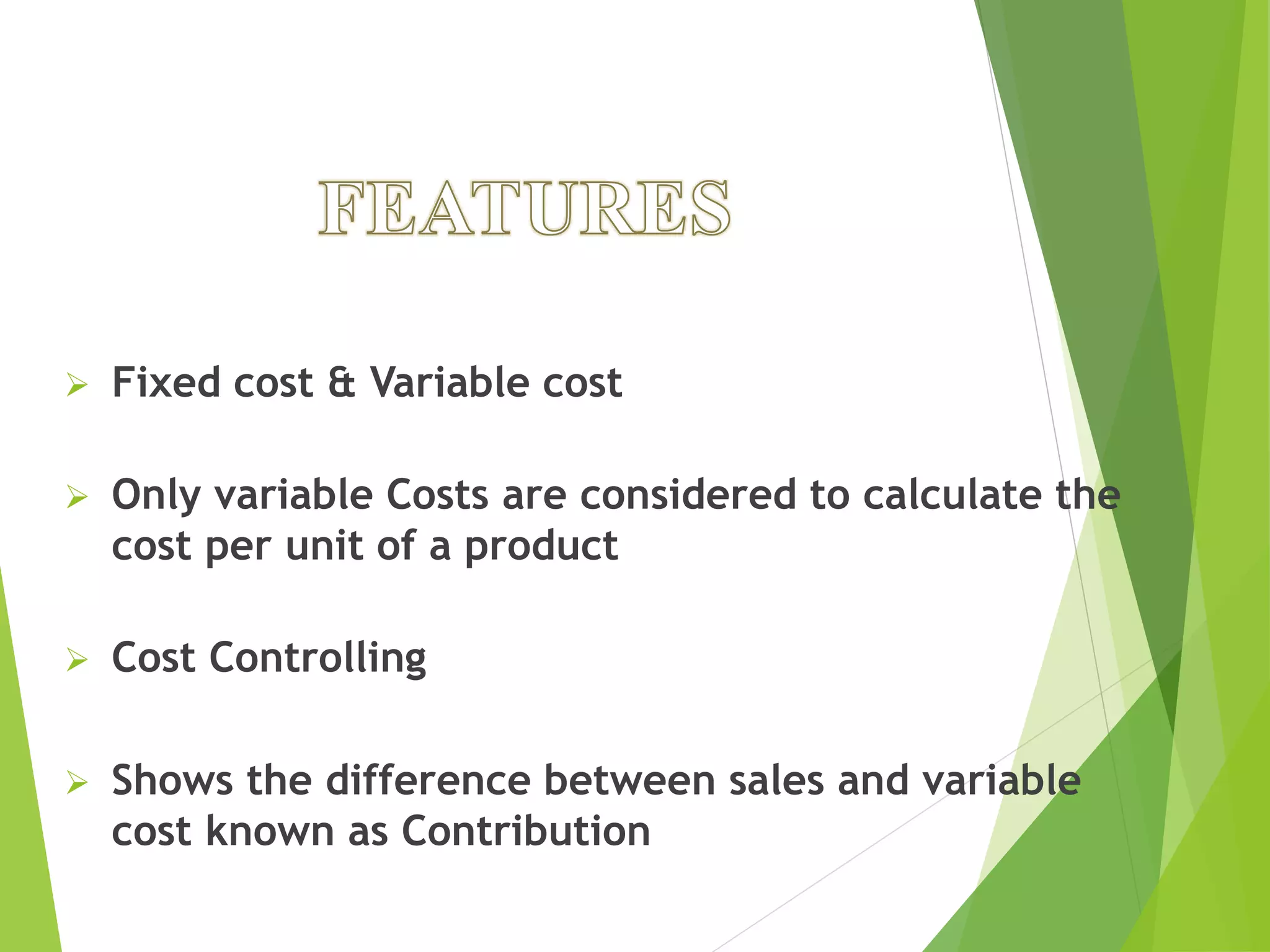

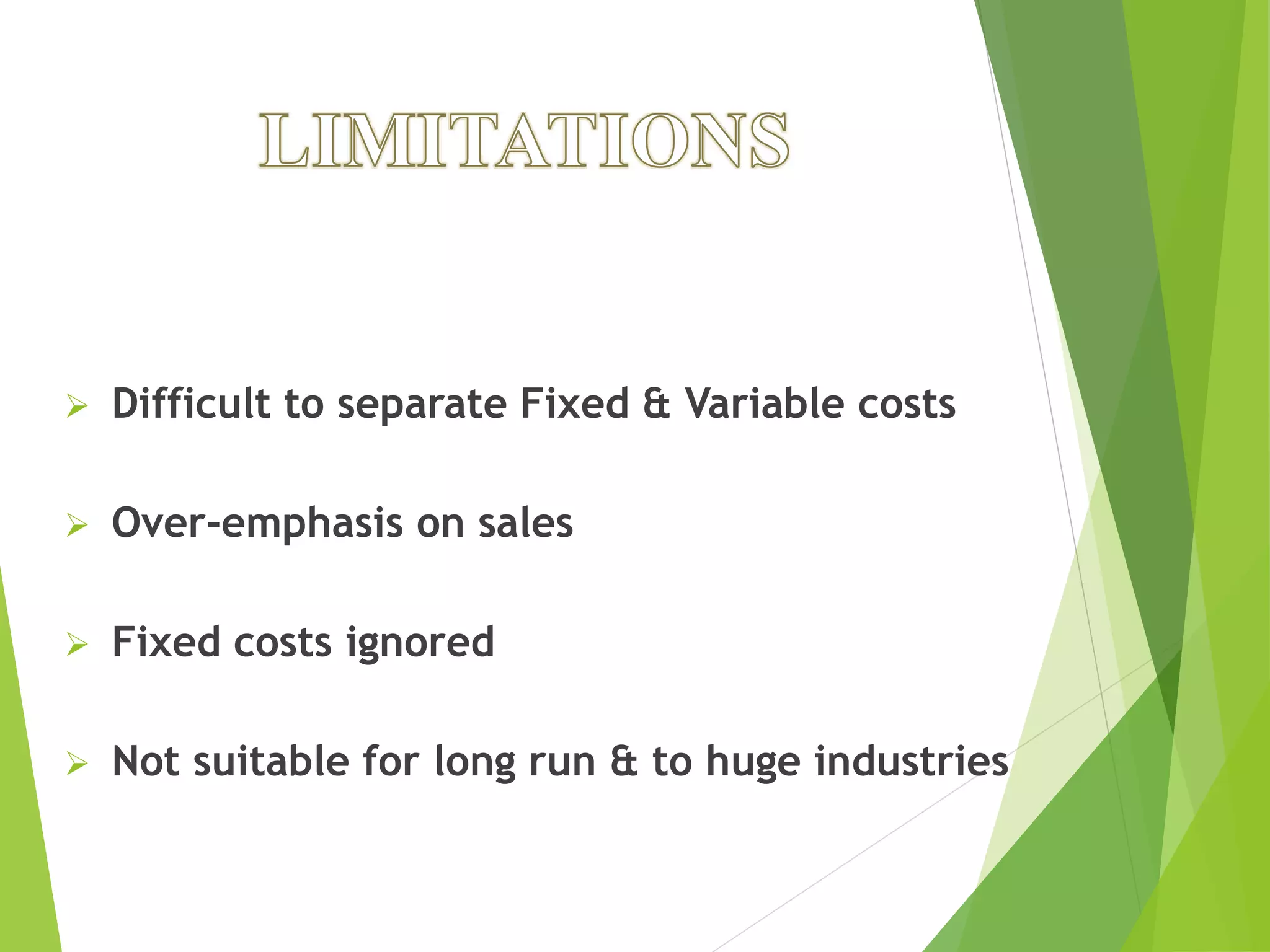

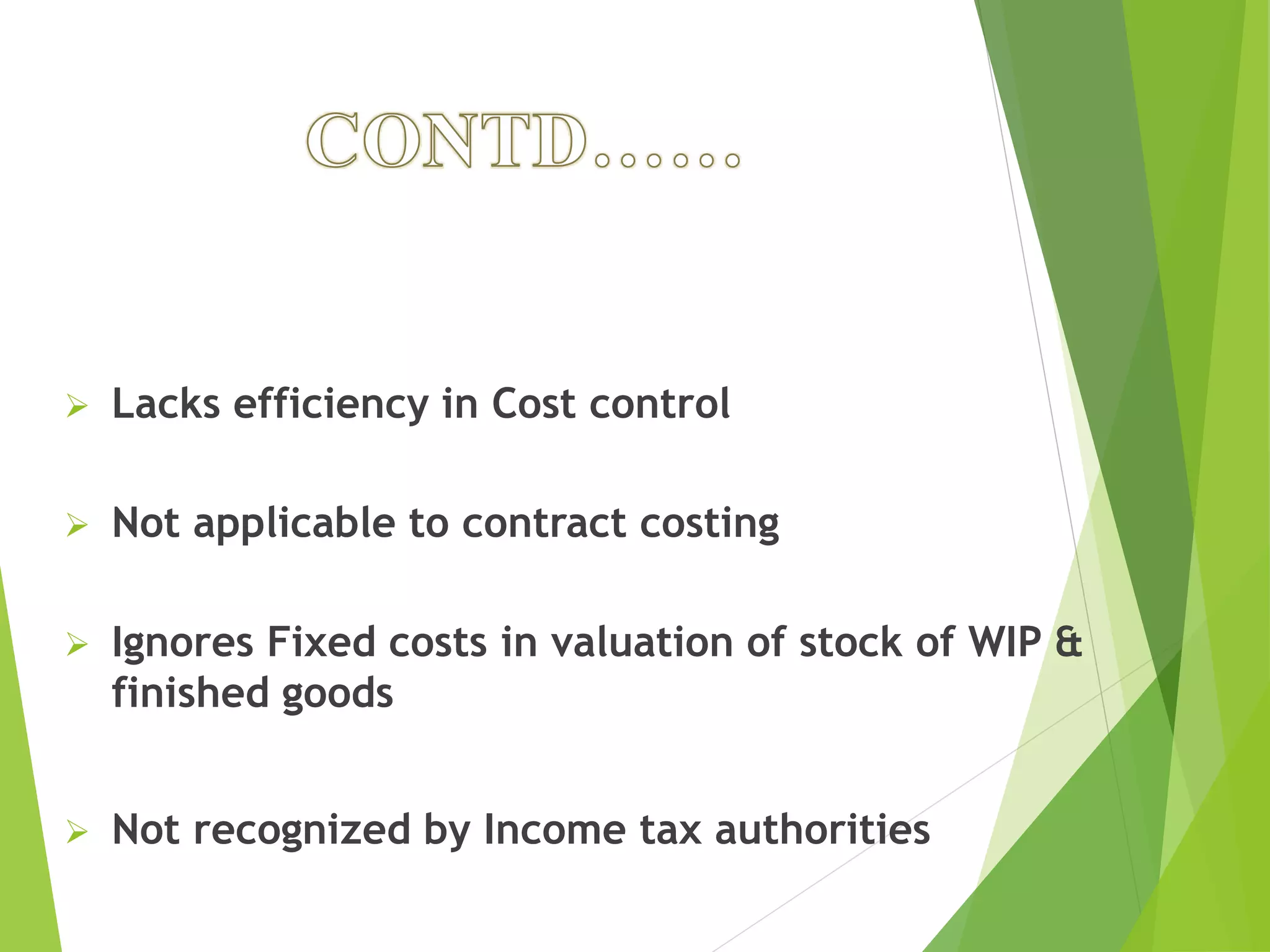

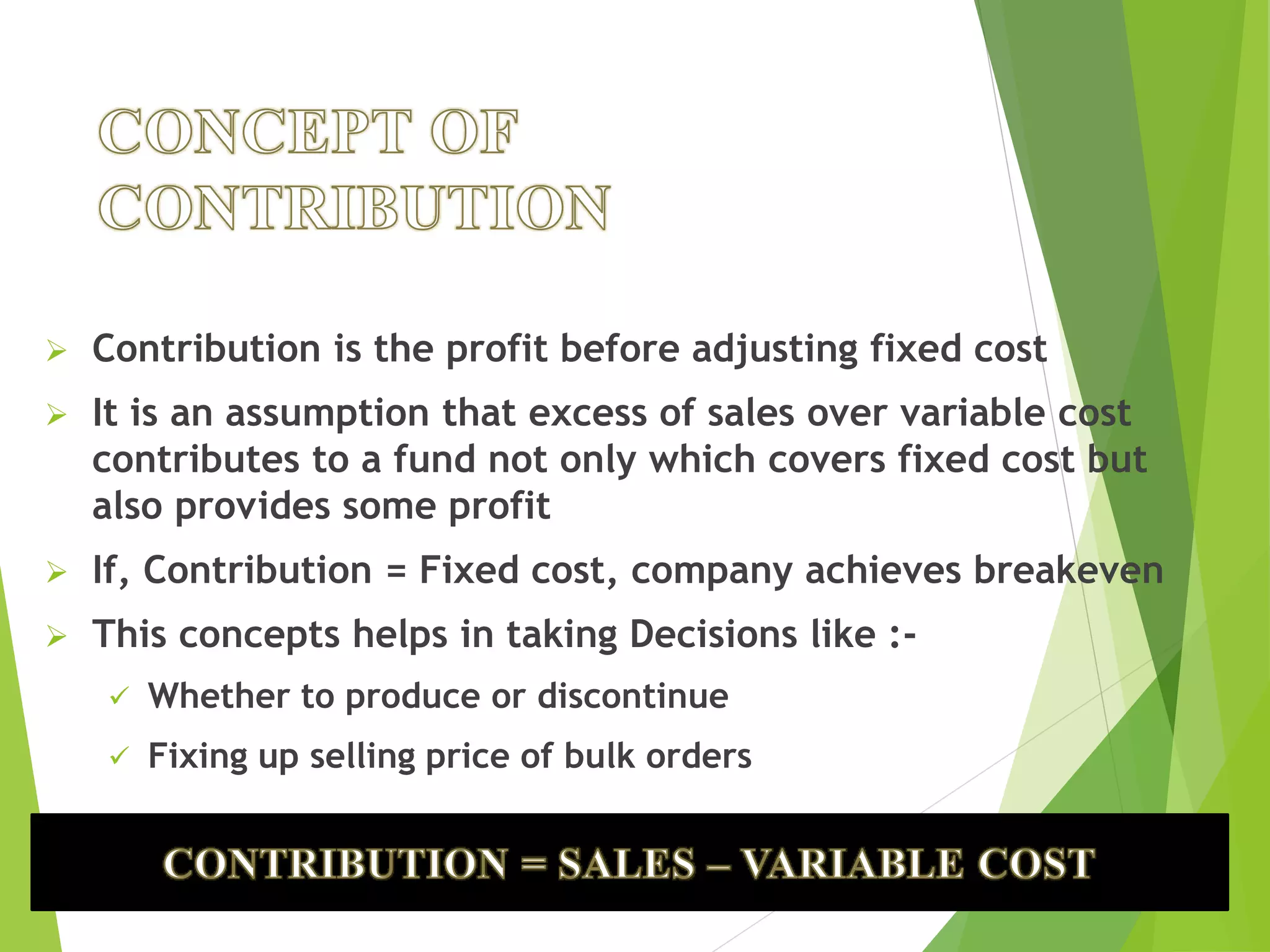

Marginal costing is a technique that classifies costs as either fixed or variable. Fixed costs remain the same regardless of production volume, while variable costs change directly with output. Under marginal costing, only variable costs are considered when calculating the unit cost of a product. The difference between sales revenue and variable costs is known as the contribution, which is useful for decision making like determining the breakeven point where total contribution covers total fixed costs. Marginal costing focuses on maximizing contribution by controlling variable costs and increasing sales volume.