- Marginal costing is a technique that differentiates between fixed and variable costs to help with managerial decision making. It involves calculating marginal costs and the effect on profit from changes in output volume or product mix.

- The key aspects of marginal costing are classifying total costs into fixed and variable components, using marginal costs and contribution margins to evaluate decisions, and treating fixed costs as period costs rather than product costs.

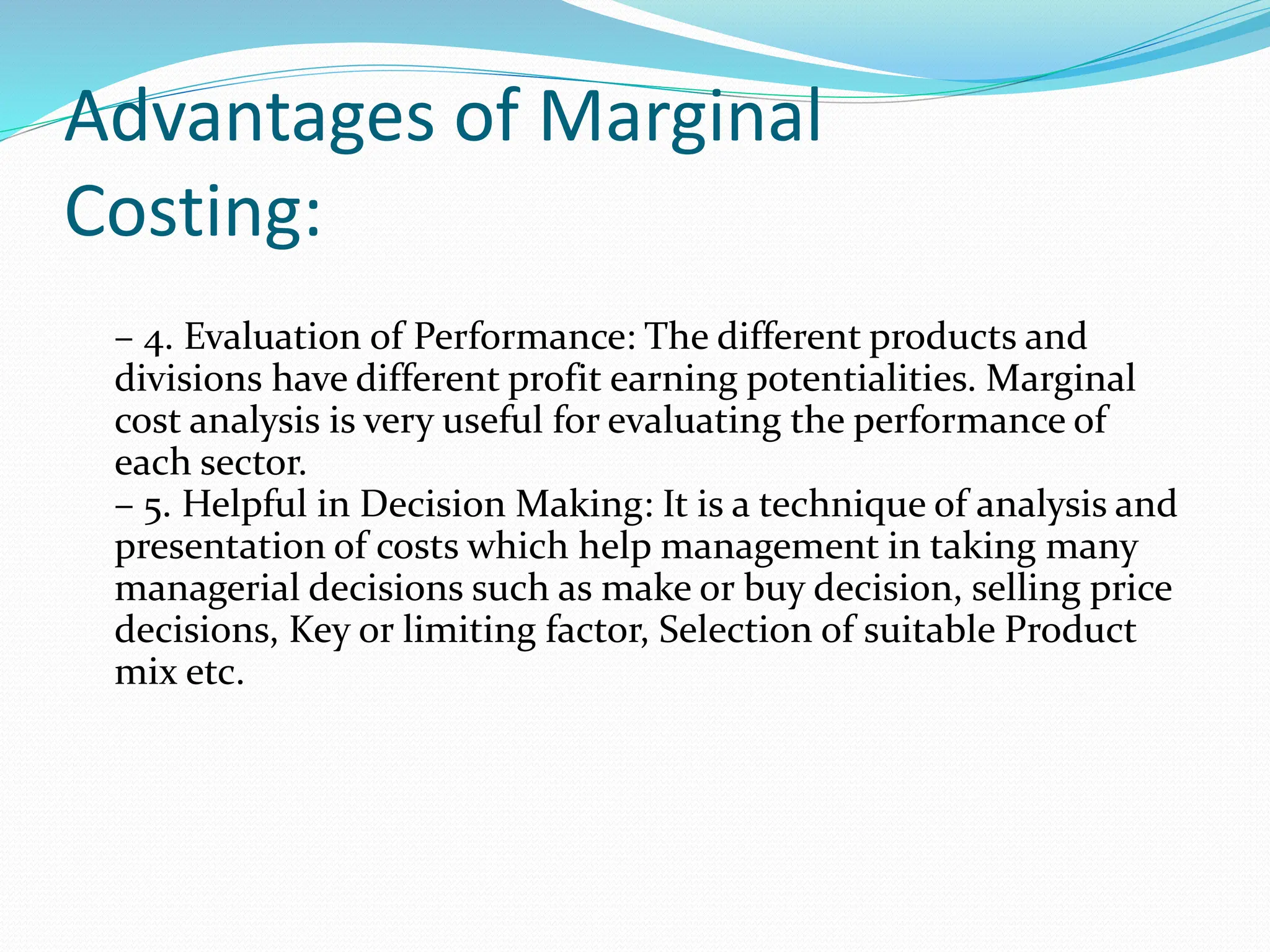

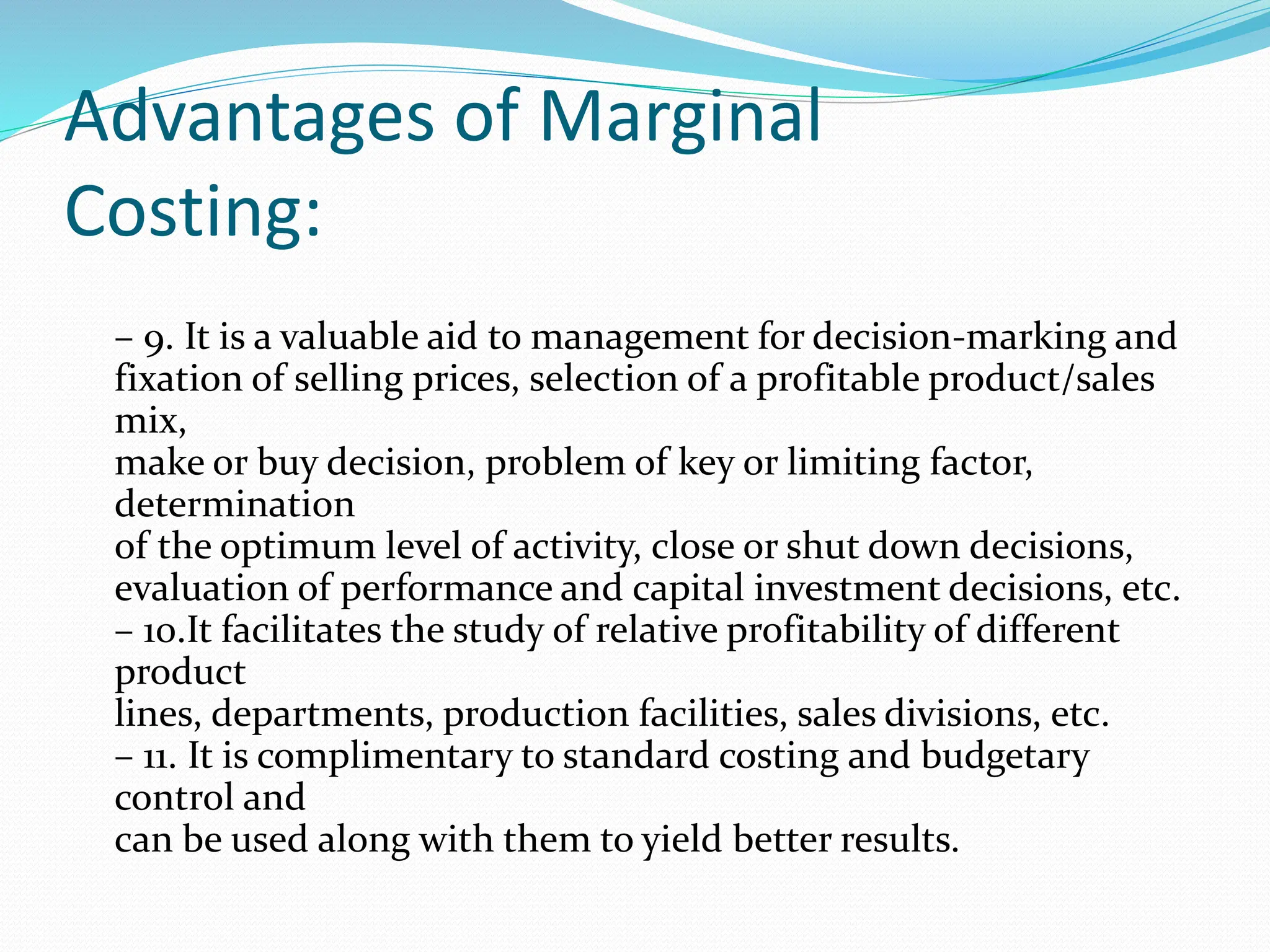

- Marginal costing provides several advantages like simplifying cost analysis, aiding cost control, profit planning, performance evaluation, and decision making around pricing, production, and product mix. It helps management evaluate alternatives and maximize returns.