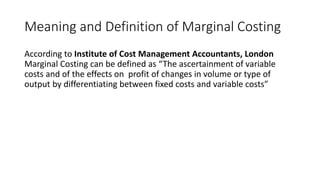

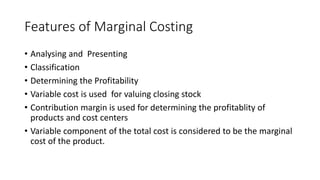

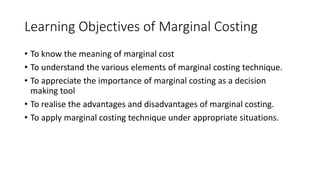

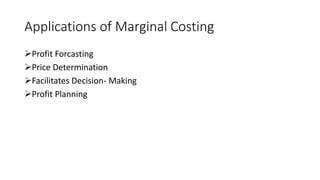

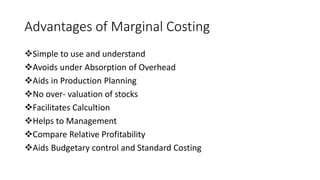

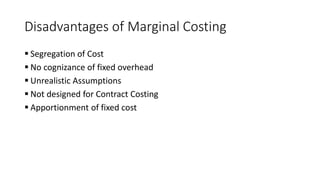

Marginal costing is a technique that differentiates between fixed and variable costs to determine the effect of changes in output on profits. It classifies costs as fixed or variable, uses variable costs to value inventory, and contribution margin to determine profitability of products and cost centers. Marginal costing can be used for profit forecasting, price determination, decision-making, and profit planning. Its advantages include being simple to use, avoiding overhead absorption issues, and aiding production planning. However, its disadvantages include the segregation of costs and not considering fixed overhead.

![08-Insight 2016 Prelims Test Series[shashidthakur23.wordpress.com].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/08-insight2016prelimstestseriesshashidthakur23-230323105248-6782aa3f-thumbnail.jpg?width=640&height=640&fit=bounds)