The Triple Threat | Article on Global Resession | Harsh Kumar

Market Outlook - August 23, 2010

1. Market Outlook

India Research

August 23, 2010

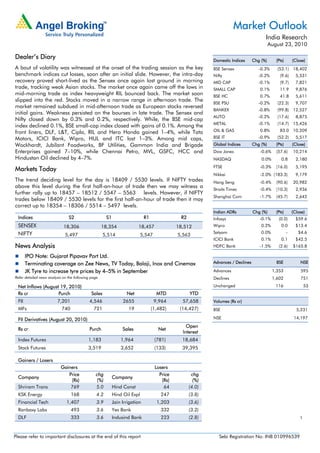

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

A bout of volatility was witnessed at the onset of the trading session as the key BSE Sensex -0.3% (53.1) 18,402

benchmark indices cut losses, soon after an initial slide. However, the intra-day Nifty -0.2% (9.6) 5,531

recovery proved short-lived as the Sensex once again lost ground in morning MID CAP -0.1% (9.7) 7,821

trade, tracking weak Asian stocks. The market once again came off the lows in SMALL CAP 0.1% 11.9 9,876

mid-morning trade as index heavyweight RIL bounced back. The market soon BSE HC 0.7% 41.8 5,611

slipped into the red. Stocks moved in a narrow range in afternoon trade. The

BSE PSU -0.2% (22.3) 9,707

market remained subdued in mid-afternoon trade as European stocks reversed

BANKEX -0.8% (99.8) 12,527

initial gains. Weakness persisted on the bourses in late trade. The Sensex and

AUTO -0.2% (17.6) 8,875

Nifty closed down by 0.3% and 0.2%, respectively. While, the BSE mid-cap

METAL -0.1% (14.7) 15,426

index declined 0.1%, BSE small-cap index closed with gains of 0.1%. Among the

front liners, DLF, L&T, Cipla, RIL and Hero Honda gained 1–4%, while Tata OIL & GAS 0.8% 83.0 10,209

Motors, ICICI Bank, Wipro, HUL and ITC lost 1–3%. Among mid caps, BSE IT -0.9% (52.2) 5,517

Wockhardt, Jubilant Foodworks, BF Utilities, Gammon India and Brigade Global Indices Chg (%) (Pts) (Close)

Enterprises gained 7–10%, while Chennai Petro, MVL, GSFC, HCC and Dow Jones -0.6% (57.6) 10,214

Hindustan Oil declined by 4–7%. NASDAQ 0.0% 0.8 2,180

FTSE -0.3% (16.0) 5,195

Markets Today

Nikkei -2.0% (183.3) 9,179

The trend deciding level for the day is 18409 / 5530 levels. If NIFTY trades Hang Seng -0.4% (90.6) 20,982

above this level during the first half-an-hour of trade then we may witness a

Straits Times -0.4% (10.3) 2,936

further rally up to 18457 – 18512 / 5547 – 5563 levels. However, if NIFTY

Shanghai Com -1.7% (45.7) 2,642

trades below 18409 / 5530 levels for the first half-an-hour of trade then it may

correct up to 18354 – 18306 / 5514 – 5497 levels.

Indian ADRs Chg (%) (Pts) (Close)

Indices S2 S1 R1 R2 Infosys -0.1% (0.0) $59.6

SENSEX 18,306 18,354 18,457 18,512 Wipro 0.2% 0.0 $13.4

NIFTY Satyam 0.0% - $4.6

5,497 5,514 5,547 5,563

ICICI Bank 0.1% 0.1 $42.5

News Analysis HDFC Bank -1.5% (2.6) $165.8

IPO Note: Gujarat Pipavav Port Ltd.

Terminating coverage on Zee News, TV Today, Balaji, Inox and Cinemax Advances / Declines BSE NSE

JK Tyre to increase tyre prices by 4–5% in September Advances 1,353 595

Refer detailed news analysis on the following page. Declines 1,602 751

Net Inflows (August 19, 2010) Unchanged 116 53

Rs cr Purch Sales Net MTD YTD

FII 7,201 4,546 2655 9,964 57,658 Volumes (Rs cr)

MFs 740 721 19 (1,482) (14,427) BSE 5,231

FII Derivatives (August 20, 2010) NSE 14,197

Open

Rs cr Purch Sales Net

Interest

Index Futures 1,183 1,964 (781) 18,684

Stock Futures 3,519 3,652 (133) 39,395

Gainers / Losers

Gainers Losers

Price chg Price chg

Company Company

(Rs) (%) (Rs) (%)

Shriram Trans 769 5.0 Hind Const 64 (4.0)

KSK Energy 168 4.2 Hind Oil Expl 247 (3.8)

Financial Tech 1,407 3.9 Jain Irrigation 1,203 (3.6)

Ranbaxy Labs 493 3.6 Yes Bank 332 (3.2)

DLF 333 3.6 Indusind Bank 223 (2.8) 1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

IPO Note: Gujarat Pipavav Port Ltd.

