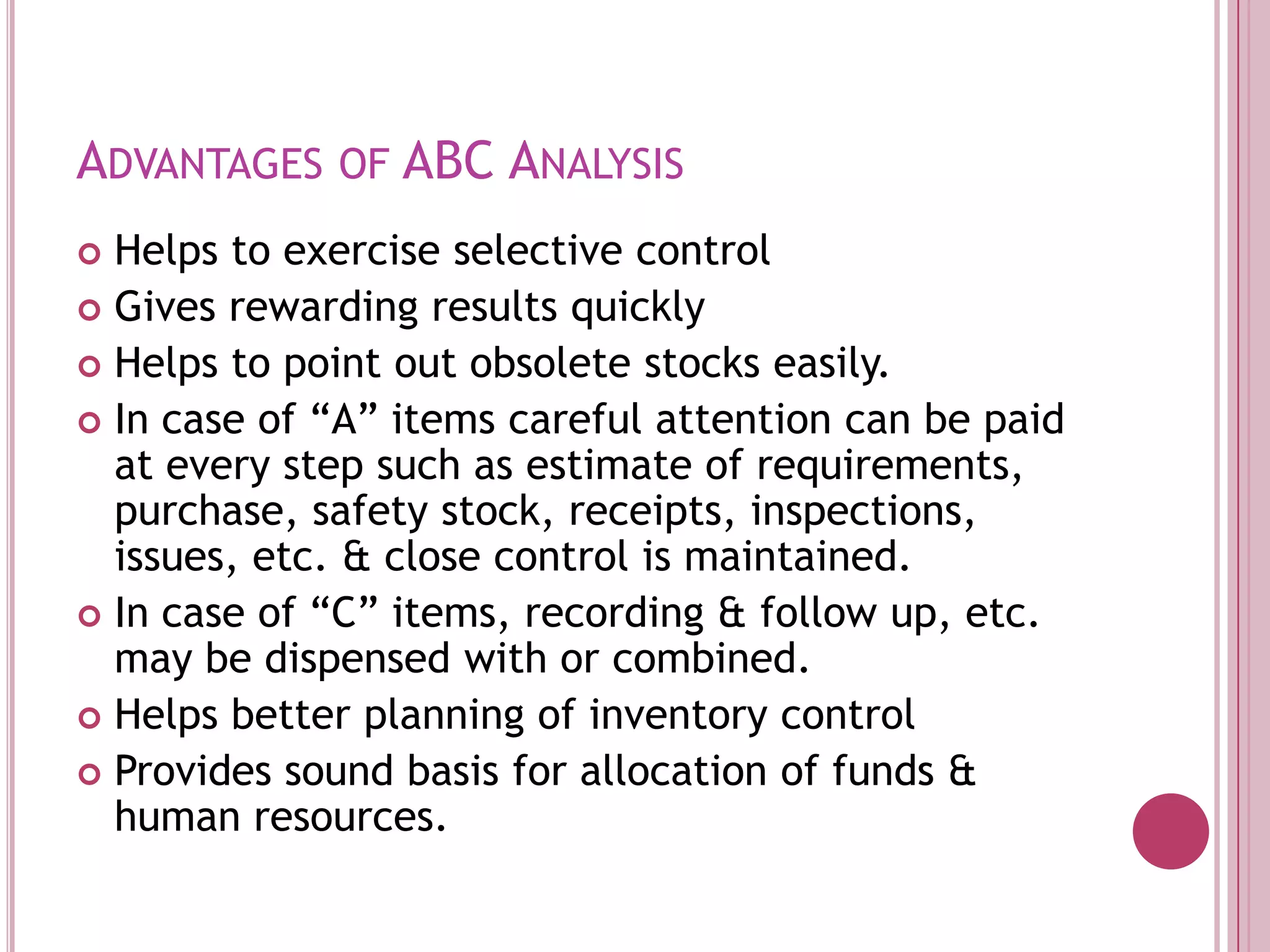

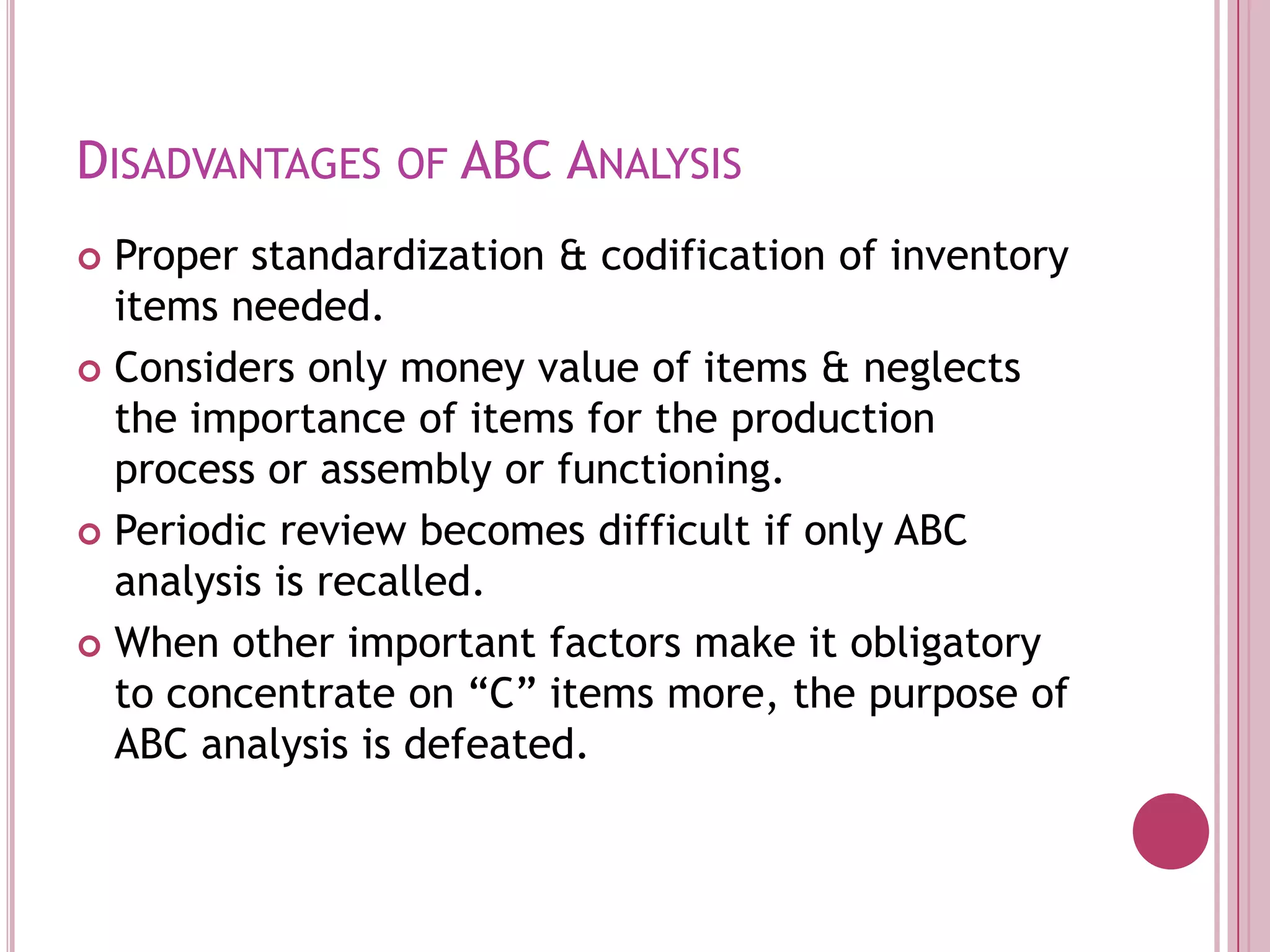

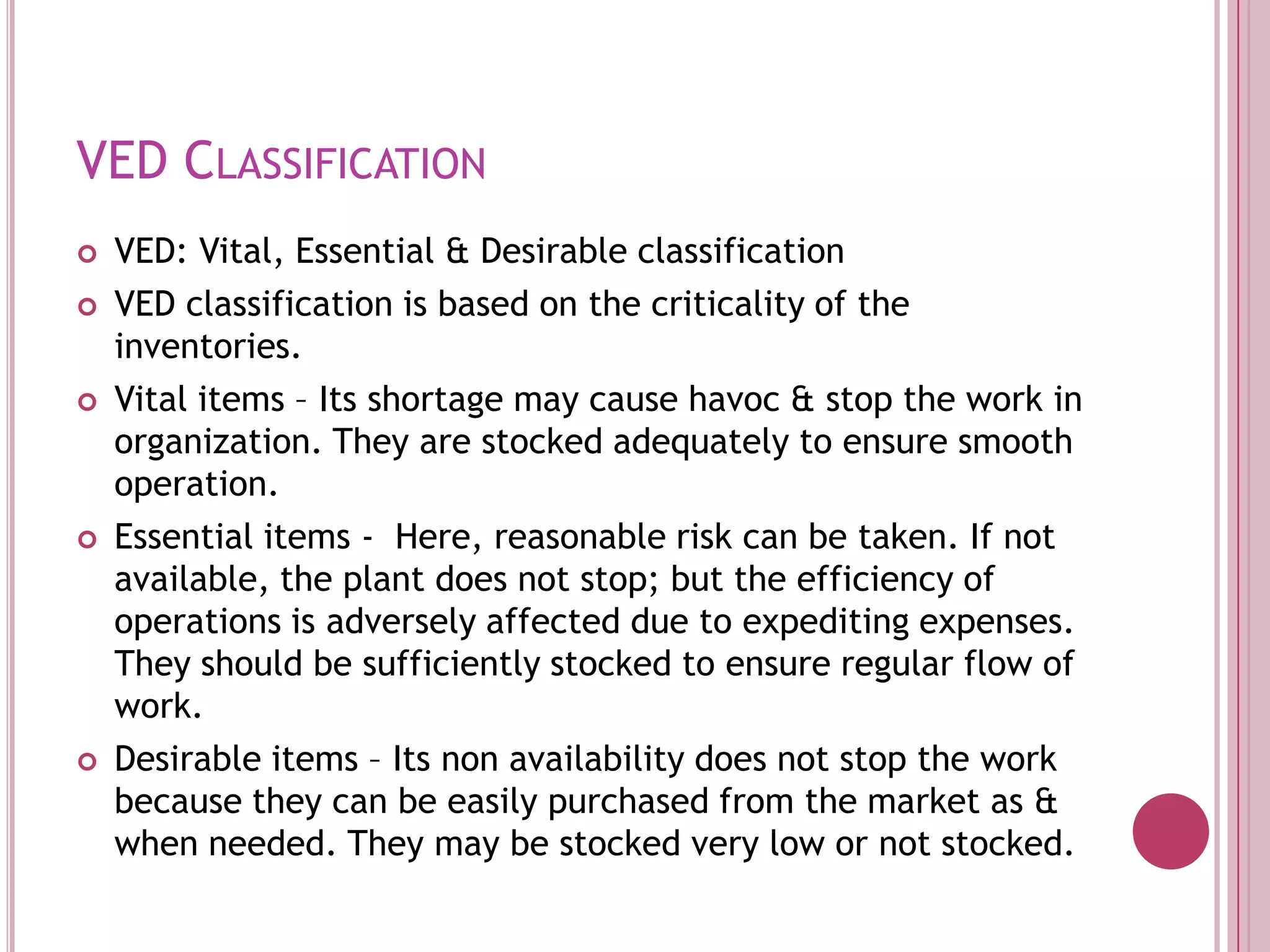

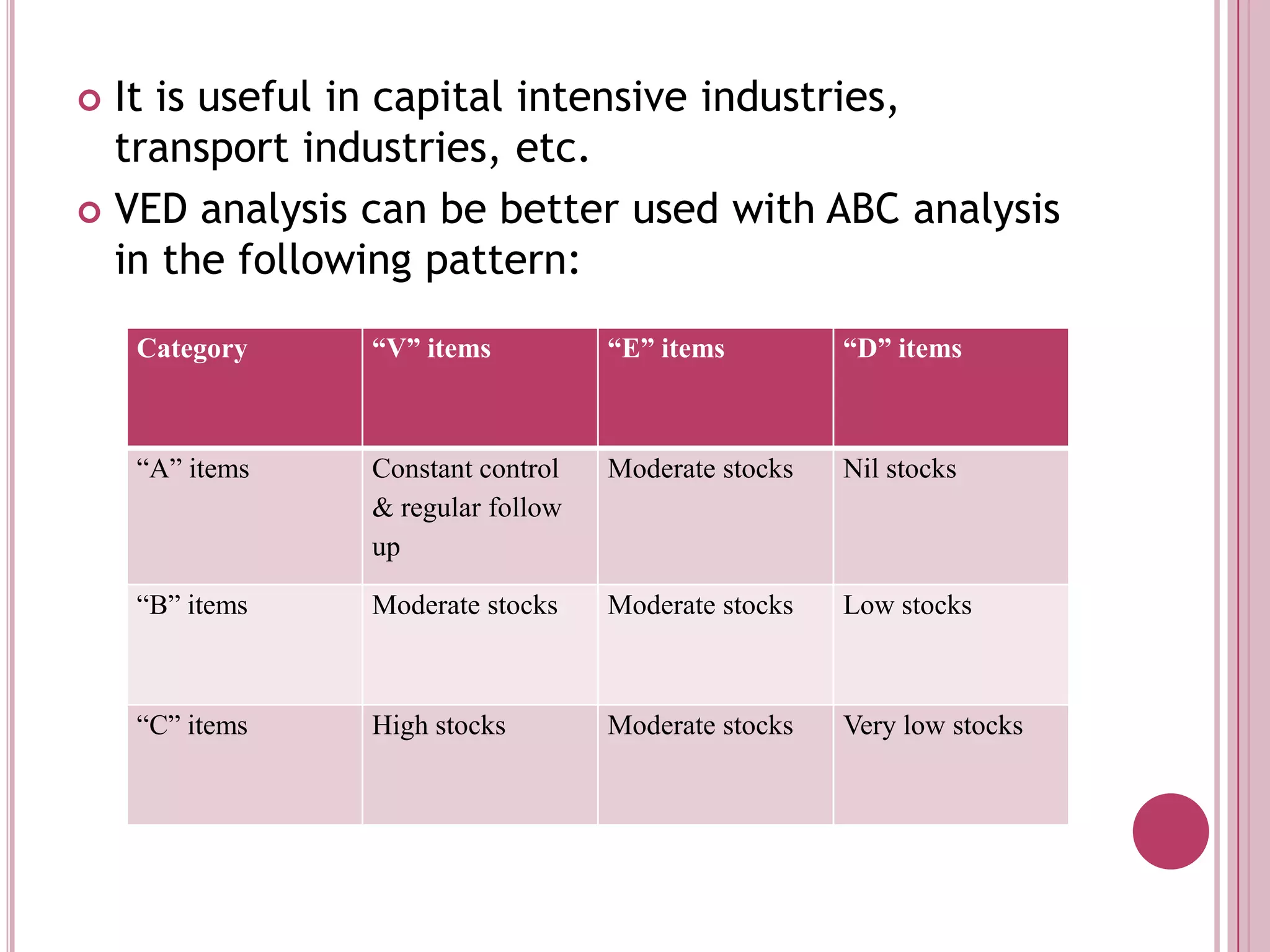

