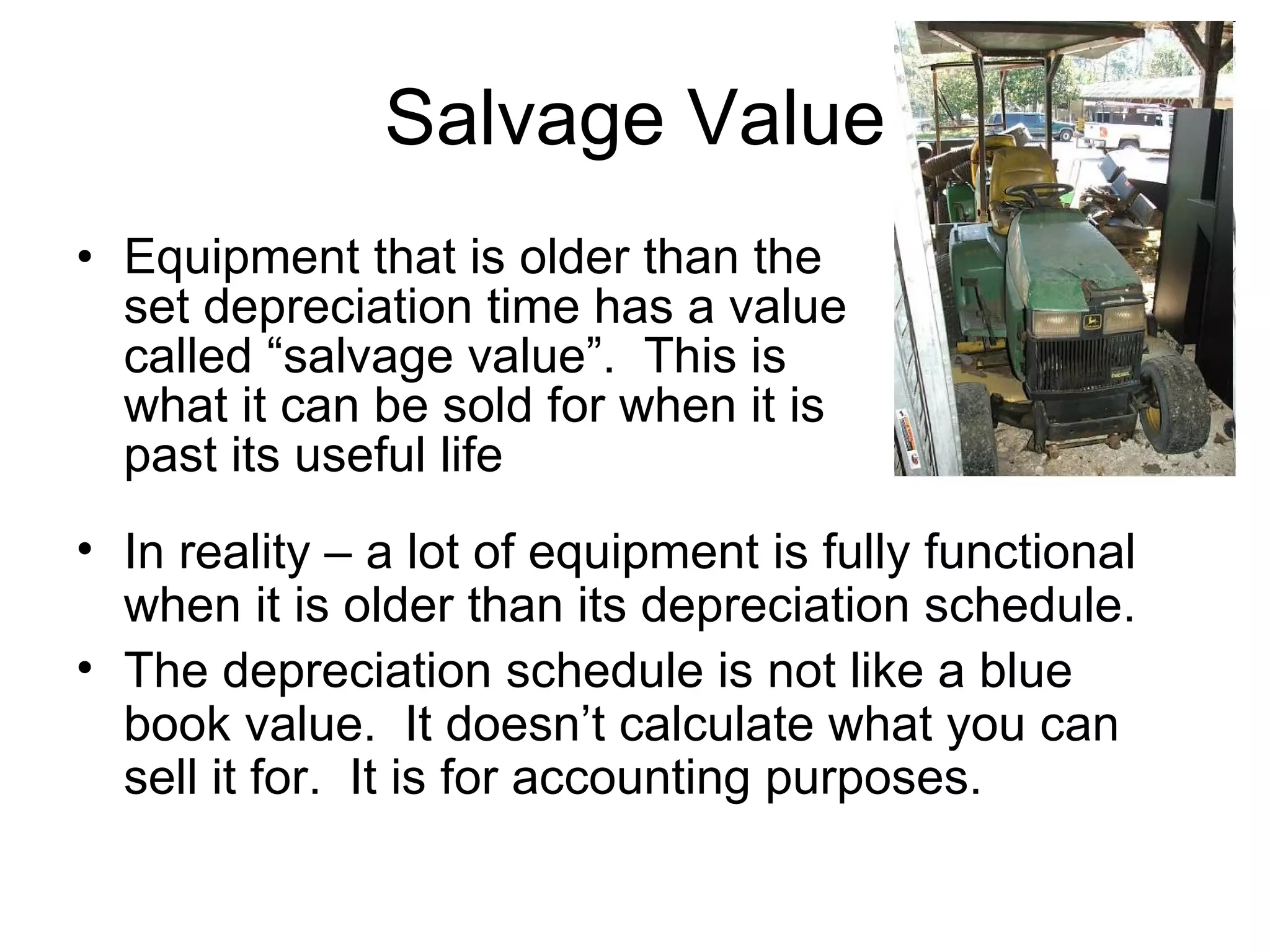

The document discusses depreciation of landscape equipment and vehicles for accounting purposes. It provides examples of how to calculate annual depreciation using the formula of new price minus salvage value divided by total useful life in years. A zero turn mower purchased for $4,500 in 2009 would be worth $3,892.86 in 2011 after depreciating $607.14 per year over its 7 year life. A used truck purchased for $7,500 in 2008 would be worth $4,700 in 2010 after depreciating over its 5 year life with a $500 salvage value.