Download as PDF, PPTX

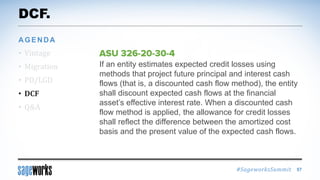

The document outlines a webinar presented by Sageworks on CECL methodology, addressing critical components such as attrition, prepayment, data requirements, and forecasting. It emphasizes the importance of methodologies in risk management for financial institutions and details the agenda for upcoming sessions. Legal disclaimers regarding the use of forward-looking statements and the accuracy of industry data are also included.