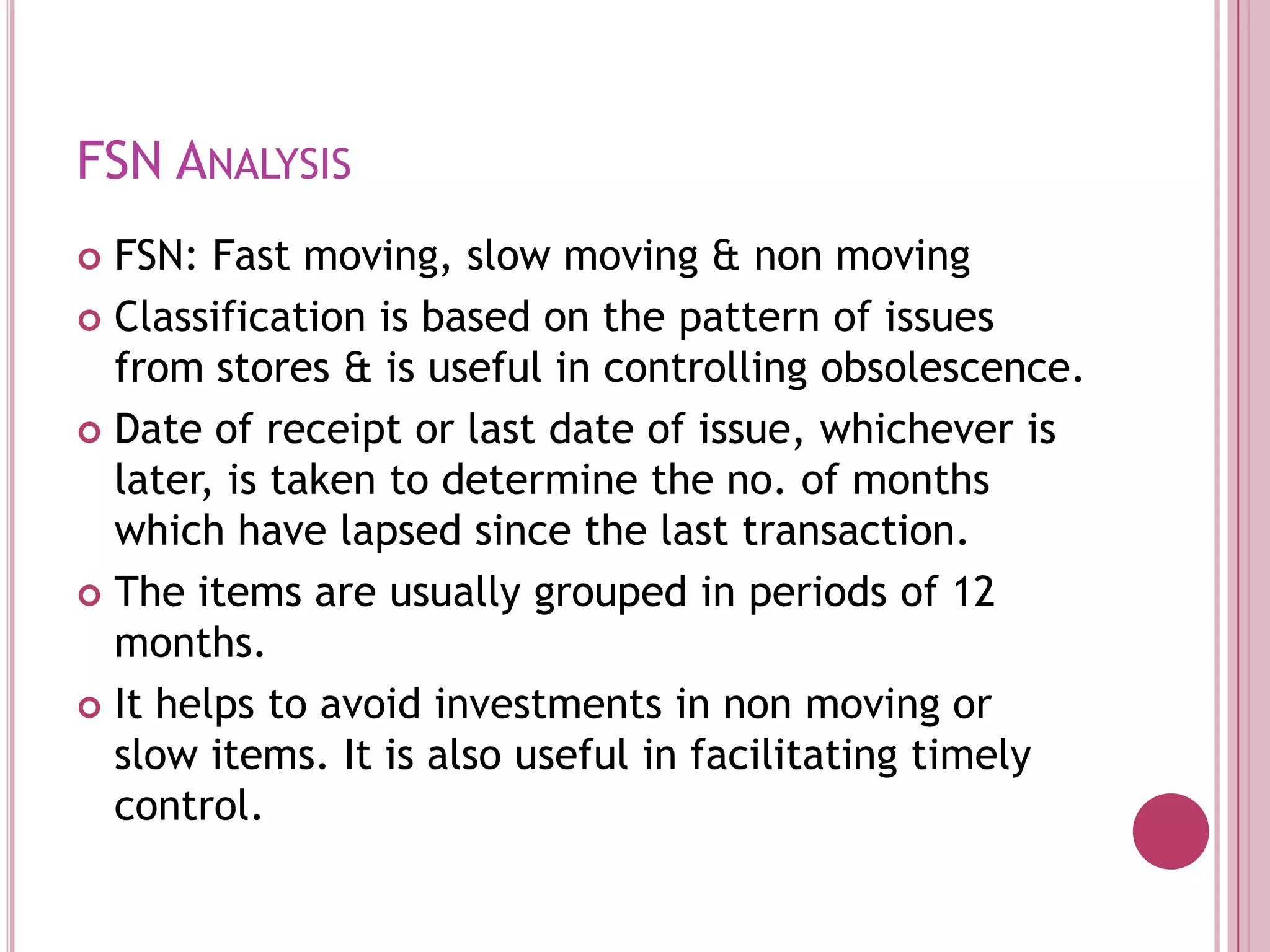

Inventory control involves regulating inventory levels according to predetermined norms to reduce costs. It aims to balance ordering, holding, and stockout costs. The ABC analysis technique categorizes inventory into A, B, and C items based on annual consumption value to focus control efforts where they are needed most. VED classification groups items as vital, essential, or desirable based on the criticality of inventory to operations. FSN analysis looks at item movement patterns to identify fast, slow, or non-moving inventory.