Downloaded 302 times

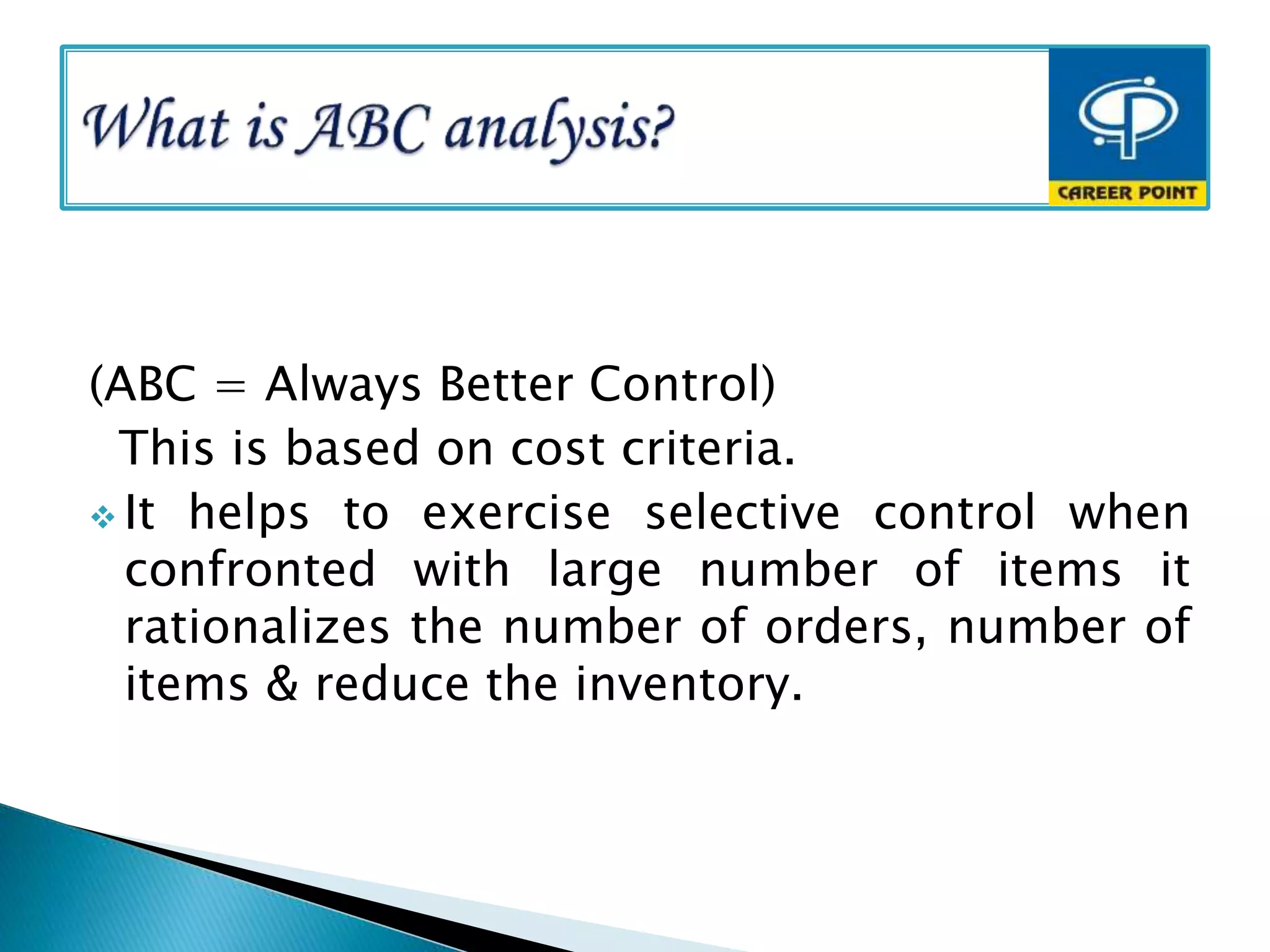

This document summarizes an operation management project on ABC analysis conducted by students for their management department. ABC analysis involves categorizing inventory items into A, B, and C categories based on their value and consumption. Category A items account for 10-25% of total items but 70-80% of total value, making them the most important to control tightly. Category B items are less important than A but more than C, while Category C items are marginally important. The analysis identifies vital few high-value items to prioritize for better inventory management and cost savings. Implementing ABC analysis' recommendations would improve the company's inventory policy and management situation.