Downloaded 22 times

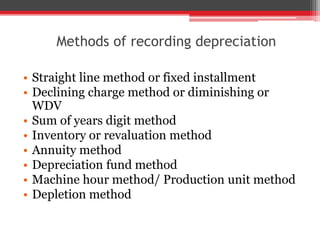

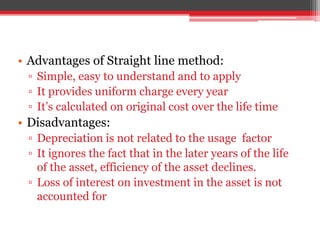

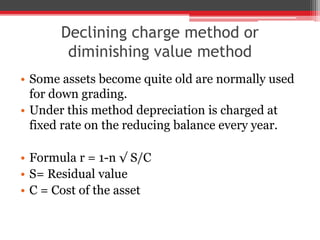

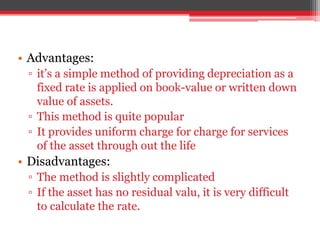

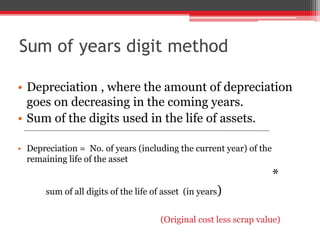

This document discusses depreciation, including its concept, objectives, causes, and methods of calculation. Depreciation refers to the reduction in value of fixed assets due to wear and tear, age, and obsolescence. The objectives of depreciation include calculating proper profits, showing the asset at a reasonable value, and maintaining the original investment. Common causes are internal wear and external obsolescence. Main methods of calculating depreciation discussed are the straight-line method, declining balance method, and sum-of-years' digits method.