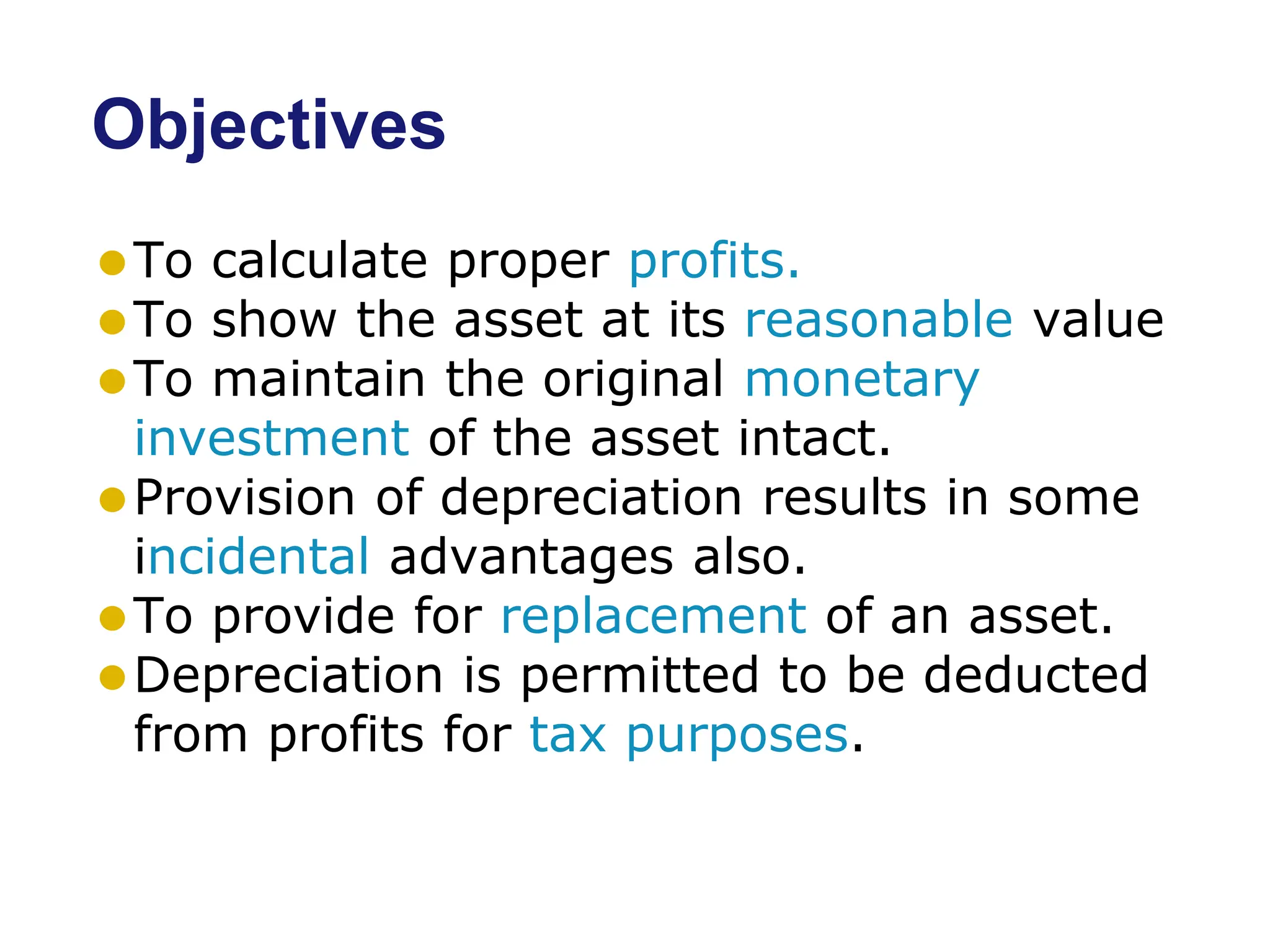

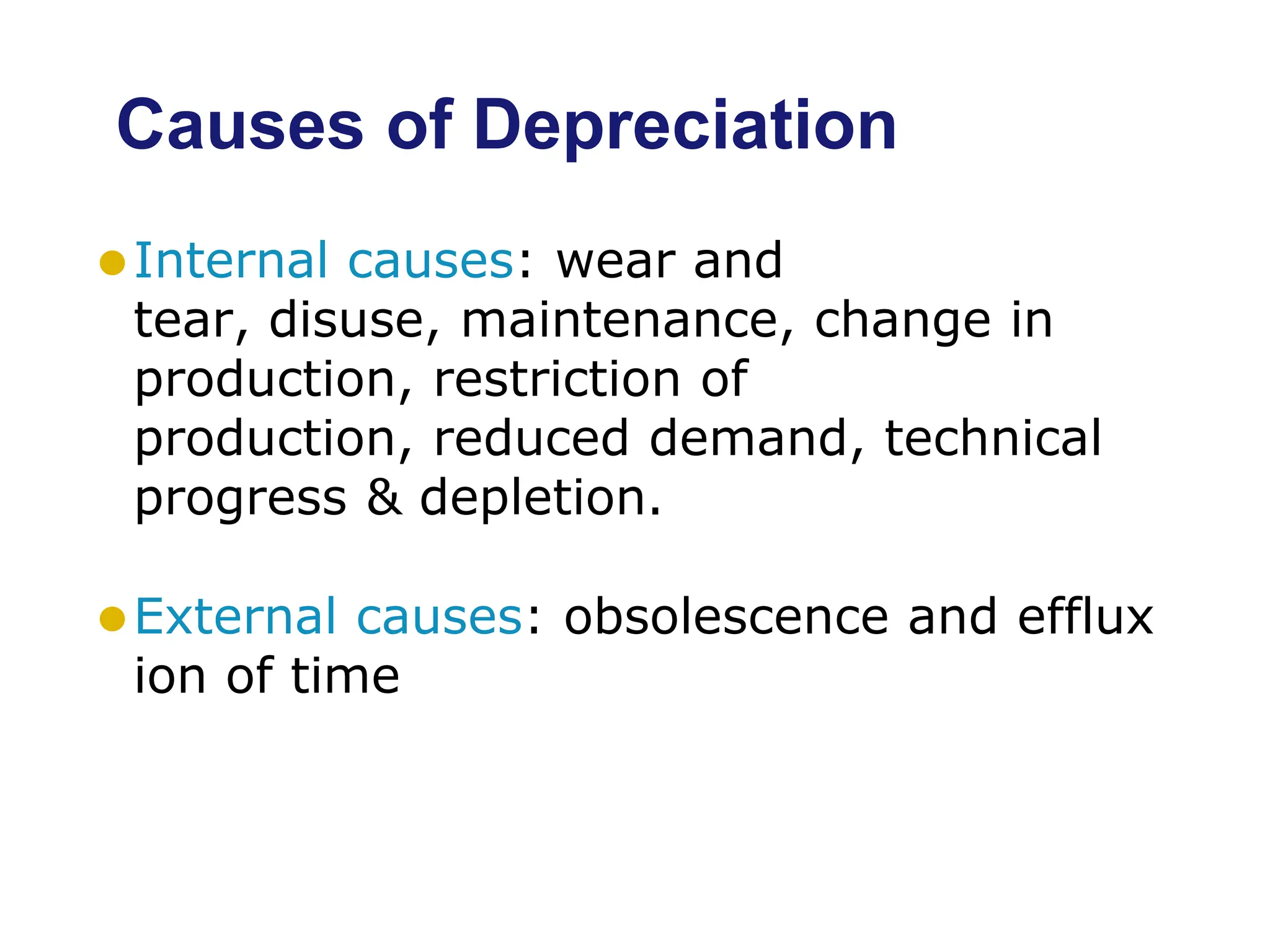

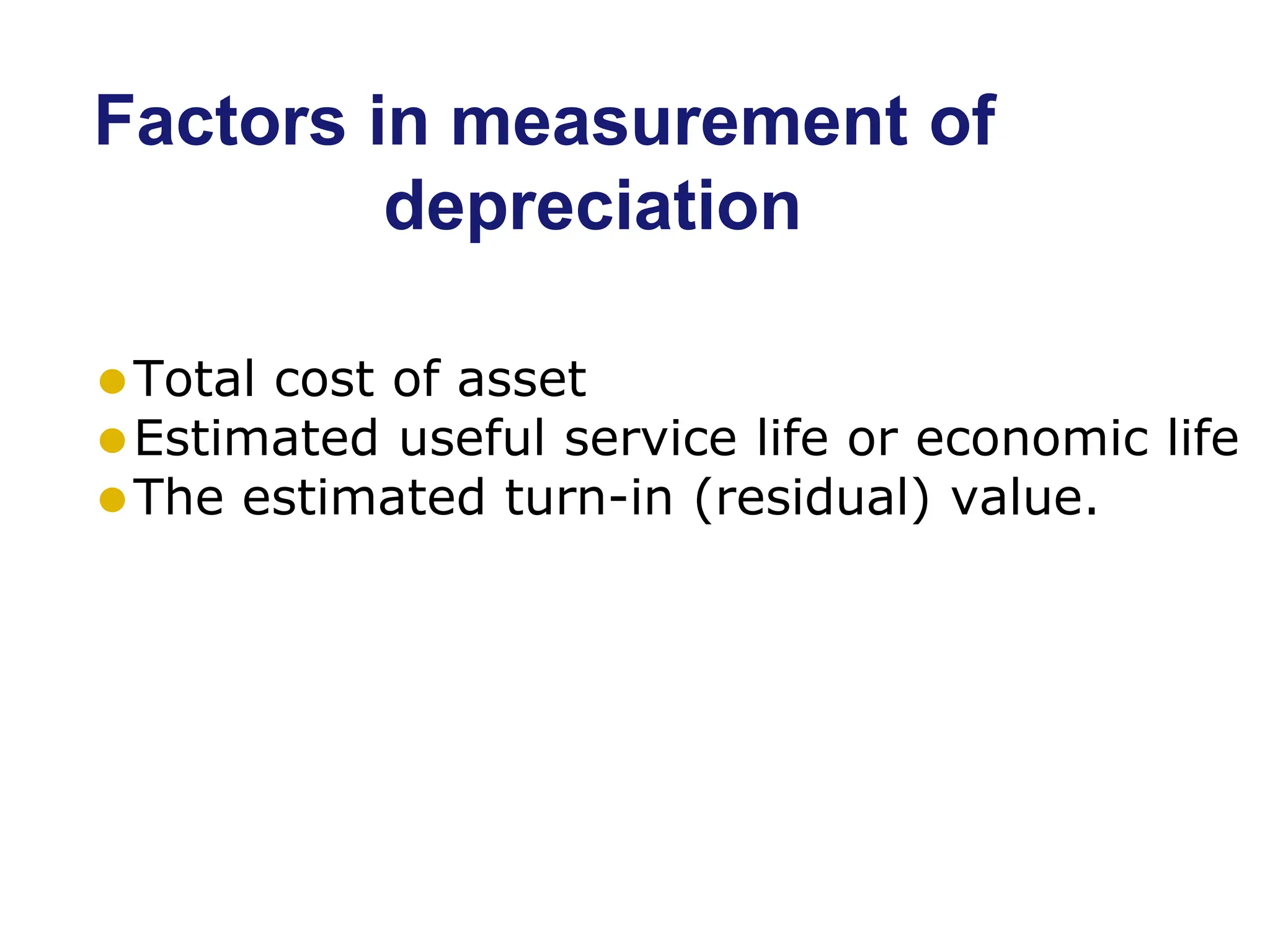

