Solution Manual for Principles of Corporate Finance 14th Edition by Richard B...

Market outlook 20.10.10

1. Market Outlook

India Research

October 20, 2010

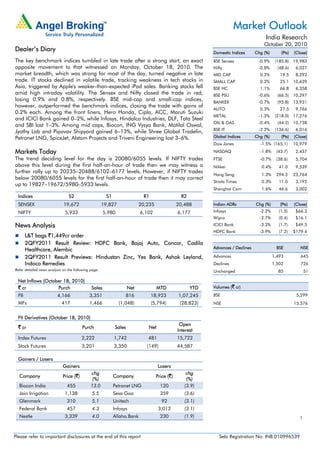

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The key benchmark indices tumbled in late trade after a strong start, an exact BSE Sensex -0.9% (185.8) 19,983

opposite movement to that witnessed on Monday, October 18, 2010. The Nifty -0.8% (48.6) 6,027

market breadth, which was strong for most of the day, turned negative in late MID CAP 0.2% 19.5 8,292

trade. IT stocks declined in volatile trade, tracking weakness in tech stocks in SMALL CAP 0.2% 25.1 10,639

Asia, triggered by Apple's weaker-than-expected iPad sales. Banking stocks fell BSE HC 1.1% 66.8 6,358

amid high intraday volatility. The Sensex and Nifty closed the trade in red, BSE PSU -0.6% (66.5) 10,297

losing 0.9% and 0.8%, respectively. BSE mid-cap and small-cap indices, BANKEX -0.7% (95.8) 13,931

however, outperformed the benchmark indices, closing the trade with gains of

AUTO 0.3% 27.5 9,766

0.2% each. Among the front liners, Hero Honda, Cipla, ACC, Maruti Suzuki

METAL -1.3% (218.0) 17,276

and ICICI Bank gained 0–2%, while Infosys, Hindalco Industries, DLF, Tata Steel

OIL & GAS -0.4% (44.2) 10,738

and SBI lost 1–3%. Among mid caps, Biocon, ING Vysya Bank, Motilal Oswal,

BSE IT -2.2% (136.6) 6,016

Jyothy Lab and Pipavav Shipyard gained 6–13%, while Shree Global Tradefin,

Petronet LNG, SpiceJet, Alstom Projects and Triveni Engineering lost 3–6%. Global Indices Chg (%) (Pts) (Close)

Dow Jones -1.5% (165.1) 10,979

Markets Today NASDAQ -1.8% (43.7) 2,437

The trend deciding level for the day is 20080/6055 levels. If NIFTY trades FTSE -0.7% (38.6) 5,704

above this level during the first half-an-hour of trade then we may witness a Nikkei 0.4% 41.0 9,539

further rally up to 20235–20488/6102–6177 levels. However, if NIFTY trades

Hang Seng 1.3% 294.3 23,764

below 20080/6055 levels for the first half-an-hour of trade then it may correct

Straits Times 0.3% 11.0 3,192

up to 19827–19672/5980–5933 levels.

Shanghai Com 1.6% 46.6 3,002

Indices S2 S1 R1 R2

SENSEX 19,672 19,827 20,235 20,488 Indian ADRs Chg (%) (Pts) (Close)

NIFTY 5,933 5,980 6,102 6,177 Infosys -2.2% (1.5) $66.3

Wipro -2.7% (0.4) $16.1

News Analysis ICICI Bank -3.3% (1.7) $49.5

HDFC Bank -3.9% (7.2) $179.4

L&T bags `1,449cr order

2QFY2011 Result Review: HDFC Bank, Bajaj Auto, Concor, Cadila

Healthcare, Alembic Advances / Declines BSE NSE

2QFY2011 Result Previews: Hindustan Zinc, Yes Bank, Ashok Leyland, Advances 1,493 645

Indoco Remedies Declines 1,502 726

Refer detailed news analysis on the following page. Unchanged 85 51

Net Inflows (October 18, 2010)

` cr Purch Sales Net MTD YTD Volumes (` cr)

FII 4,166 3,351 816 18,923 1,07,245 BSE 5,299

MFs 417 1,466 (1,048) (5,794) (28,823) NSE 15,576

FII Derivatives (October 18, 2010)

Open

` cr Purch Sales Net

Interest

Index Futures 2,222 1,742 481 15,722

Stock Futures 3,201 3,350 (149) 44,587

Gainers / Losers

Gainers Losers

chg chg

Company Price (`) Company Price (`)

(%) (%)

Biocon India 455 13.0 Petronet LNG 120 (3.9)

Jain Irrigation 1,138 5.5 Sesa Goa 359 (3.6)

Glenmark 310 5.1 Unitech 92 (3.1)

Federal Bank 457 4.3 Infosys 3,012 (3.1)

Nestle 3,339 4.0 Allaha.Bank 230 (1.9) 1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

L&T bags `1,449cr order

Larsen & Toubro (L&T) has bagged an order valued at `1,449cr from DB Power Limited,

promoted by the Bhaskar Group. L&T will execute the complete Balance of Plant (BOP)

package for DB Power’s 2x600MW thermal power plant at Baradarha, Chhattisgarh. The

entire plant will be commissioned within 31 months. L&T is one of the few companies to

bag consistent orders in the recent times, especially in the power space. At `1,994 –

FY2012E P/E of 28.4x and FY2012E P/BV of 4.9x on standalone basis – we believe that

most of the positives are factored in and, hence, maintain our Neutral rating on the stock.

