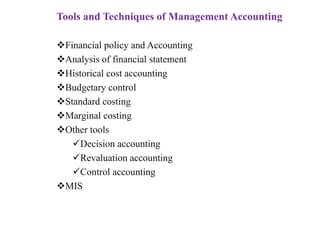

Management accounting involves collecting and analyzing both financial and non-financial information to help managers plan strategies, set goals, and make decisions. It differs from financial accounting in that it is for internal use by management rather than external reporting. Some key tools of management accounting include budgeting, cost accounting, financial analysis, and decision making techniques. The information provided by management accounting aims to increase efficiency, support effective planning and control, and maximize profitability for the organization.