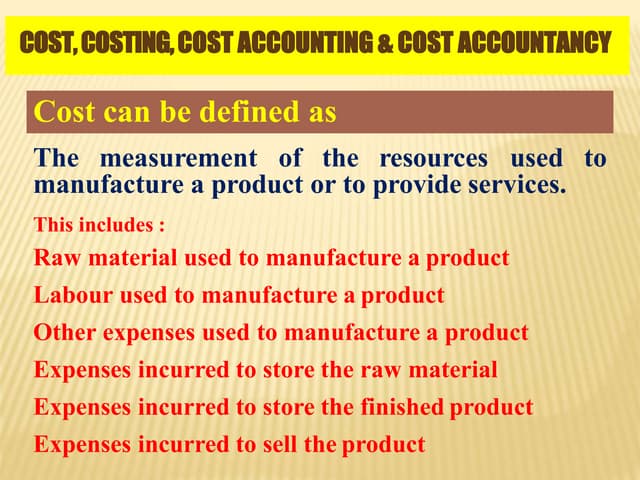

Downloaded 163 times

![13

MarginalCost

In economics and finance, marginal cost is the change in total cost that arises when the

quantity produced changes by one unit. It is the cost of producing one more unit of a good.

[1] Mathematically, the marginal cost (MC) function is expressed as the first derivative of

the total cost (TC) function with respect to quantity (Q). Note that the marginal cost may

change with volume, and so at each level of production, the marginal cost is the cost of the

next unit produced.

RelationbetweenMarginalCostand Economies ofScale

Production may be subject to economies of scale (or diseconomies of scale).

Increasing returns to scale are said to exist if additional units can be produced for

less than the previous unit, that is, average cost is falling.

This can only occur if average cost at any given level of production is higher than

the marginal cost.

Conversely, there may be levels of production where marginal cost is higher than

average cost, and average cost will rise for each unit of production after that point.

This type of production function is generally known as diminishing marginal

productivity: at low levels of production, productivity gains are easy and marginal

costs falling, but productivity gains become smaller as production increases;

eventually, marginal costs rise because increasing output (with existing capital,

labour or organization) becomes more expensive. For this generic case, minimum

average cost occurs at the point where average cost and marginal cost are equal

(when plotted, the two curves intersect); this point will not be at the minimum for

marginal cost if fixed costs are greater than zero.](https://image.slidesharecdn.com/applicationofmarginalcostingtechniqueitslimitations-151108065514-lva1-app6891/75/Application-of-marginal-costing-technique-amp-its-limitations-13-2048.jpg)

This document is a project report submitted by a student named Vivek Shriram Mahajan to the University of Mumbai in partial fulfillment of an M.Com degree in Accountancy. The report discusses the application of marginal costing technique and its limitations. It includes an introduction, objectives and importance of cost accounting, an introduction to marginal costing explaining key concepts, applications of marginal costing in managerial decisions, advantages and disadvantages, and limitations of the marginal costing technique.