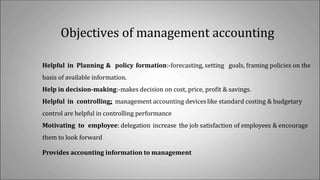

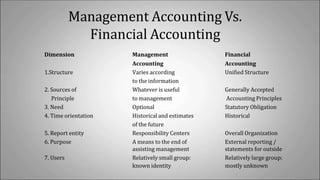

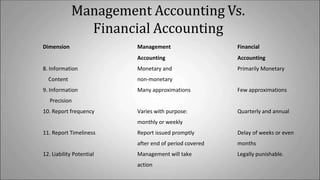

Cost and management accounting involves three parts: financial accounting, cost accounting, and management accounting. Financial accounting records and reports on financial transactions and statements. Cost accounting records and measures cost information for decision making and performance evaluation. Management accounting provides accounting data to management for planning, decision making, control, and motivation of employees. It has a different structure, principles, users, and timeliness than financial accounting.