We have used the sum-of-the-parts (SOTP) methodology to value the company to capture

all its business initiatives and investments/stakes in the different businesses and have

arrived at a Target Price of `2,024.

Result Review – 2QFY2011

HDFC Bank

HDFC Bank announced its 2QFY2011 results. The bank registered net profit growth of

32.7% yoy to `912cr, in line with our estimates of `908cr. Advances grew by a healthy

6.4% sequentially compared to marginal industry growth of ~0.6%. Deposits increased by

6.7% sequentially compared to ~1.6% industry growth. Adjusting for one-off movements

in wholesale loans, core growth in advances stood at ~32% yoy. Retail loans grew by a

healthy 30.8% yoy, constituting 51.7% of gross advances. The bank registered strong

expansion in its balance sheet, while improving the CASA ratio to 50.6% and maintaining

the NIMs at 4.2%. This is in line with our expectations that strong capital adequacy and

branch expansion will increasingly drive market share gains in credit as well as CASA for

the bank in the coming quarters. Moreover, asset quality remained stable sequentially and

was materially better than the year-ago numbers (reflected in the decline in provisions to

avg. assets from 1.1% in FY2010 to 0.7% in 2QFY2011).

During the quarter, NII increased by 29.2% yoy and 5.2% qoq to `2,526cr. Fee income

grew by a moderate 16% yoy to `857cr. The cost-to-income ratio stood at 48.2%, in line

with its eight-quarter average of 48.6%. Gross NPAs increased by 2.8% sequentially to

`1,841cr. Net NPAs stood at `409cr compared to `413cr in 1QFY2011. Gross and net

NPA ratios of the bank stood at 1.16% (1.21% in 1QFY2011) and 0.3% (0.30% in

1QFY2011), respectively, implying a healthy provision coverage ratio of 77.8%, excluding

technical write-offs. The bank’s CAR continued to be healthy at 17.0%, with tier-I at 12.7%.

At the CMP, the stock is trading at 3.8x FY2012E ABV, which is close to our target multiple

of 4.0x (benchmarked at a 30% premium to our Sensex target multiple). We maintain an

Accumulate recommendation on the stock with Target Price of `2,514.

October 20, 2010 2

3. Market Outlook | India Research

Bajaj Auto

Bajaj Auto (BAL) reported 50.4% yoy top-line growth to `4,342cr, which was above our

expectation of `4,212cr. Growth was largely aided by ~46% yoy jump in volumes. The

top-line performance was also aided by ~71% increase in other operating income at

`161cr (`94.3cr in 2QFY2010). Favourable product mix helped the company to register

~3% yoy increase in average net realisation at `41,786.

On the operating front, EBITDA margins were 66bp ahead of our estimate at 20.7%, a

jump of 69bp qoq and a fall of 138bp yoy. Raw-material cost for the quarter increased by

almost 490bp yoy, while it declined by 110bp on a qoq basis. Richer product mix along

with higher commercial vehicle volumes supported the company to report sequential

improvement at the operating front. Further, improved operating leverage helped the

company to save on staff cost and other fixed expenditure, which restricted the contraction

in EBITDA margins yoy to a certain extent. Net profit grew 69.3% yoy to `682cr (`403cr in

2QFY2010), as against our estimate of `644cr, largely aided by improved operating

performance and higher other income. Other income for the quarter increased to `83.7cr

(`21.7cr in 2QFY2010).

At current levels, the stock is trading at 19x FY2011E and 16x FY2012E earnings. We

maintain our positive outlook on the company. However, due to the recent run-up in the

stock price, we recommend a Neutral view to the stock, as we believe most of the positive

news flow is already factored in. At present, our fair value for the stock works out to be

`1,603. We would release a detailed result update post the earnings conference call with

the management.

Container Corporation

Container Corporation (Concor) reported its 2QFY2011 results, which were above our

expectations on account of better Exim performance. The company reported a 1.6% yoy

decline in total revenue to `944cr, against our estimate of `891cr. There was moderate

decline of 5.2% yoy in the company’s Exim revenue to `733cr, which came in as a positive

surprise as volumes at JNPT were impacted on account of shutdown of operations for five

days in August and prolonged monsoon. Domestic revenue grew by 13.1% yoy to `211cr,

above our expectation. We were positively surprised by higher EBIDTA margin, which came

in much above our estimate (27.0%) at 27.7%. Margins of the Exim business grew by

150bp yoy and 90bp qoq to 28.5%. However, margins of the domestic segment declined

by 290bp yoy and 360bp qoq to 9.9%. Consequently, PAT grew by 1.2% yoy to `206.7cr,

which was above our estimate (`187cr). At the CMP of `1,292, Concor is trading at 17.8x

its FY2012E EPS and 3.2x P/BV on FY2012E. We maintain our Reduce rating on the stock

with a Target Price of `1,194. We will be releasing a detailed note after the conference call

today.