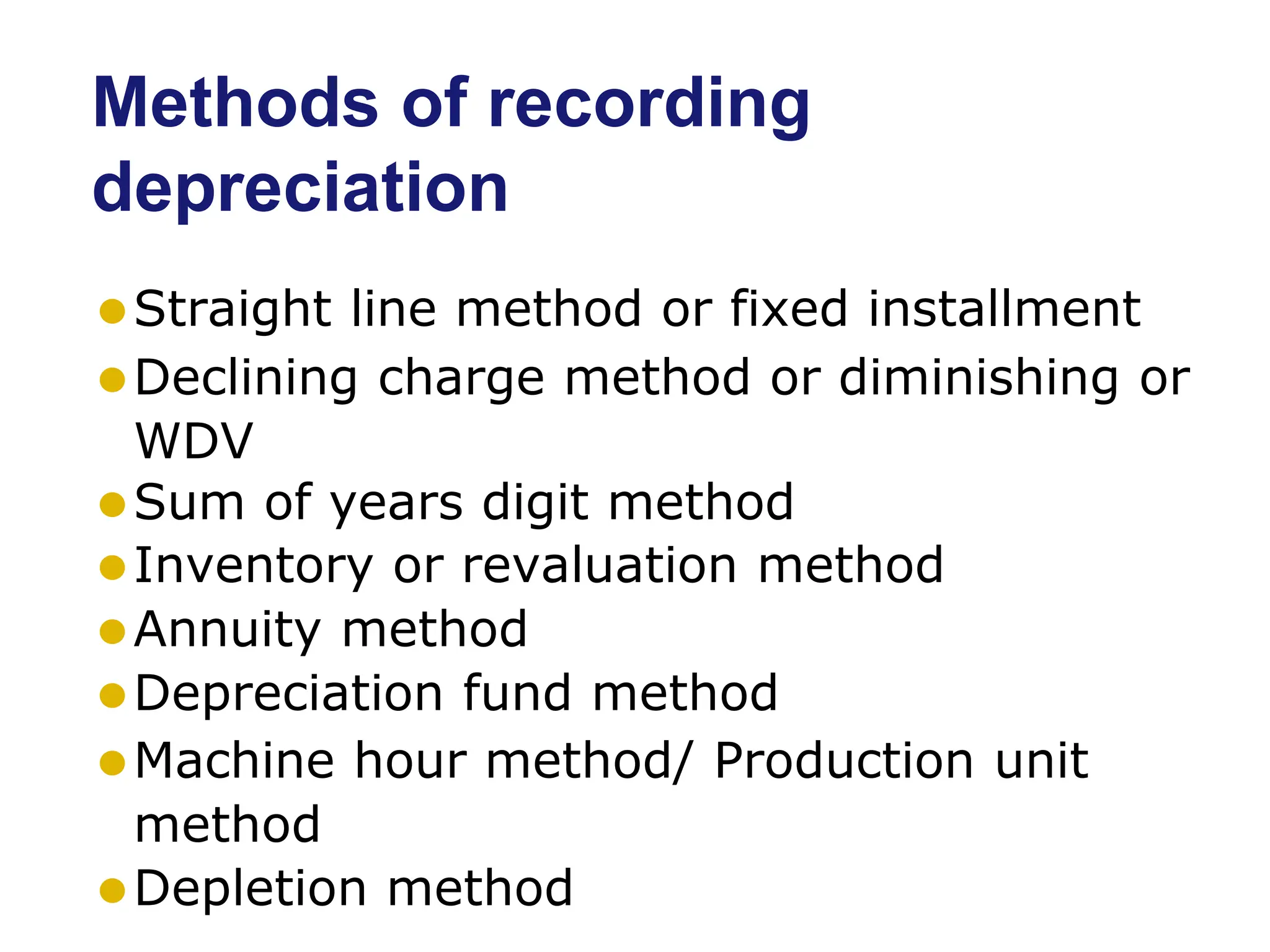

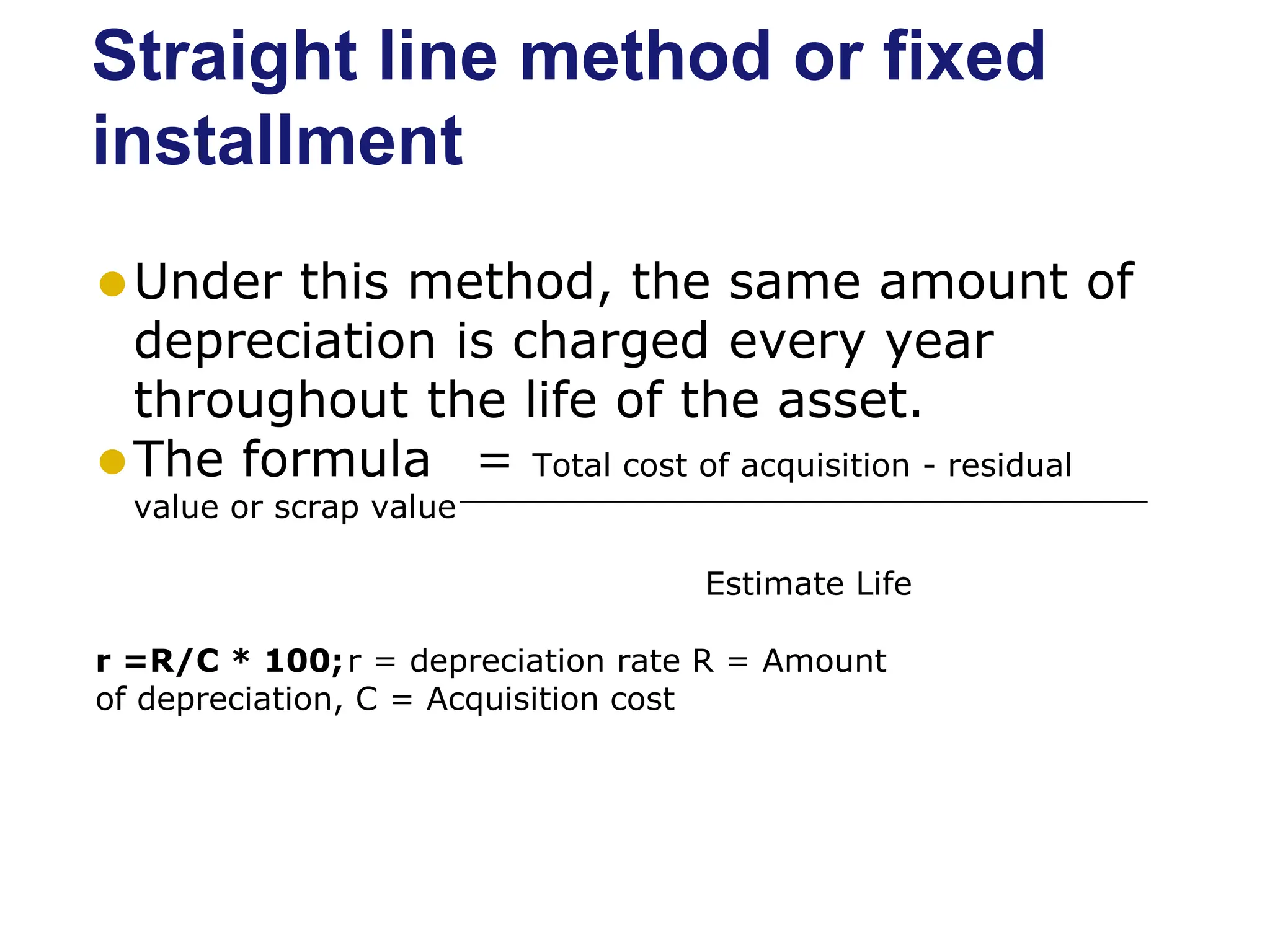

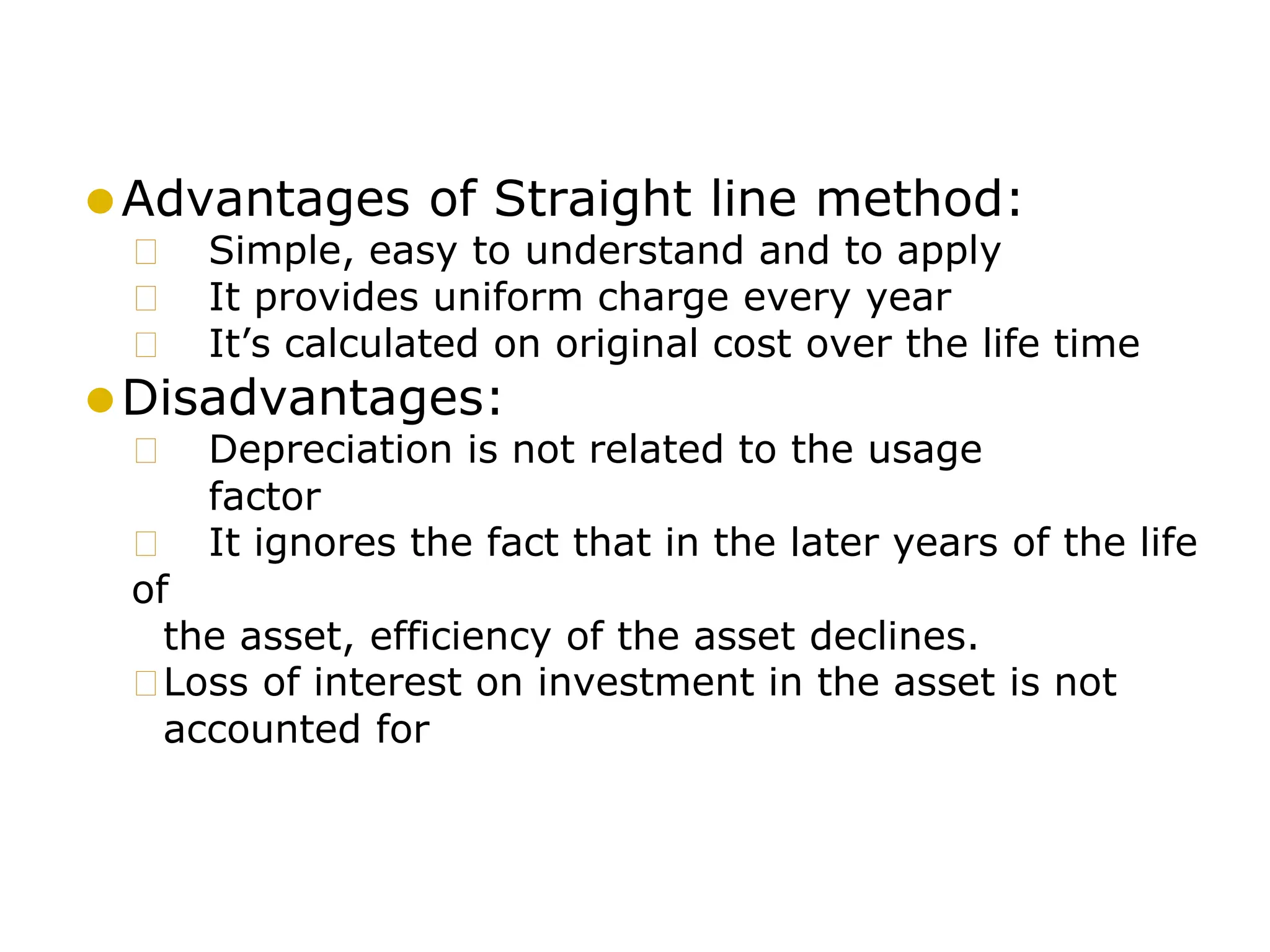

