1. .

Market Outlook

India Research

August 11, 2010

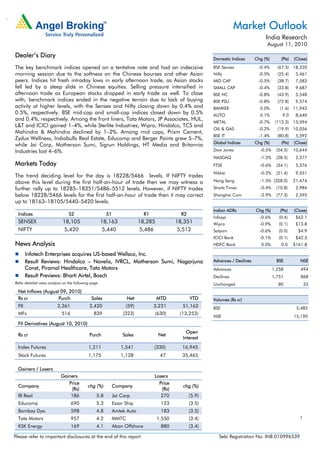

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The key benchmark indices opened on a tentative note and had an indecisive BSE Sensex -0.4% (67.5) 18,220

morning session due to the softness on the Chinese bourses and other Asian Nifty -0.5% (25.4) 5,461

peers. Indices hit fresh intraday lows in early afternoon trade, as Asian stocks MID CAP -0.5% (38.7) 7,583

fell led by a steep slide in Chinese equities. Selling pressure intensified in SMALL CAP -0.4% (33.8) 9,687

afternoon trade as European stocks dropped in early trade as well. To close BSE HC -0.8% (43.9) 5,548

with, benchmark indices ended in the negative terrain due to lack of buying BSE PSU -0.8% (72.8) 9,574

activity at higher levels, with the Sensex and Nifty closing down by 0.4% and BANKEX 0.0% (1.6) 11,943

0.5%, respectively. BSE mid-cap and small-cap indices closed down by 0.5% AUTO 0.1% 9.0 8,640

and 0.4%, respectively. Among the front liners, Tata Motors, JP Associates, HUL,

METAL -0.7% (112.3) 15,594

L&T and ICICI gained 1–4%, while Sterlite Industries, Wipro, Hindalco, TCS and

OIL & GAS -0.2% (19.9) 10,056

Mahindra & Mahindra declined by 1–2%. Among mid caps, Prism Cement,

BSE IT -1.4% (80.8) 5,592

Zydus Wellness, Indiabulls Real Estate, Educomp and Berger Paints grew 5–7%,

Global Indices Chg (%) (Pts) (Close)

while Jai Corp, Motherson Sumi, Sigrun Holdings, HT Media and Britannia

Industries lost 4–6%. Dow Jones -0.5% (54.5) 10,644

NASDAQ -1.2% (28.5) 2,277

Markets Today FTSE -0.6% (34.1) 5,376

Nikkei -0.2% (21.4) 9,551

The trend deciding level for the day is 18228/5466 levels. If NIFTY trades

above this level during the first half-an-hour of trade then we may witness a Hang Seng -1.5% (328.0) 21,474

further rally up to 18285–18351/5486–5512 levels. However, if NIFTY trades Straits Times -0.4% (10.8) 2,984

below 18228/5466 levels for the first half-an-hour of trade then it may correct Shanghai Com -2.9% (77.3) 2,595

up to 18163–18105/5440–5420 levels.

Indian ADRs Chg (%) (Pts) (Close)

Indices S2 S1 R1 R2

Infosys -0.6% (0.4) $62.1

SENSEX 18,105 18,163 18,285 18,351 Wipro -0.9% (0.1) $13.8

NIFTY 5,420 5,440 5,486 5,512 Satyam -0.6% (0.0) $4.9

ICICI Bank -0.1% (0.1) $42.3

News Analysis HDFC Bank 0.0% 0.0 $161.8

Infotech Enterprises acquires US-based Wellsco, Inc.

Result Reviews: Hindalco – Novelis, IVRCL, Motherson Sumi, Nagarjuna Advances / Declines BSE NSE

Const, Piramal Healthcare, Tata Motors Advances 1,258 494

Result Previews: Bharti Airtel, Bosch Declines 1,751 868

Refer detailed news analysis on the following page. Unchanged 80 33

Net Inflows (August 09, 2010)

Rs cr Purch Sales Net MTD YTD Volumes (Rs cr)

FII 2,361 2,420 (59) 3,221 51,162 BSE 5,485

MFs 516 839 (323) (630) (13,253)

NSE 15,190

FII Derivatives (August 10, 2010)

Open

Rs cr Purch Sales Net

Interest

Index Futures 1,211 1,541 (330) 16,945

Stock Futures 1,175 1,128 47 35,465

Gainers / Losers

Gainers Losers

Price Price

Company chg (%) Company chg (%)

(Rs) (Rs)

IB Real 186 5.8 Jai Corp 270 (5.9)

Educomp 690 5.3 Essar Ship 123 (3.5)

Bombay Dye. 598 4.8 Amtek Auto 183 (3.5)

Tata Motors 957 4.2 MMTC 1,550 (3.4) 1

KSK Energy 169 4.1 Aban Offshore 880 (3.4)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

Infotech Enterprises acquires US-based Wellsco, Inc. in an all-cash deal

Infotech Enterprises (Infotech) has acquired Arkansas-based Wellsco, Inc. (Wellsco) in an

all-cash deal. Wellsco provides network engineering and management services to the

telecommunications (Telco) industry. Wellsco has 180 professionals working across five

offices in the US.

