1. Market Outlook

India Research

July 5, 2010

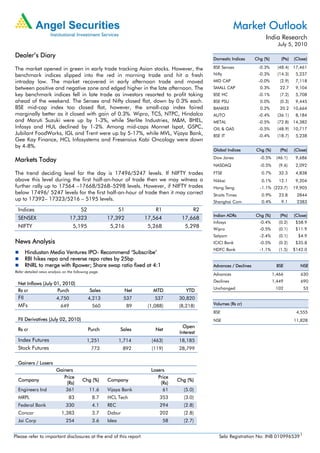

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The market opened in green in early trade tracking Asian stocks. However, the BSE Sensex -0.3% (48.4) 17,461

benchmark indices slipped into the red in morning trade and hit a fresh Nifty -0.3% (14.3) 5,237

intraday low. The market recovered in early afternoon trade and moved MID CAP -0.0% (2.9) 7,118

between positive and negative zone and edged higher in the late afternoon. The SMALL CAP 0.3% 22.7 9,104

key benchmark indices fell in late trade as investors resorted to profit taking BSE HC -0.1% (7.2) 5,708

ahead of the weekend. The Sensex and Nifty closed flat, down by 0.3% each. BSE PSU 0.0% (0.3) 9,445

BSE mid-cap index too closed flat, however, the small-cap index faired BANKEX 0.2% 20.2 10,664

marginally better as it closed with gain of 0.3%. Wipro, TCS, NTPC, Hindalco AUTO -0.4% (36.1) 8,184

and Maruti Suzuki were up by 1-3%, while Sterlite Industries, M&M, BHEL, METAL -0.5% (72.8) 14,382

Infosys and HUL declined by 1-2%. Among mid-caps Monnet Ispat, GSPC, OIL & GAS -0.5% (48.9) 10,717

Jubilant FoodWorks, IGL and Trent were up by 5-17%, while MVL, Vijaya Bank, BSE IT -0.4% (18.7) 5,238

Gee Kay Finance, HCL Infosystems and Fresensius Kabi Oncology were down

by 4-8%.

Global Indices Chg (%) (Pts) (Close)

Dow Jones -0.5% (46.1) 9,686

Markets Today

NASDAQ -0.5% (9.6) 2,092

The trend deciding level for the day is 17496/5247 levels. If NIFTY trades FTSE 0.7% 32.3 4,838

above this level during the first half-an-hour of trade then we may witness a Nikkei 0.1% 12.1 9,204

further rally up to 17564 –17668/5268–5298 levels. However, if NIFTY trades Hang Seng -1.1% (223.7) 19,905

below 17496/ 5247 levels for the first half-an-hour of trade then it may correct Straits Times 0.9% 23.8 2844

up to 17392– 17323/5216 – 5195 levels. Shanghai Com 0.4% 9.1 2383

Indices S2 S1 R1 R2

Indian ADRs Chg (%) (Pts) (Close)

SENSEX 17,323 17,392 17,564 17,668

Infosys -0.4% (0.2) $58.9

NIFTY 5,195 5,216 5,268 5,298 Wipro -0.5% (0.1) $11.9

Satyam -2.4% (0.1) $4.9

News Analysis ICICI Bank -0.5% (0.2) $35.8

HDFC Bank -1.1% (1.5) $142.0

Hindustan Media Ventures IPO- Recommend ‘Subscribe’

RBI hikes repo and reverse repo rates by 25bp

RNRL to merge with Rpower; Share swap ratio fixed at 4:1 Advances / Declines BSE NSE

Refer detailed news analysis on the following page.

Advances 1,466 630

Declines 1,449 690

Net Inflows (July 01, 2010)

Unchanged 102 53

Rs cr Purch Sales Net MTD YTD

FII 4,750 4,213 537 537 30,820

MFs 649 560 89 (1,088) (8,218) Volumes (Rs cr)

BSE 4,555

FII Derivatives (July 02, 2010) NSE 11,828

Open

Rs cr Purch Sales Net

Interest

Index Futures 1,251 1,714 (463) 18,185

Stock Futures 773 892 (119) 28,799

Gainers / Losers

Gainers Losers

Price Price

Company Chg (%) Company Chg (%)

(Rs) (Rs)

Engineers Ind 361 11.6 Vijaya Bank 61 (5.0)

MRPL 83 8.7 HCL Tech 353 (3.0)

Federal Bank 330 4.1 REC 294 (2.8)

Concor 1,383 3.7 Dabur 202 (2.8)

Jai Corp 254 3.6 Idea 58 (2.7)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 0109965391

2. Market Outlook | India Research

Hindustan Media Ventures IPO- Recommend ‘Subscribe’

Hindustan Media Ventures (HMVL) is tapping the IPO market with an issue size of Rs270cr

and a price band of Rs162-175 per equity share, thus resulting in a public issue of 1.67cr

and 1.54cr equity shares of face value Rs10, resulting in a promoter shareholding dilution

of 23% and 21% at the lower and the upper price band, respectively. The company plans

to use the IPO proceeds for expanding its presence in new markets and for the repayment

of debt. HMVL plans to set up eight new publishing units for printing and publishing new

editions of Hindustan and expects the same to be fully operational by end of fiscal 2012.

