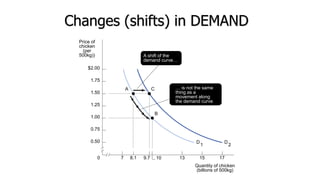

The document outlines the key assumptions and concepts of the supply and demand model. It assumes rational behavior by market participants and that all other factors remain constant ("ceteris paribus"). It defines demand as the quantity willing and able to be purchased at a given price. The law of demand states that, ceteris paribus, quantity demanded decreases when price rises and increases when price falls. Shifts in the demand curve represent changes in demand from non-price factors like number of buyers, income levels, prices of related goods, preferences, and expectations.