Infotech has not disclosed the consideration amount but has guided that the consideration

value paid is lower than 1x of Wellsco’s annual revenue. Out of the total consideration

amount, 85% is already paid in cash, while the remaining would be paid-off by Infotech in

the form of earn-outs, depending on the financial performance of Wellsco in the next six

months. The current annual revenue run rate of Wellsco is US $12mn, which would result

in annual revenue contribution of US $8mn for Infotech in FY2011, while the current

EBITDA margin of Wellsco is in the 7–10% range. The acquisition is expected to be

earnings accretive. Currently, the addressable market size of the Telco engineering services

sector in the US stands at US $20bn, of which the market size of the designing and

planning work, where Wellsco has a strong presence stands at US $2.5bn. Thus, through

this acquisition, Infotech plans to explore and scale up on this huge opportunity.

This acquisition would also result in improved volume-led growth in the company’s UTG

vertical, which has been witnessing subdued growth in the past couple of quarters. After

the acquisition, Infotech would execute work from offshore compared to the complete

onshore delivery currently being done by Wellsco. Going forward, this is expected to result

in an improvement in Wellsco’s EBITDA margin.

The acquisition is in line with Infotech’s inorganic growth strategy. Going forward, we

expect the company to continue to scout for such acquisitions, which are of a strategic fit,

as it would help it gain further domain expertise for seizing any upcoming opportunities.

Through this strategy, the company also aims to add and grow its marquee client accounts

across geographies and verticals, thereby expanding its operations. At the current level,

we recommend Buy on the stock with a Target Price of Rs192.

Result Reviews – 1QFY2011

Hindalco – Novelis

Novelis, Hindalco’s subsidiary, reported strong set of numbers for 1QFY2011. The top line

grew 29.2% yoy and 4.7% qoq to US $2,533mn as shipments of rolled products increased

by 14.8% yoy and 4.2% qoq to 746kt. Adjusted EBITDA grew by 112.1% yoy and 13.9%

qoq to US $263mn. Net income decreased by 65% yoy to US $50mn. Following the expiry

of Novelis’s metal price ceiling contracts and the expected benefit from price increases and

cost savings measures, we maintain our Buy recommendation on the stock with a Target

Price of Rs204.

IVRCL Infrastructure

For 1QFY2011, IVRCL Infrastructure (IVRCL) posted a flat top line at Rs1,106cr, which was

19.1% below our expectations. The company lost revenue of around Rs250cr for the

quarter on account of its projects in MP and AP along with its IOC tankage project. On the

operating front, the company posted margin of 9.1% against our estimate of 8.6%. Below-

estimate top-line performance cascaded at the bottom-line level, which came in at mere

Rs28.1cr. The order inflow for the quarter stood at Rs3,174cr, whereas the outstanding

order book stood tall at Rs23,275cr (4.3x FY2010 revenue). The management continues to

maintain its FY2011 top-line guidance in the Rs6,700cr–Rs7,100cr range. However, we

have marginally pruned our numbers, which are below the management’s guidance. We

believe the current valuations provide a good entry point for long-term investors. Hence,

we maintain a Buy rating on IVRCL with a Target Price of Rs216.

August 11, 2010 2

3. Market Outlook | India Research

Motherson Sumi Systems

For 1QFY2011, Motherson Sumi Systems (MSSL) registered 32% yoy growth in net sales to

Rs1,905cr (Rs1,442cr), which was below our expectations. Sales growth was largely aided

by the 53% yoy jump in domestic market revenue at Rs630cr and a 24% yoy increase in

revenue from outside India at Rs1,229cr. However, the sequential decline in Samvardhana

Motherson Reflectec’s (SMR) revenue arrested revenue growth during the quarter.

On the operating front, the company reported a 370bp yoy increase in EBITDA margin to

9.8%, lower than our expectation of 11.6%. Operating margin also came in below our

expectation, largely due to the sequential increase in overall input costs and lower-than-

expected margin of SMR at 7.2% (8.7% in 4QFY2010). On a sequential basis, margin fell

by 508bp qoq. The adverse currency movement also impacted operating performance

during the quarter. Thus, net profit for the quarter came in below our expectation at

Rs60cr, largely on account of lower-than-expected top-line growth and operating margin.

Further, higher tax rate for 1QFY2011 restricted net profit growth for the quarter.

We will be revising our estimates and rating post the management’s conference call.

However, we maintain our positive stand on the company, considering its fundamental

track record and business portfolio. The stock rating is under review.