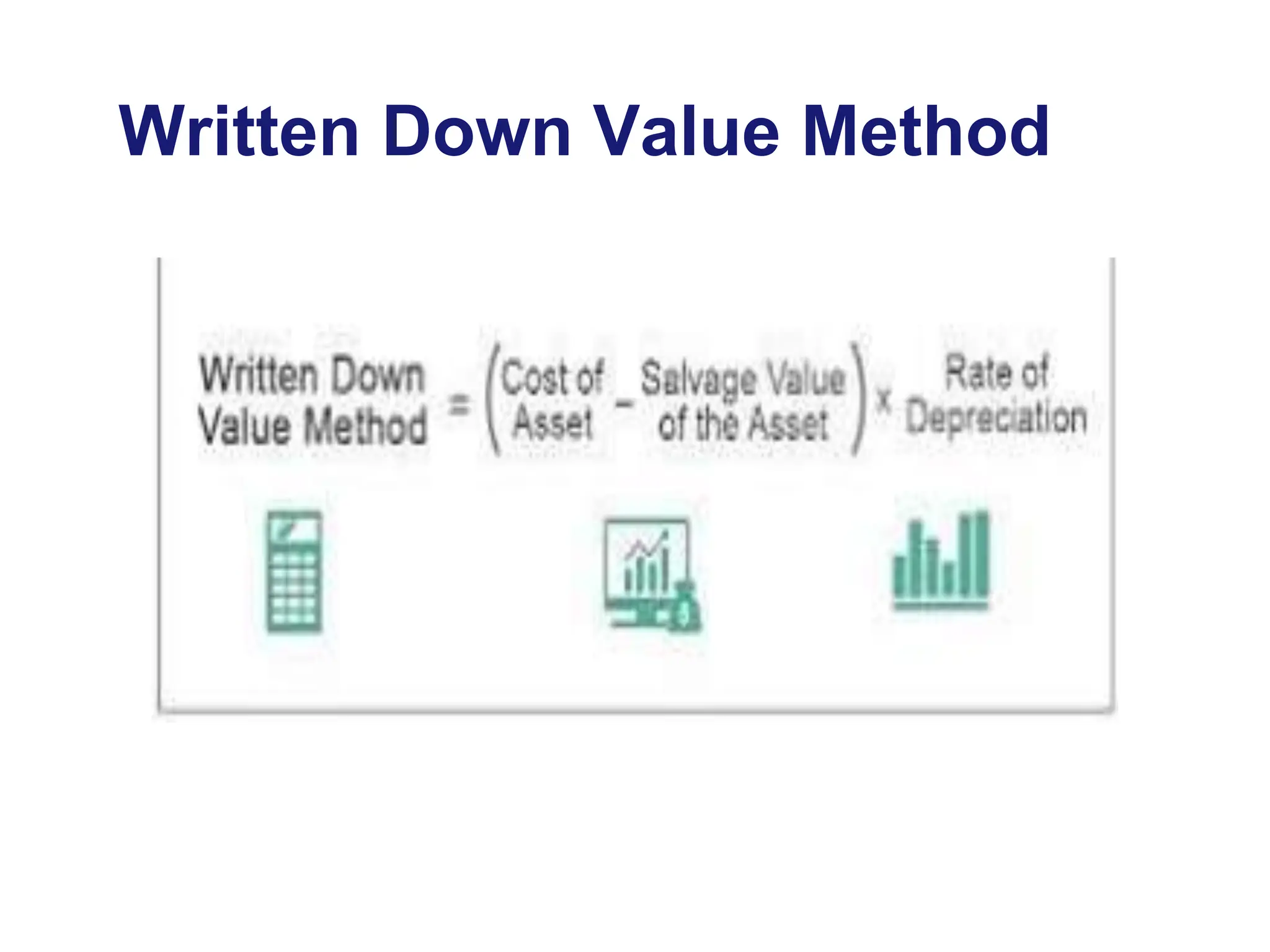

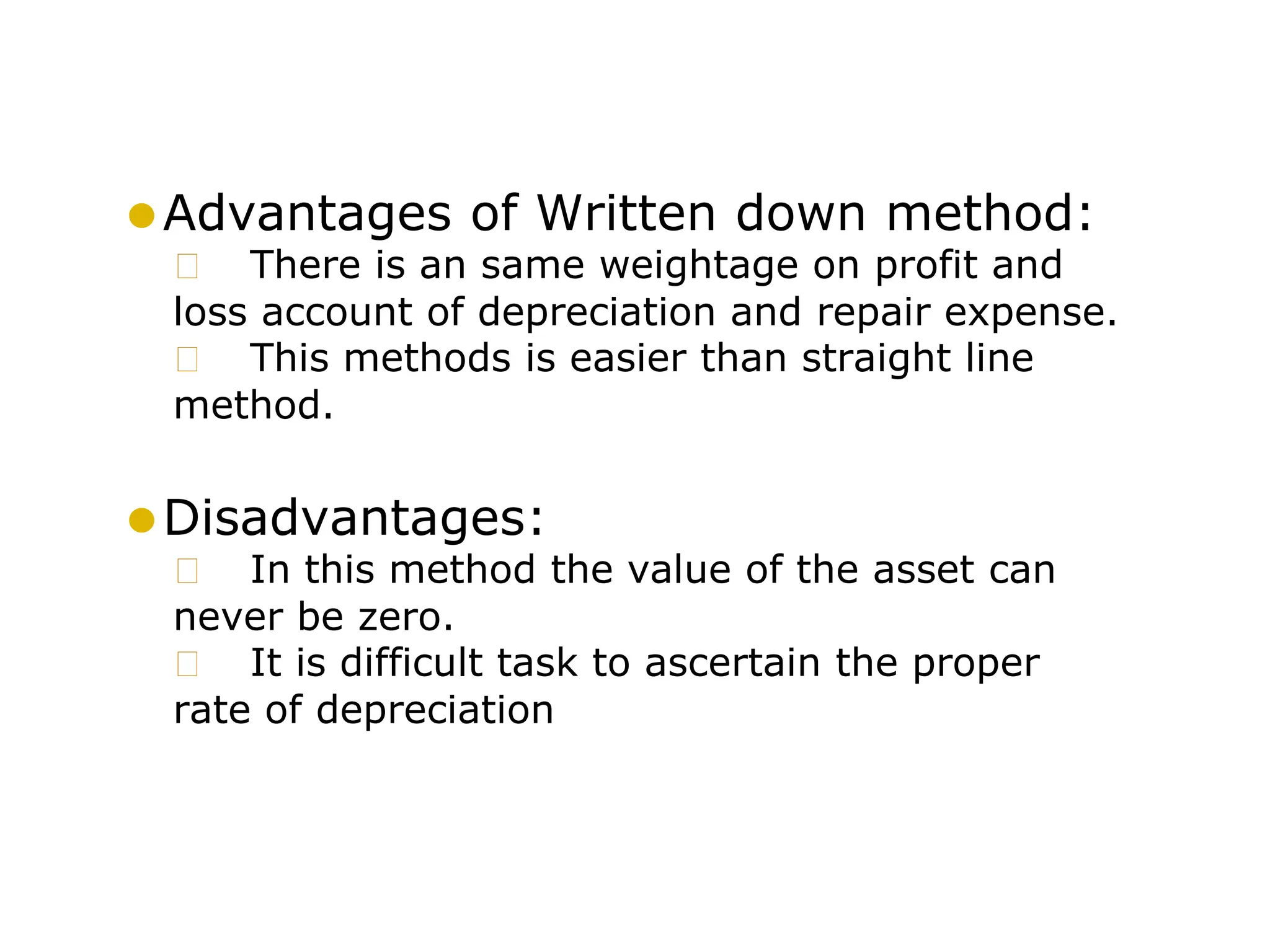

This document summarizes key concepts related to depreciation. It defines depreciation as the cost of lost usefulness or diminution of an asset over time due to wear and tear, consumption, or obsolescence. The objectives of depreciation include calculating proper profits, showing assets at reasonable value, and maintaining the original investment. Causes of depreciation include internal factors like wear and tear as well as external factors like obsolescence. Common methods for recording depreciation discussed are the straight line method, declining balance method, and sum of years digits method.