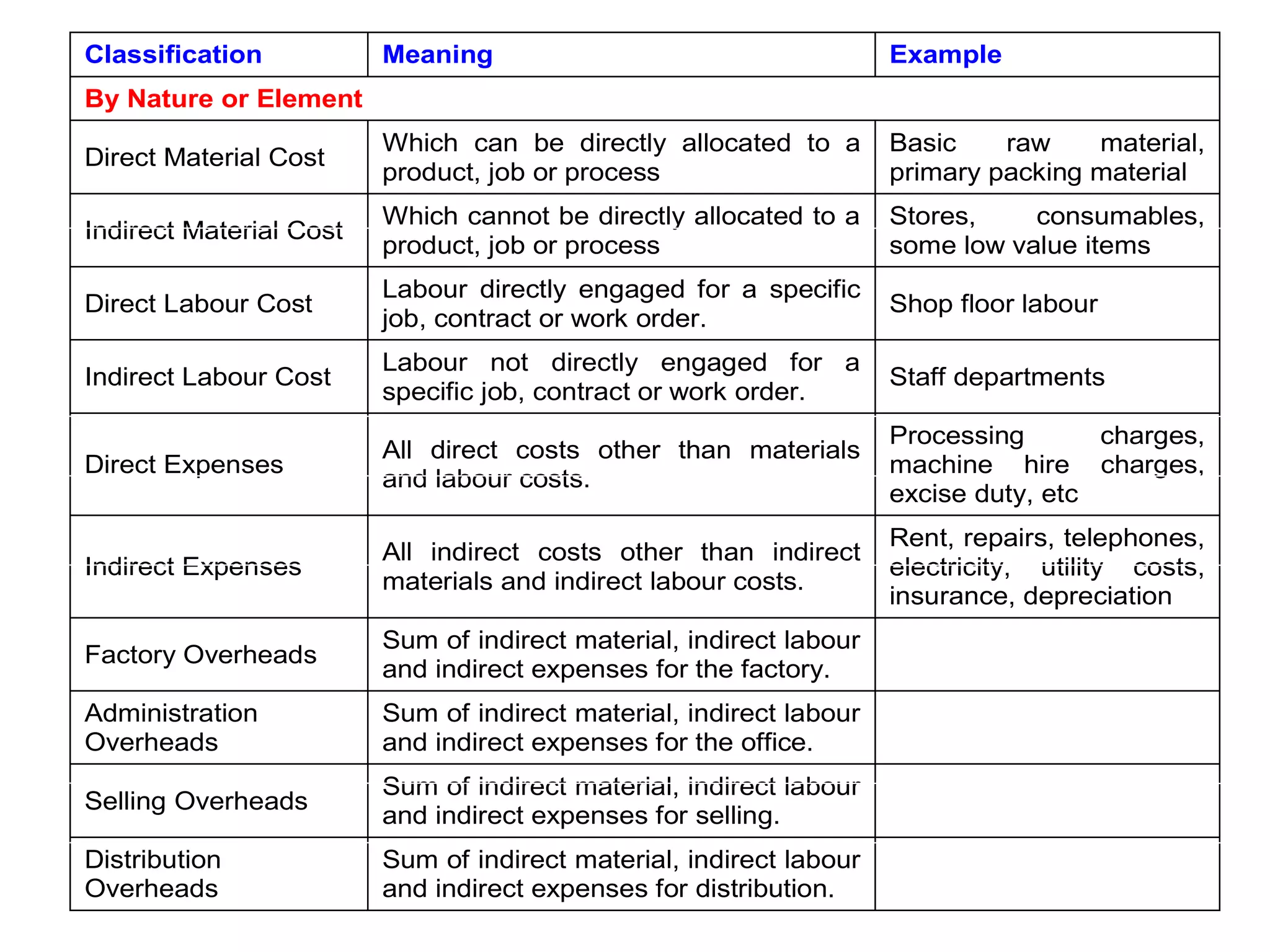

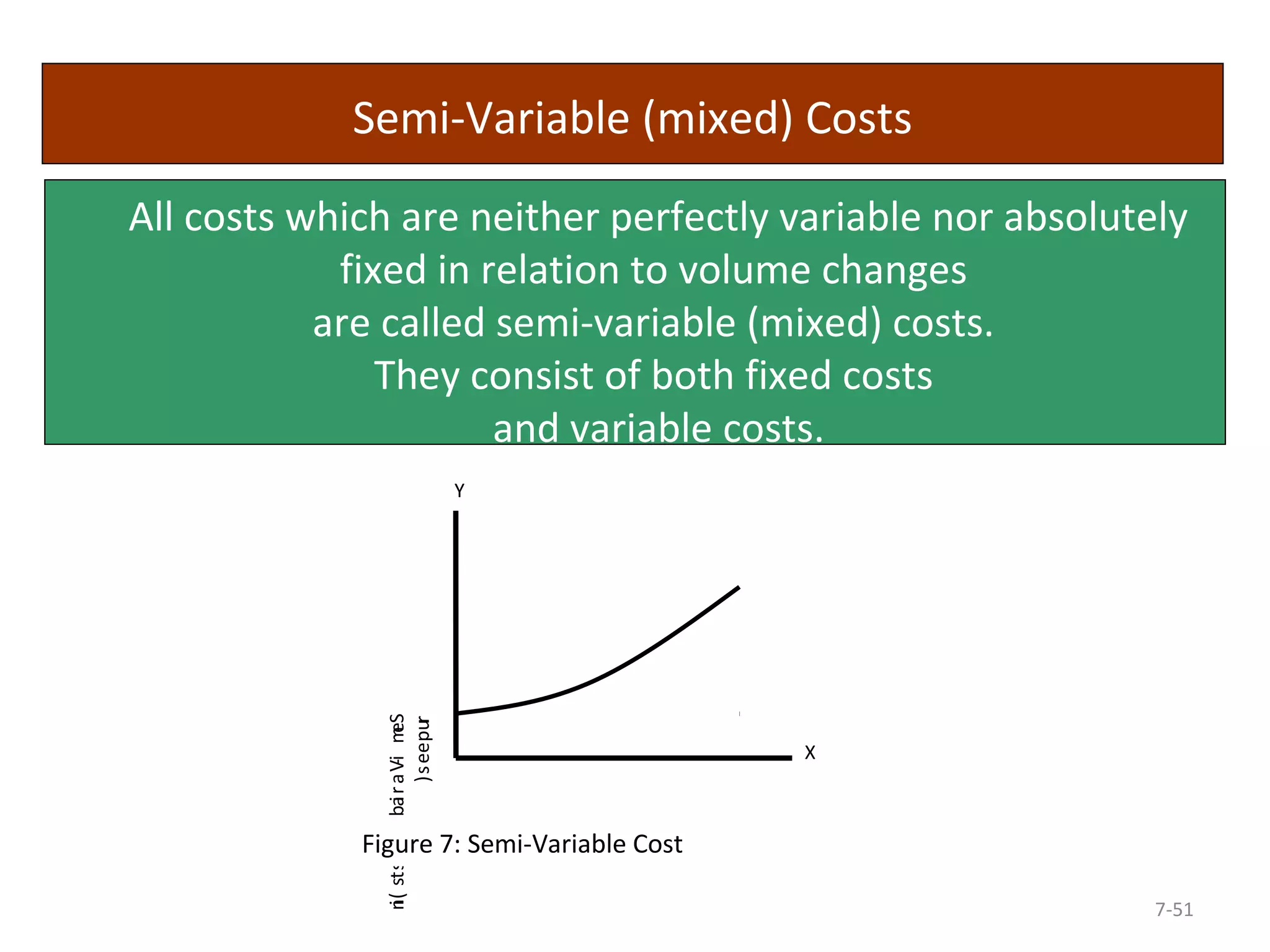

Downloaded 1,483 times

![Example 1: Absorbed, Underabsorbed and Overabsorbed Costs

Suppose that fixed costs are Rs 30,000 and the normal production is

15,000 units. The standard fixed overhead rate (SFOR) of recovery is

Rs 2 per unit (Rs 30,000 ÷ 15,000 units). In other words, every unit of

production absorbs Rs 2 of fixed costs.

If the company produces 10,000 units, the total absorbed costs will be Rs

20,000 (10,000 units × Rs 2, SFOR). Obviously, Rs 10,000 constitutes

unabsorbed costs (Rs 30,000, actual cost – Rs 20,000, absorbed costs).

In contrast, overabsorbed costs represent the positive difference of fixed

costs charged to production and actual fixed costs. Such a situation will

arise if actual production is more than the normal production.

In the above example, if the company produces 16,250 units, the costs

charged to production will be Rs 32,500 (16,250 units × Rs 2, SFOR). The

overabsorbed cost will be Rs 2,500 [Rs 30,000, actual fixed costs (AFC) –

Rs 32,500 charged to production]. Figure 1 portrays these relationships.

