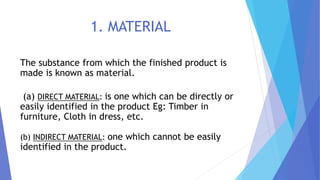

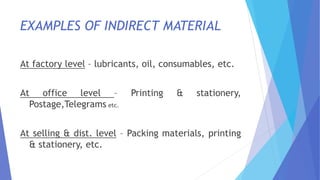

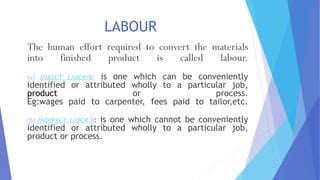

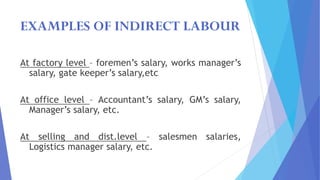

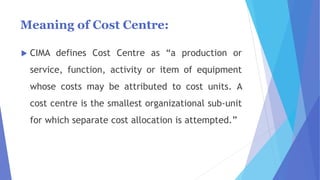

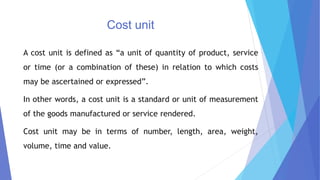

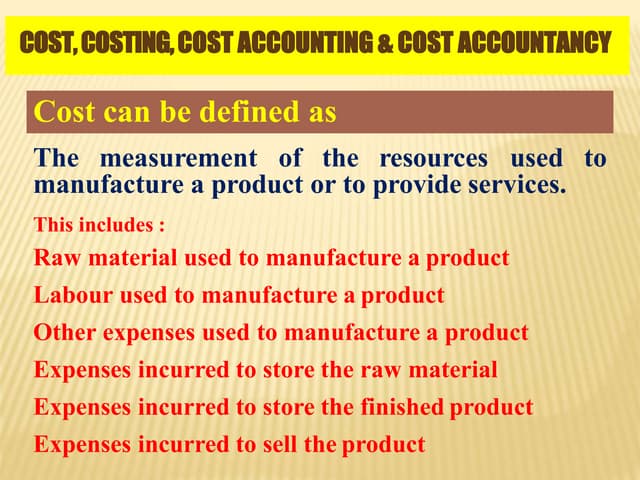

This document provides an introduction to cost accounting. It defines cost as the expenditure incurred to produce a good or service. Cost accounting is the process of tracking and measuring financial and non-financial inputs and outputs of processes to determine the cost of products, services, activities or equipment. The objectives of cost accounting include determining costs, setting prices, increasing efficiency, controlling costs, and aiding managerial decision making. Costs are classified by nature as materials, labor or expenses, and by behavior as fixed or variable. Cost centers and cost units are also introduced as organizational sub-units and units of measurement used in cost accounting.