Downloaded 4,200 times

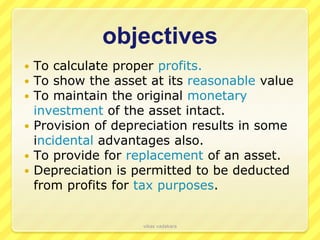

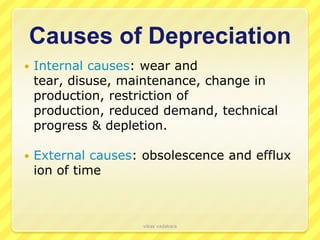

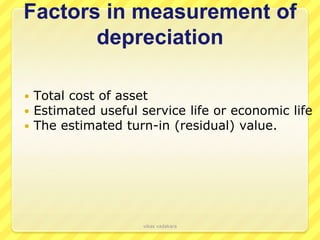

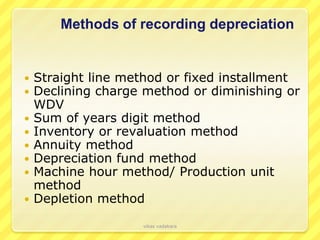

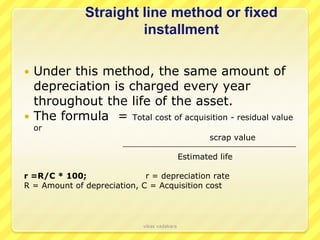

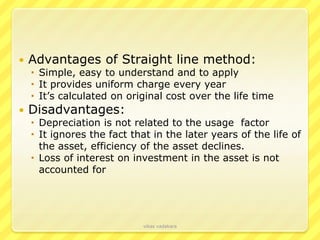

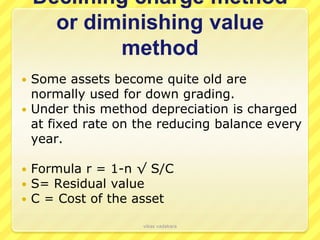

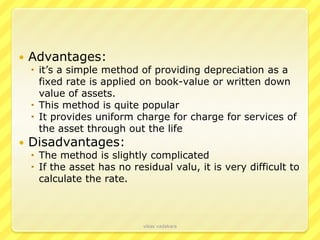

This document discusses depreciation, including its concept, objectives, causes, and methods. It defines depreciation as the permanent fall in value of fixed assets due to wear and tear from use in business. The objectives of depreciation include calculating proper profits, maintaining the original investment, and providing for asset replacement. Causes include wear and tear, obsolescence, and the passage of time. Common depreciation methods discussed are the straight-line method, declining balance method, and sum of years digits method.