7-44](https://image.slidesharecdn.com/costmanagementaccounting-141102023755-conversion-gate02/75/Cost-management-accounting-44-2048.jpg)

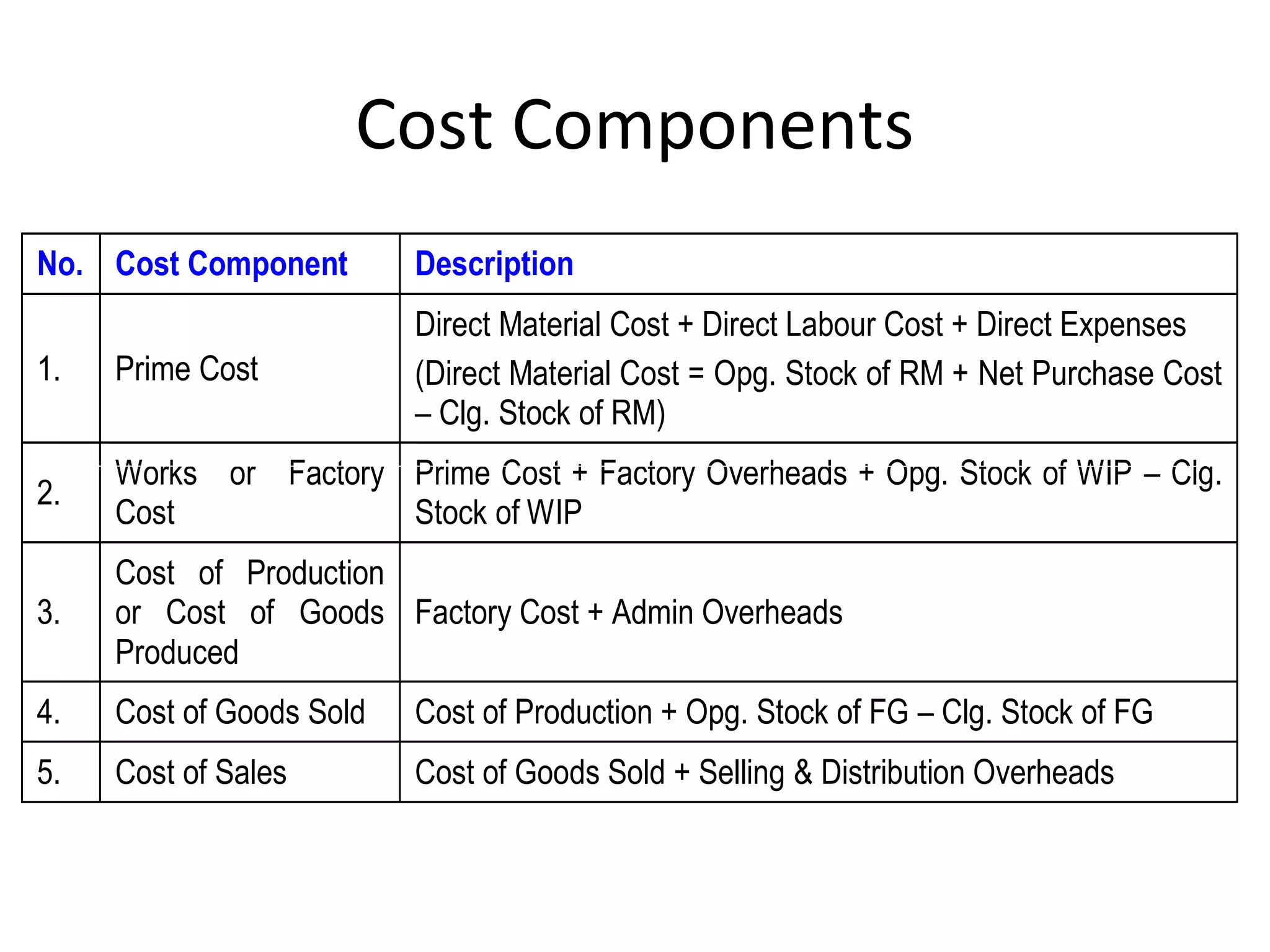

![7-45

Absorbed costs = Units produced × SFOR

Unabsorbed costs = [AFC – (Units produced × SFOR)]

Overabsorbed costs = [Units produced × SFOR) – AFC]

)seepur ni( sdaehr ev O dexi F

Over-absorption

Under-absorption

Volume of Activity (in Units)

Y

X

Figure 1: Absorbed and Unabsorbed Costs

FC Line

Full absorption

32,500

30,000

1,5000

10,000 1,5000 1,5000](https://image.slidesharecdn.com/costmanagementaccounting-141102023755-conversion-gate02/75/Cost-management-accounting-45-2048.jpg)

This document provides an introduction to cost and management accounting. It discusses key concepts such as cost accounting, management accounting, costing, and the differences between financial accounting and management accounting. The objectives of cost accounting are to ascertain costs, control costs, aid decision-making, determine selling prices, and more. Management accounting builds on cost and financial accounting data to provide information for planning, control, and decision-making. It focuses on the internal needs of management rather than external reporting.