Cadila Healthcare

Cadila Healthcare (Cadila) reported 2QFY2011 results, which were ahead of our

estimates. Net sales came in at `1,106cr (`913cr), up 21.2% yoy, driven by US (up 40.8%

yoy, `226cr), domestic formulation (up 19.1% yoy, `440cr), Zydus Wellness (up 23% yoy,

`80cr) and Latin America (up 27% yoy, `58cr). The company reported gross margins of

68.0% (66.9%) on the back of favourable product mix. Employee expenses increased

22.8% yoy to `137cr (`111cr). Cadila reported OPM of 21.2% (18.9%), which was higher

than our estimates of 20.5%. Financial cost went down 30.5% yoy to `16.0cr (`23cr), while

depreciation cost remained flat at `30cr. Cadila reported net profit of `171cr (`132cr), up

29.5% yoy. The stock is trading at 22.2x FY2011E and 17.2x FY2012E earnings. We

maintain our Neutral view on the stock.

October 20, 2010 3

4. Market Outlook | India Research

Alembic

Alembic reported its 2QFY2011 results, which were ahead of our estimates. Net sales

came in at strong `363cr (`282cr), up 27.8% yoy, driven by the domestic formulation

business (up 27.3%, `207cr), domestic API business (up 126.7%, `55cr) and export

formulation (up 18.8%, `55cr) business; however, the export API business declined (down

10.7%, `45cr). The company reported gross margins of 51.5% (53.9%), primarily on

account of higher proportion of low-margin domestic API business (15.1% v/s 8.5%).

Employee expenses increased 19.6% yoy to `46cr (`39cr). Alembic reported OPM of

11.9% (11.9%), which was marginally lower than our estimates. Financial cost went down

26.3% yoy to `7cr (`9cr). Depreciation cost remained flat at `12cr. Alembic reported net

profit of `22cr (`13cr), up 64.3% yoy, driven by top-line growth and lower financial cost.

We recommend Accumulate on the stock with a Target Price of `74.

Result Previews – 2QFY2011

Hindustan Zinc

Hindustan Zinc is expected to announce its results. We expect the company’s top line to

grow by 14.5% to `2,049cr on account of higher zinc volumes. EBITDA margins are

expected to contract by 525bp to 53.2%. Consequently, net income is expected to increase

marginally by 3.3% to `966cr. We recommend a Neutral rating on the stock.

Yes Bank

Yes Bank is scheduled to announce its 2QFY2011 results. We expect the bank to report

robust NII growth of 75.9% yoy, driven by strong growth in advances, while the non-

interest income is expected to decline by 9.3% yoy. The cost-to-income ratio is expected to

deteriorate to 39.5% compared to 38.7% in 1QFY2011 and 36.9% in 2QFY2010 on

account of higher employee additions in 1QFY2011. The pre-provision profit of the bank

is expected to register healthy growth of 32.1% yoy. Net profit is expected to increase by

23.5% on a yoy basis to `138cr. At the CMP, the stock is trading at valuations of 2.8x

FY2012E ABV. We maintain our Neutral rating on the stock.

Ashok Leyland

Ashok Leyland is slated to announce its 2QFY2011 results. We expect the company’s top

line to grow by a substantial 62.2% yoy to `2,559cr on account of 72% yoy growth in

volumes and marginal increase in realisation. On the operating front, EBITDA margin is

expected to decline by 53bp yoy to 10% on account of increased raw-material cost.

However, the bottom line is expected to surge by 51.7% yoy to `134.4cr. The stock rating

is under review.

Indoco Remedies

Indoco Remedies is expected to report top-line growth of 17.9% to `113cr, driven by the

domestic and export segments. The domestic formulation segment is expected to grow by

17.5% to `78cr. The company's OPM is expected to expand by 260bp to 15.6%, driven by

top-line growth. As a result, net profit is expected to increase by 55.6% to `14.3cr. We

maintain Buy on the stock with a Target Price of `541.

October 20, 2010 4

5. Market Outlook | India Research

Economic and Political News

Domestic air passenger numbers drop 11.08%

TRAI regulation on unsolicited calls by October-end

India to step up asset sales in next six months as investor appetite grows

Corporate News

SBI grants highest ever loan of `300cr for dairy firms in Punjab

Videocon discovers Gas in another well in Mozambique

KAL Airways buys further 2.28% stake in SpiceJet

Havells enters new generation Electric Water Heaters business

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Agro Tech Foods Results

Ashok Leyland Results

BASF India Results

Bombay Dyeing Results

Canara Bank Results

Ceat Results

Gujarat State Fertilizers Results

HCL Tech Results

Hindustan Zinc Results

Indiabulls Power Results

Indiabulls Real Estate Results

Indoco Remedies Results

Jubilant Organosys Results

Kotak Mahindra Bank Results

Lanco Industries Results

Mahindra Lifespace Developers Results

Pidilite Industries Results

Power Grid Corporation Results

VIP Industries Results

Yes Bank Results

October 20, 2010 5

6. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

October 20, 2010 6