Download to read offline

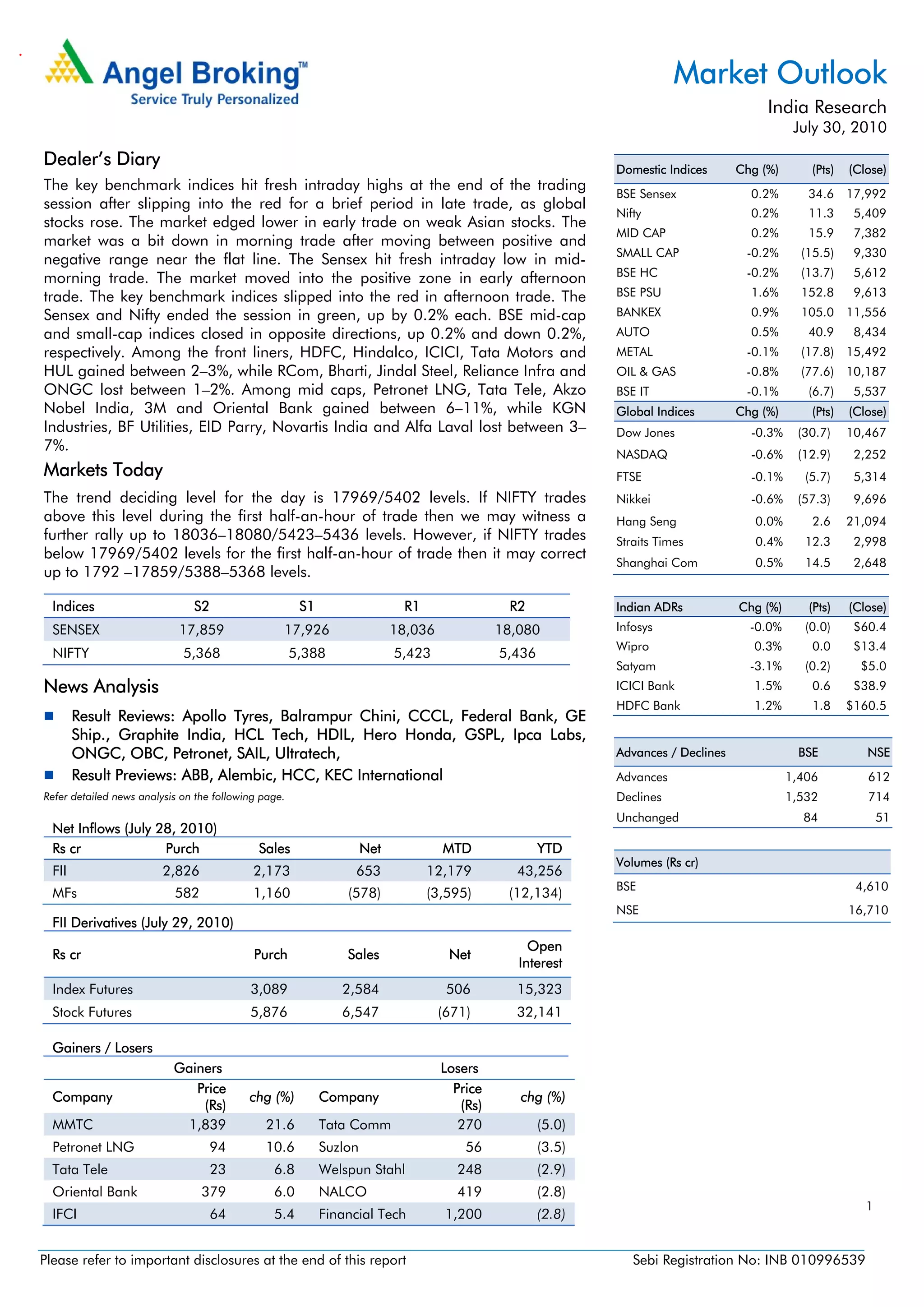

The document provides an analysis of market performance and outlook for India on July 30, 2010. It summarizes key index performance with the Sensex and Nifty ending up 0.2% each. It also reviews results from several companies and previews others. The text provides support and resistance levels for the indices and analyzes foreign institutional investor flows and derivatives.