Download as PDF, PPTX

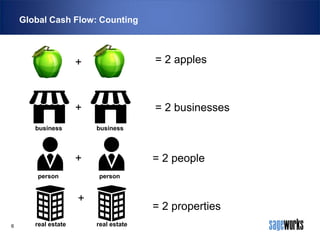

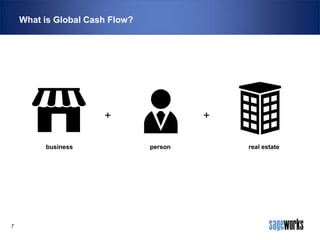

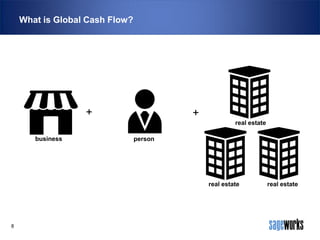

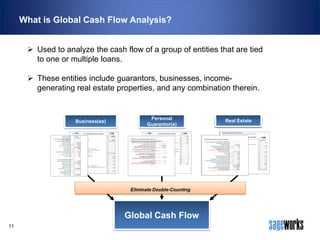

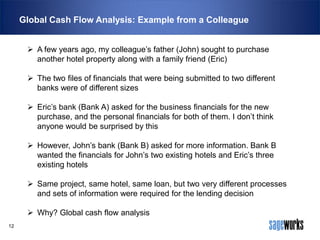

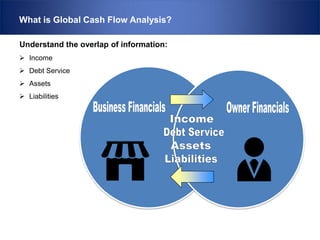

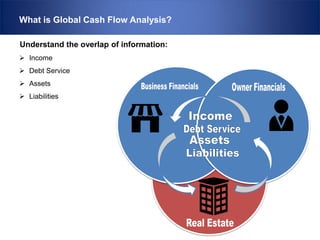

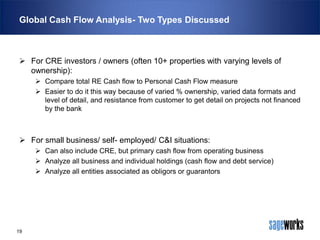

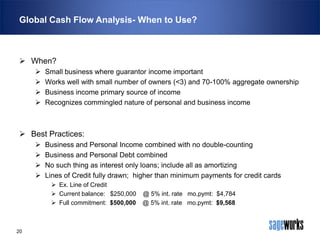

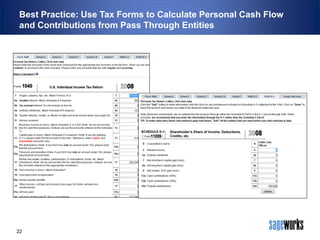

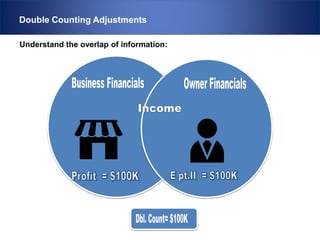

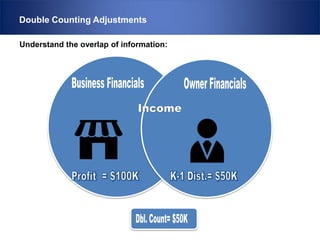

This document summarizes a presentation on global cash flow analysis. It discusses analyzing the combined cash flow of interconnected entities like businesses, property, and personal finances. Global cash flow analysis is important to get an accurate picture of debt and income when entities' finances are combined. The presentation covers why and when to use global cash flow analysis, how to perform it, best practices, and common mistakes. It emphasizes combining income and debt sources, avoiding double-counting, and using tax forms to calculate personal cash flow contributions.