Gujarat Pipavav Port (GPPL) is the exclusive developer and operator of APM Terminals

Pipavav—India’s first private sector port. The company is promoted by APM Terminals

(holding 57.9% pre-issue), one of the largest container terminal operators in the world.

The port is primarily engaged in multi-cargo and multi-user operations for container, bulk

and LPG cargo.

GPPL is coming out with an IPO for Rs500cr through fresh issue of 10.4cr–11.9cr shares in

the price band of Rs42–48 per share. The issue proceeds would be utilised for prepayment

of loans, purchase of capital equipment and general corporate purpose.

Location advantages and quality infrastructure: The port is strategically located in Gujarat

(at the mouth of the Gulf of Khambhat) and provides a convenient international trade

gateway to Europe, Africa, America and the Middle East. The port offers vessel acceptance

draught of 14.5 meters, which allows navigation for bulk vessels of ~81,600 MT and

container vessels of 6,200 TEU capacities. The company owns 38.8% in a joint venture

with Indian Railways, viz. Pipavav Railways Corporation (PRCL), providing rail connectivity

to industrialised hinterland and is connected by 10km road to NH-8E.

Expensive valuations justified by substantial growth potential: At the lower band of Rs42,

GPPL commands 2.5x CY2011E P/BV, a premium to its global peers, which trade at an

average P/BV of 2.0x. However, it is at a substantial discount to the Mundra port, which

trades at 5.9x FY2012E P/BV, which we believe is justified given the latter’s larger scale,

revenue contribution from its SEZ and higher profitability growth. However, over the last

couple of years, GPPL has exhibited strong growth rates at the operating level following an

improvement in utilisation levels and growing traffic. GPPL also expects to retire high-cost

debt utilising Rs300cr from the issue proceeds resulting in reduction in interest expenses

from Rs115cr in CY2009 to Rs92cr in CY2011E. Consequently, we expect GPPL to report

profit from CY2011E. Further, management has indicated to hike container tariffs in line

with market dynamics with re-negotiation of contracts from CY2010. Consequently, we

expect GPPL to report profit from CY2011E. We recommend Subscribe to the IPO at the

lower price band with a long-term perspective.

Terminating coverage on Zee News, TV Today, Balaji, Inox and Cinemax

Due to the re-alignment of our coverage universe, we are terminating coverage on

Zee News, TV Today, Balaji Telefilms, Inox and Cinemax India. Effective the coverage

termination, the last rating issued for these stocks should not be relied upon going

forward.

JK Tyre to increase tyre prices by 4–5% in September

JK Tyre is set to increase its products prices by 4–5% in the first week of September to offset

rising input costs. The price hike comes on the back of the ~3% increase in tyre prices by

the company in July. In 1QFY2011, natural rubber prices witnessed a steep increase (up

~70% yoy), and continue to inch upwards. Currently, the prices are ruling around Rs180–

185/kg. With the increase in prices set to happen in September, the company intends to

protect its margins and offset the cost pressure on the raw-material front. On the utilisation

front, JK Tyre is operating at the 95–96% level, buoyed by robust demand from OE

makers. At the CMP of Rs175, JK Tyre is available at attractive valuations of 4.4x and 3.7x

FY2011E and FY2012E EPS, respectively. We maintain a Buy rating on the stock with a

Target Price of Rs238, at which level the stock would trade at 5x, 3.3x and 0.8x FY2012E

EPS, EV/EBITDA and P/BV, respectively.

August 23, 2010 2

3. Market Outlook | India Research

Economic and Political News

GST set to miss April 2011 deadline as the bill will not be introduced in the parliament

DTC may moderate tax rates: CBDT Chairman

Orissa to move apex court over POSCO project

Apparel exporters ask government to provide more sops in FTP

Forex reserves down by US $4.6bn to US $282.8bn for the week ending August 13

FICCI demands additional duty sops for steel exports

Corporate News

JSPL resumes implementation of steel and iron ore mine project in Bolivia

BPCL buys stake in Australian shale gas fields

Tata Steel to invest Rs1,000cr in Orissa plants

Cairn-Vedanta deal may not get ministry’s approval

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

GEI Ind Dividend, Results

Prime Focus Results, Stock Split

August 23, 2010 3

4. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

August 23, 2010 4