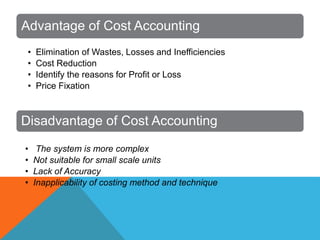

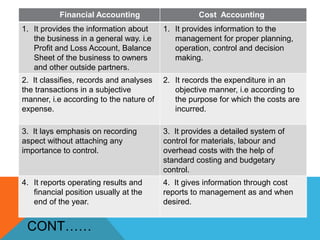

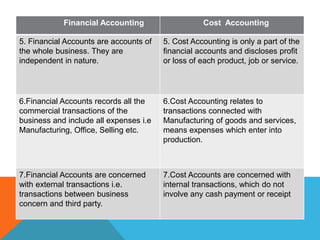

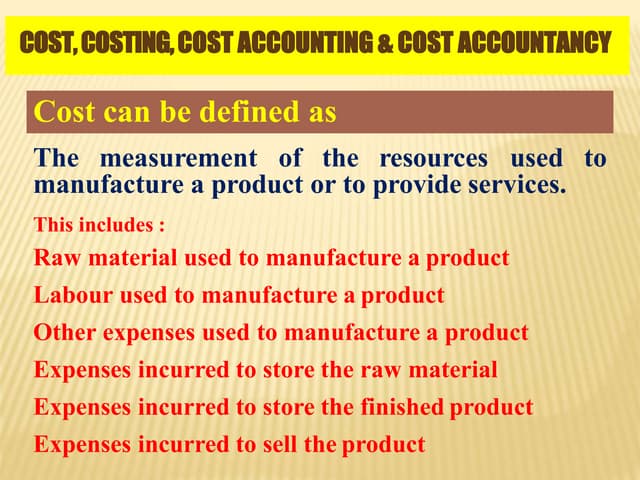

Cost accounting involves the classification, recording, and analysis of costs to determine product or service costs and support managerial decision-making. It serves various objectives such as cost ascertainment, efficiency control, and valuation of inventory, while distinguishing between direct and indirect costs, fixed and variable costs, and different functions. The advantages include waste elimination and cost reduction, whereas disadvantages encompass complexity and potential inaccuracies in cost methodology.