Downloaded 38 times

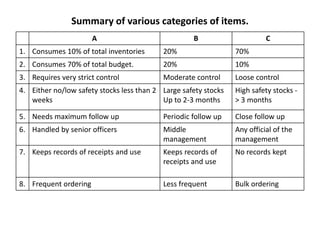

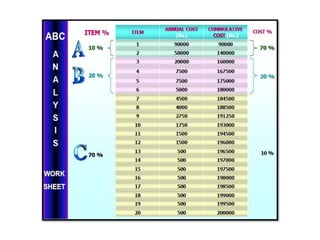

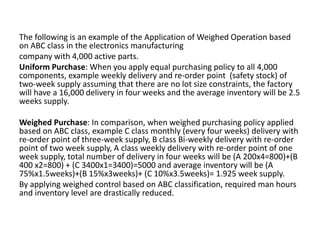

This document discusses various techniques for inventory management and control. It begins by defining inventory and classifying it into different types such as raw materials, work in process, and finished goods. It then discusses the objectives of inventory control such as protecting against demand fluctuations and improving production economics. Several techniques for controlling inventory are described, including ABC analysis, economic order quantity modeling, VED analysis, perpetual inventory systems, and reviewing slow-moving items. ABC analysis involves categorizing inventory into A, B, and C classes based on value and prioritizing control efforts accordingly. The document provides examples of how these techniques can be applied to manage inventory effectively.