Downloaded 105 times

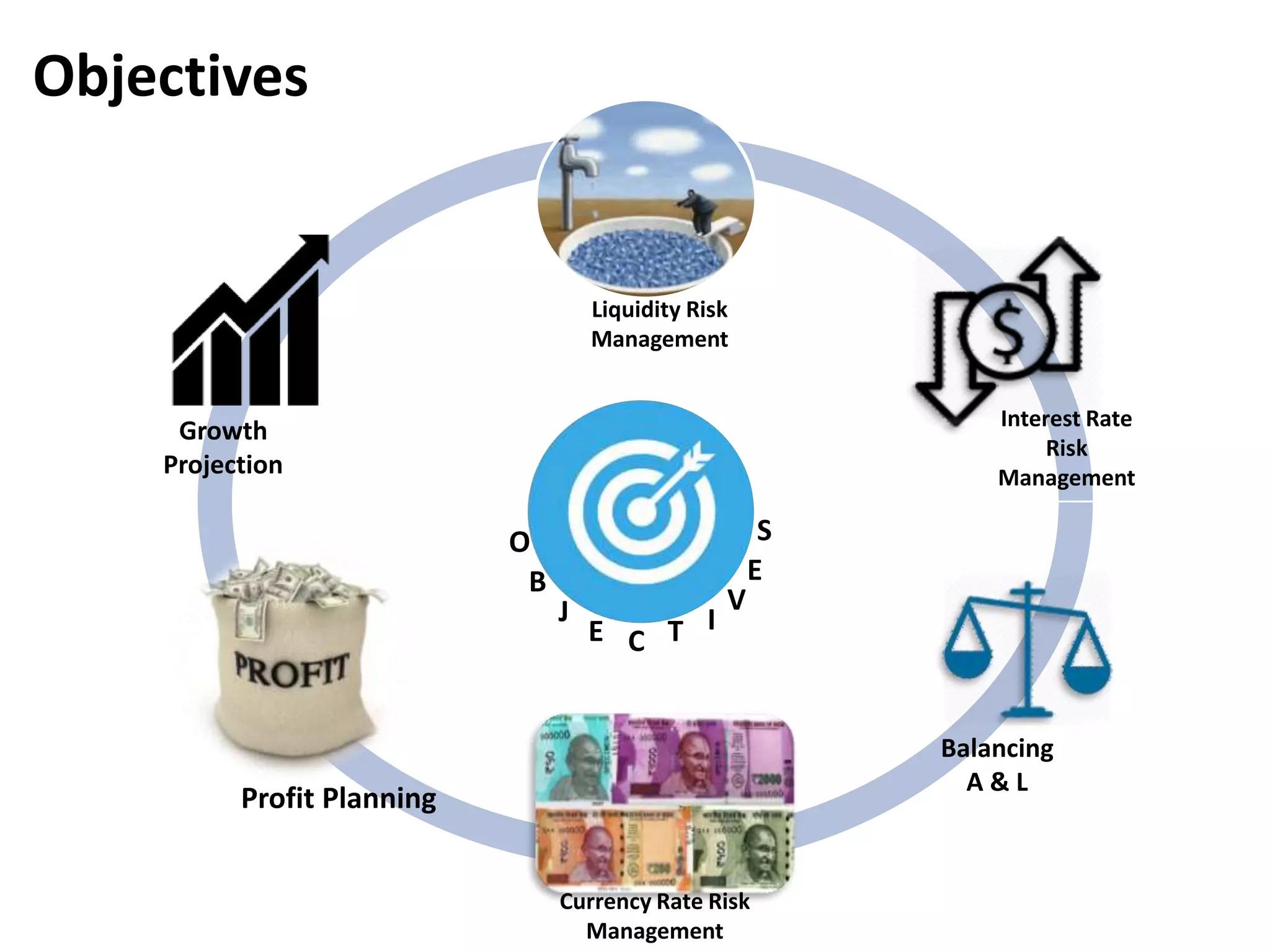

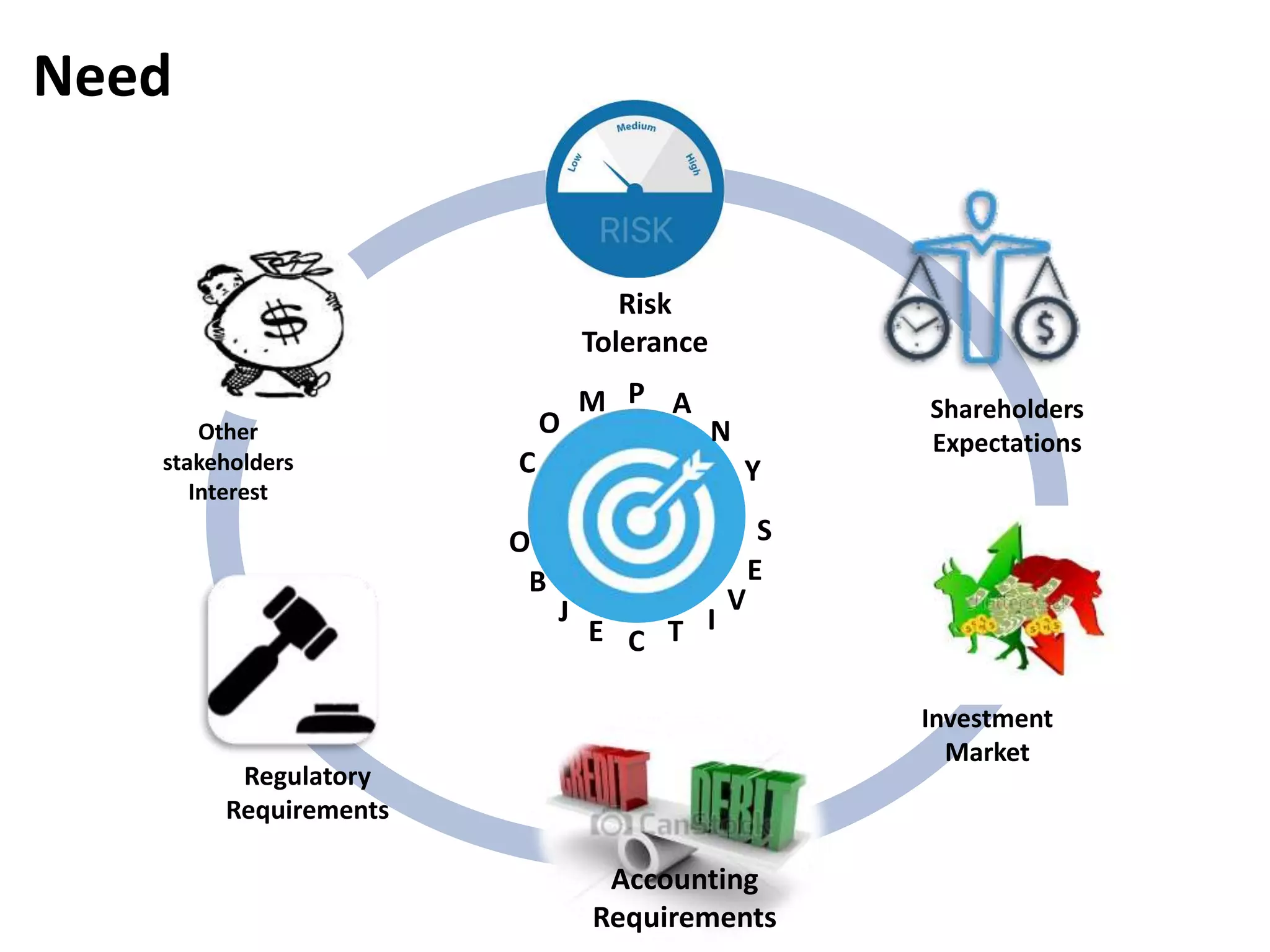

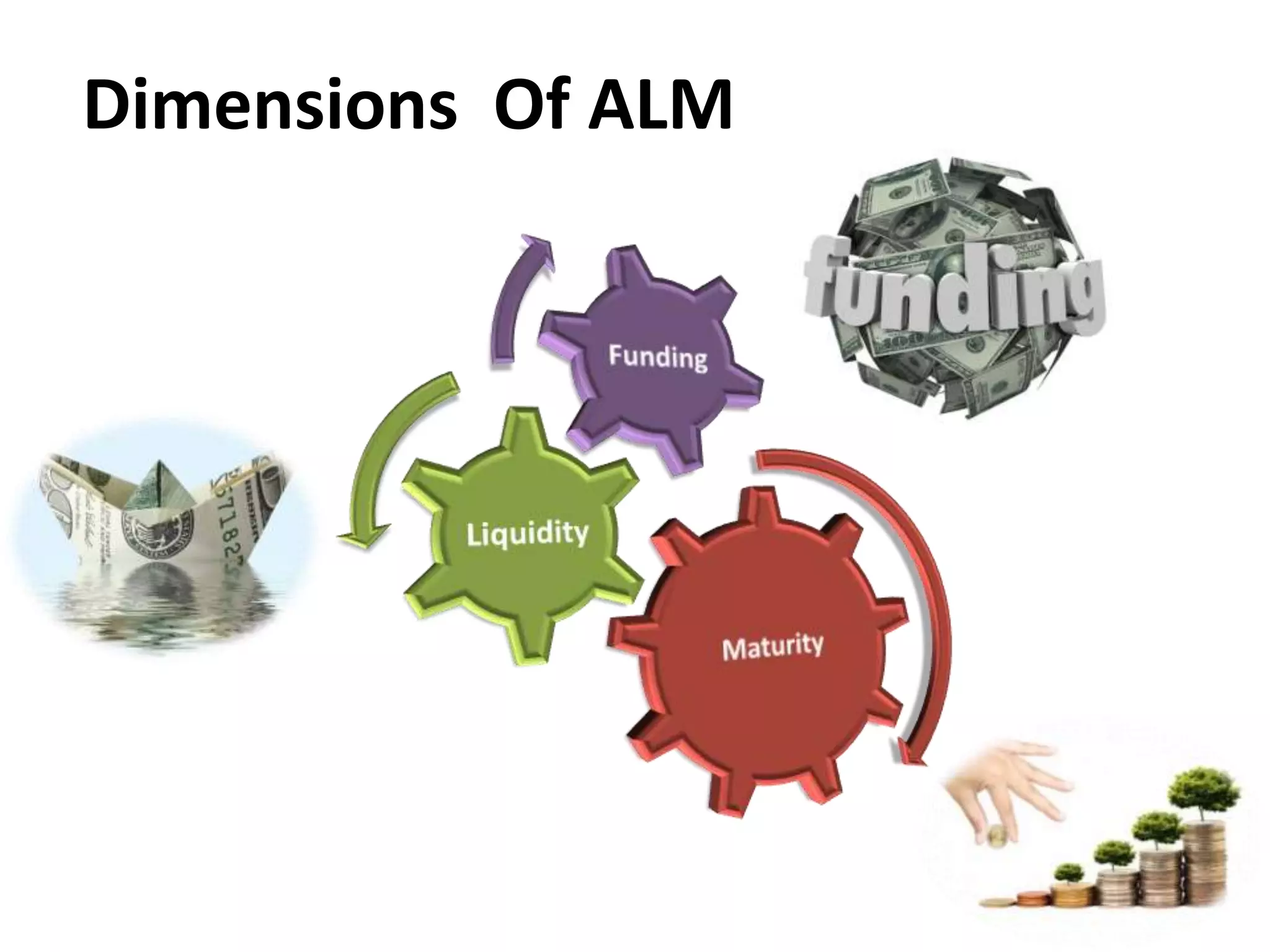

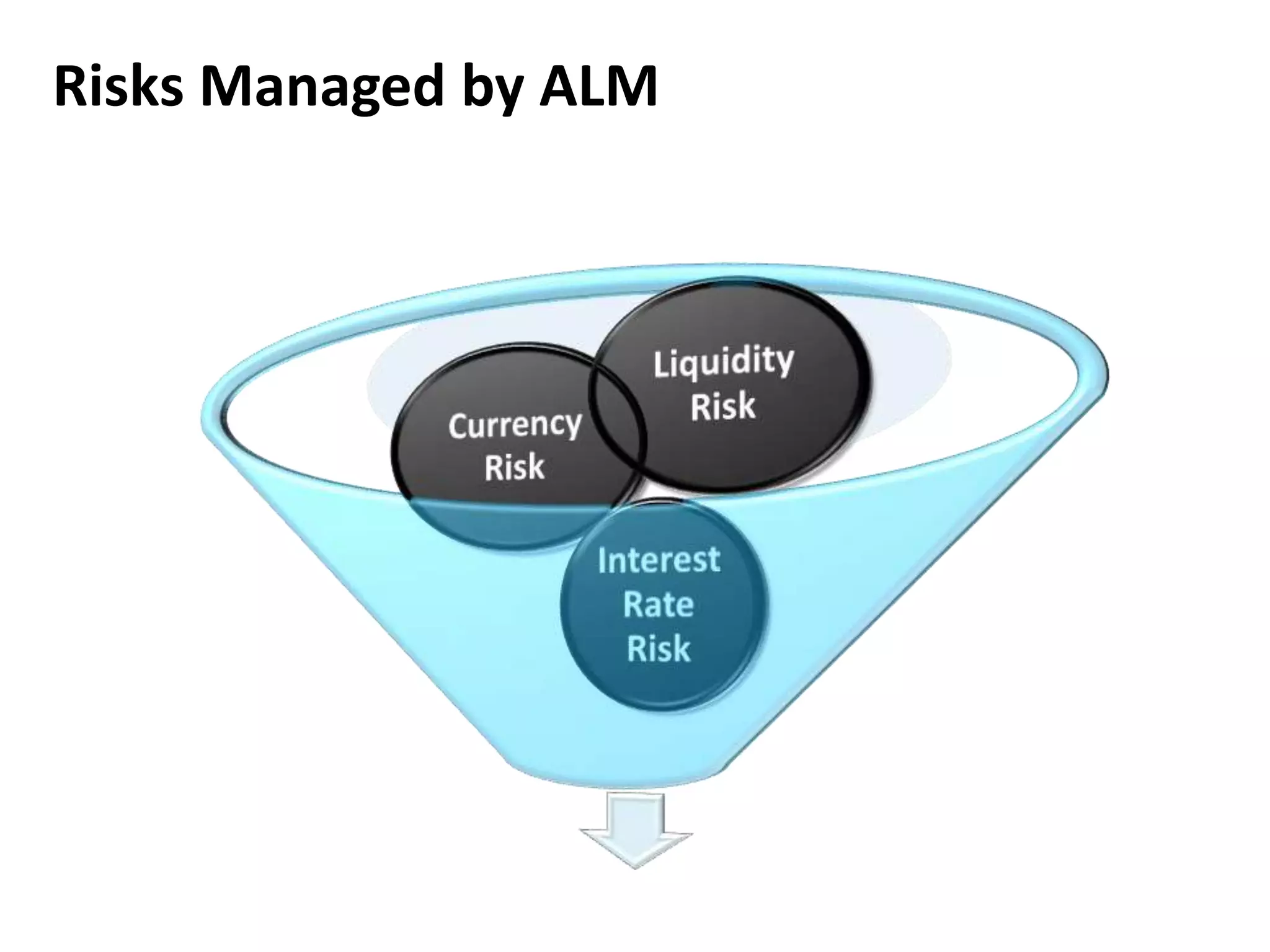

Asset liability management (ALM) is the process of managing a bank's assets and liabilities to maximize profits and minimize risk. It involves planning asset and liability maturities and interest rates to ensure adequate liquidity and stable net interest income. The ALM process includes risk identification, measurement, and management of liquidity risk, interest rate risk, currency risk, and other risks. Banks use ALM techniques like maturity gap analysis, duration analysis, simulation, and value at risk to measure different types of risks. The asset liability committee (ALCO) oversees the ALM process and makes strategic decisions about the balance sheet, pricing, and risk management.