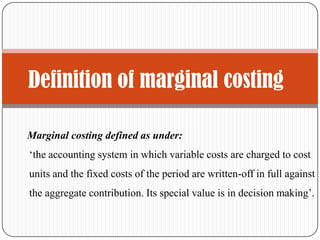

This document provides an introduction to marginal costing. It defines marginal costing as an accounting system where only variable costs are charged to cost units and fixed costs are written off for the period. Marginal costing is useful for management decision making. It presents costs in a way that helps management make important decisions. Inventory is valued based on marginal costs. A marginal profit and loss statement is prepared to determine profit. Selling prices are based on marginal cost plus contribution. Contribution is sales price minus variable cost. Break-even analysis is part of the marginal costing system. Contribution from sales is compared to determine profitability of departments or products.