Download to read offline

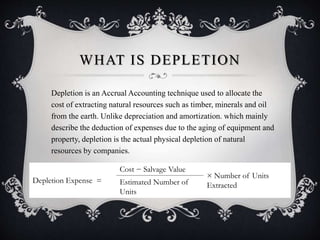

Our group's topic is accounting concepts related to depreciation, depletion, and amortization. Depreciation allocates the cost of a tangible asset over its useful life for tax and accounting purposes. It allows businesses to ascertain true profits, report accurate financial positions, replace assets, and save on taxes. Depletion allocates the cost of extracting natural resources by calculating the depletion expense based on units extracted over total estimated units. Amortization refers to paying off debt or allocating capital expenses of intangible assets over their useful lives, such as allocating loan principal payments over time or expensing a patent cost over its 15-year life.