Nagarjuna Construction

Nagarjuna Construction (NCC) posted disappointing numbers for 1QFY2011. The major

disappointment came in from the top-line front, which grew by mere 8.5% against our

expectations of 27.4%. However, the management has maintained its guidance of

Rs5,800cr for the year. Operating margin for the quarter came in at 9.7% (10.4%), in line

with our estimates. NCC managed to save on the interest cost front due to low short-term

borrowings rate and as interest costs witnessed a sequential decline in spite of increasing

debt. NCC is well placed to leverage the opportunity in the infrastructure space with one of

the most diversified order books and exposure to most of the growth sectors—

transportation, water and power. We maintain a Buy rating on the stock with a Target Price

of Rs201.

Piramal Healthcare

Piramal Healthcare (PHL) reported its 1QFY2011 results, which were below our estimates

on the back of subdued domestic formulation business. The company reported net sales of

Rs842cr (Rs821cr), up by mere 2.6% yoy. Domestic formulation sales grew by 4.9% to

Rs461cr (Rs440cr), mainly affected by the sale of the business to Abbott. Further, the

CRAMS segment remained lackluster at Rs175cr (Rs190cr), down 8.0% yoy; however, the

critical care segment grew by 48.6% yoy to Rs108cr (Rs72.8cr) on the back of higher

contribution from Minrad. The company also disappointed on the operating front, with

OPM at 15.3% (18.9%), a contraction of 360bp yoy on the back of higher employee

expenses and cost pertaining to the Abbott deal. PHL reported net profit of Rs80.7cr

(Rs85.0cr), down 5.3% yoy, impacted by subdued growth on the top-line front. On the

Abbott deal, the company expects the proceeds (US $2.1bn) to come by September end.

We recommend a Neutral rating on the stock at the current level, given the uncertainty

over the usage of funds.

August 11, 2010 3

4. Market Outlook | India Research

Tata Motors

Tata Motors posted an outstanding performance for 1QFY2011, on the back of improved

operational performance at JLR and other key subsidiaries of the company. On a

standalone basis, the company reported 63% yoy growth in the top line, aided by 48% yoy

growth in volumes and 10.5% growth in realisations. Operating margin stood at 11.1%,

driven by better operating leverage and a yoy decline in input costs. However, net profit

declined 23% yoy to Rs396cr due to lower other income of Rs69cr (Rs319cr).

On a consolidated basis, net revenue grew 65% yoy to Rs27,056cr, aided by higher

growth in domestic and JLR volumes and a substantial 27% yoy jump in JLR realisations.

Volumes at JLR increased by 59% yoy. On the operating front, margin increased by

1,118bp yoy and 343bp qoq to 14.2% for 1QFY2011. Favorable currency movement and

restructuring efforts at JLR helped to improve the margin at consolidated levels. Net profit

for the quarter stood at Rs1,979cr, as against net loss of Rs334cr in 1QFY2010.

We maintain our positive stance on the company, considering its impressive 1QFY2011

performance. We will be revising our estimates upwards (largely on the JLR front) and

would shortly release a detailed update on the company. The stock rating is under review.

Result Previews – 1QFY2011

Bharti Airtel

For 1QFY2011, we expect Bharti Airtel to report a 5.1% yoy (3.9% qoq) increase in net

revenue to Rs10,450cr. Growth is expected to be driven by the mobile services business, as

net subscribers are expected to grow by 6.6% qoq and 33% yoy to 136mn. However,

higher network expansion costs and a decline in tariffs are expected to impact margins by

480bp yoy (100bp qoq). However, the bottom line is expected to decline by 22% yoy (4.5%

qoq) to Rs1,962cr. At the current level, we maintain an Accumulate rating on the stock with

a Target Price of Rs360.

Bosch – 2QCY2010

Bosch is slated to announce its 2QCY2010 results. The company is expected to deliver

33% yoy growth in revenue to Rs1,628cr for the quarter. On the operating front, Bosch is

expected to post a 119bp yoy improvement in operating profit margin to 18.7%. Net profit

is expected to increase by 9.6% yoy to Rs209.3cr. The stock rating is under review.

August 11, 2010 4

5. Market Outlook | India Research

Economic and Political News

High Court asks SEBI to decide on MCX-SX plea by September 30

Rajasthan government to take a 26% stake in ONGC’s Barmer refinery

18 foreign banks apply for branches, representative offices: Jr. Fin. Min. NN Meena

Corporate News

M&M, Ruia submit bids for Ssangyong

Uttam Galva increases prices by Rs500 a tonne

GMR Infra gets US $1bn offer for InterGen stake

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Bajaj Hindustan Results

Bajaj Hindustan Sugar Results

Bharti Airtel Results

Bosch Results

Everonn Results

Financial Tech Results

Jindal Poly Results

Parsvnath Developers Results

Sundaram Fasteners Results

Tamilnadu Petroproducts Results

Tips Inds Results

Videocon Inds Results

West Coast Paper Results

August 11, 2010 5

6. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

August 11, 2010 6