We recommend our Subscribe view on the issue based on Hindustan’s third largest

cumulative readership base (9.9mn), dominant position in the Hindi speaking states of

Bihar/Jharkhand (readership of 4.5mn and 1.4mn, respectively) and strong infrastructure

and synergies with promoter HT Media. Our Subscribe view on the issue is based on 18x

FY2012E EPS (~10% discount to our target multiple of 20x for Jagran and DB Corp);

hence, we arrive at a fair value of Rs195, indicating an ~11% upside to the upper price

band.

RBI hikes repo and reverse repo rates by 25bp

The Reserve Bank of India (RBI) has raised the repo and reverse repo rates by 25bp each

to 5.5% and 4.0%, respectively. Up to February 2010, food and textiles were contributing

as much as 70% of the overall 9.9% WPI inflation on account of the drought-driven

increase in prices of food grains, sugar, and cotton, among others. By May 2010, their

contribution to the 10.2% WPI inflation, though on a downward trend, was still high at

57%. Oil continued to contribute 12% to overall inflation, though this is likely to increase in

the coming weeks due to the increase in petrol and diesel prices. Contribution of other

items (having 50% weightage in the WPI index) had increased to 31% in May 2010 due to

the increase in the prices of coal, metals, electricity and wood products, among others,

indicating that inflation is becoming more broad-based. Therefore, monetary tightening to

anchor inflation expectations is appropriate at this juncture. Going forward, as credit

demand is expected to sustain at least above the 19% level, banks are expected to raise

their lending and deposit rates. The expected increase in interest rates will not affect the

sector negatively, as it will be outweighed by acceleration in core earnings growth on the

back of improvement in credit growth and fee income coupled with a sharp reduction in

NPA losses. However, on a relative basis, we continue to prefer banks with a high CASA

ratio and lower-duration investment book, given the rising interest rate scenario.

July 5, 2010 2

3. Market Outlook | India Research

RNRL to merge with Rpower; Share swap ratio fixed at 4:1

The boards of Reliance Power (Rpower) and Reliance Natural Resources (RNRL) have

decided to merge RNRL with Rpower. The merger will be done on a share swap basis and

the ratio will be 4:1, which implies RNRL shareholders will get one share of Rpower for

every four shares of RNRL held by them. The share swap ratio has been fixed on an

independent valuation by KPMG, wherein RNRL has been valued at Rs7,157cr at a 31%

discount to its total market capitalization based on the closing price of its share on July 2nd

2010. This deal would result in a fresh issue of 41cr shares by Rpower as the total number

of shares outstanding of RNRL stands currently at 163cr. The total outstanding shares of of

RPower post merger would stand at 280cr.

Post the Supreme Court verdict in RIL-RNRL case, RNRL was reduced to a shell company as

it was declared that the government has the sole rights in the allocation of gas and fixing

the price for the same. Thus going ahead the company would not earn any marketing

margin which works to around Rs156cr per annum (at 0.14$/mmbtu transferred) on

28mmscmd of gas as per our estimates, which it would have earned post the

commencement of Rpower’s gas based plants. Meanwhile, as per the court orders RIL and

RNRL signed a revised gas supply master agreement on June 25, which will be at the price

determined by the government. Though, the deal is negative for RNRL shareholders in the

short term due to the unfavourable swap ratio, on a long-term basis, this deal would

compensate the RNRL shareholders by providing direct exposure to Rpower’s utility

business.

As for Rpower, RNRL will bring in prospects for gas from Coal Bed Methane (CBM) blocks,

with estimated resources of about 193 billion cubic metres. RNRL also has 10% share in an

oil and gas block in Mizoram, with an acreage of 3,619sqkm and reserve potential of up

to 28 billion cubic metre. RNRL will also bring in expertise in coal supply logistics and

shipping businesses. Despite this, we feel the the move is a negative for Rpower

shareholders, considering the 14.6% equity dilution as the merger is not expected to yield

much of synergy benefits for Rpower.

Economic and Political News

Govt. may review PSY bank’s freedom to choose auditors

FIIs invest US $2.3bn in first quarter: SEBI

Tea exports up 19% in Jan-May period

Corporate News

Shopper’s stop eyes ~Rs1,000cr revenue from Hypercity

SREI infra to raise Rs4,600cr PE fund

M&M, Adani in race to buy DLF’s stake in insurance firm

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Zee News Dividend,Results

July 5, 2010 3

4. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in

this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem

necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and

risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that

are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the

company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be

true, and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document.

Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

document. While Angel Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed

on, directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory

services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with

the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

July 5, 2010 4