Prices of RelatedProducts

• Changes in prices of related goods

• The direction in which demand would

change depends on the relationships

of products.

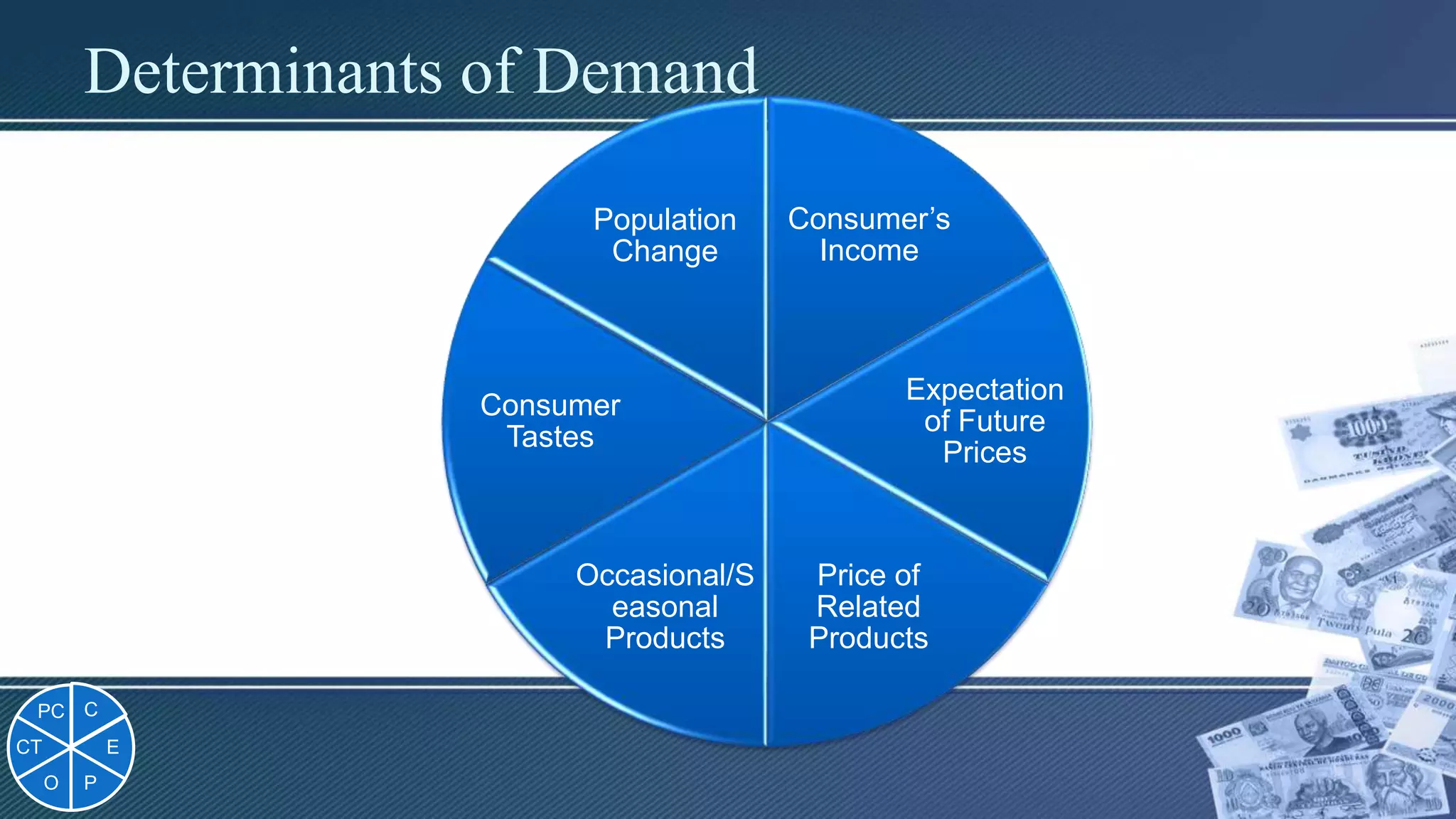

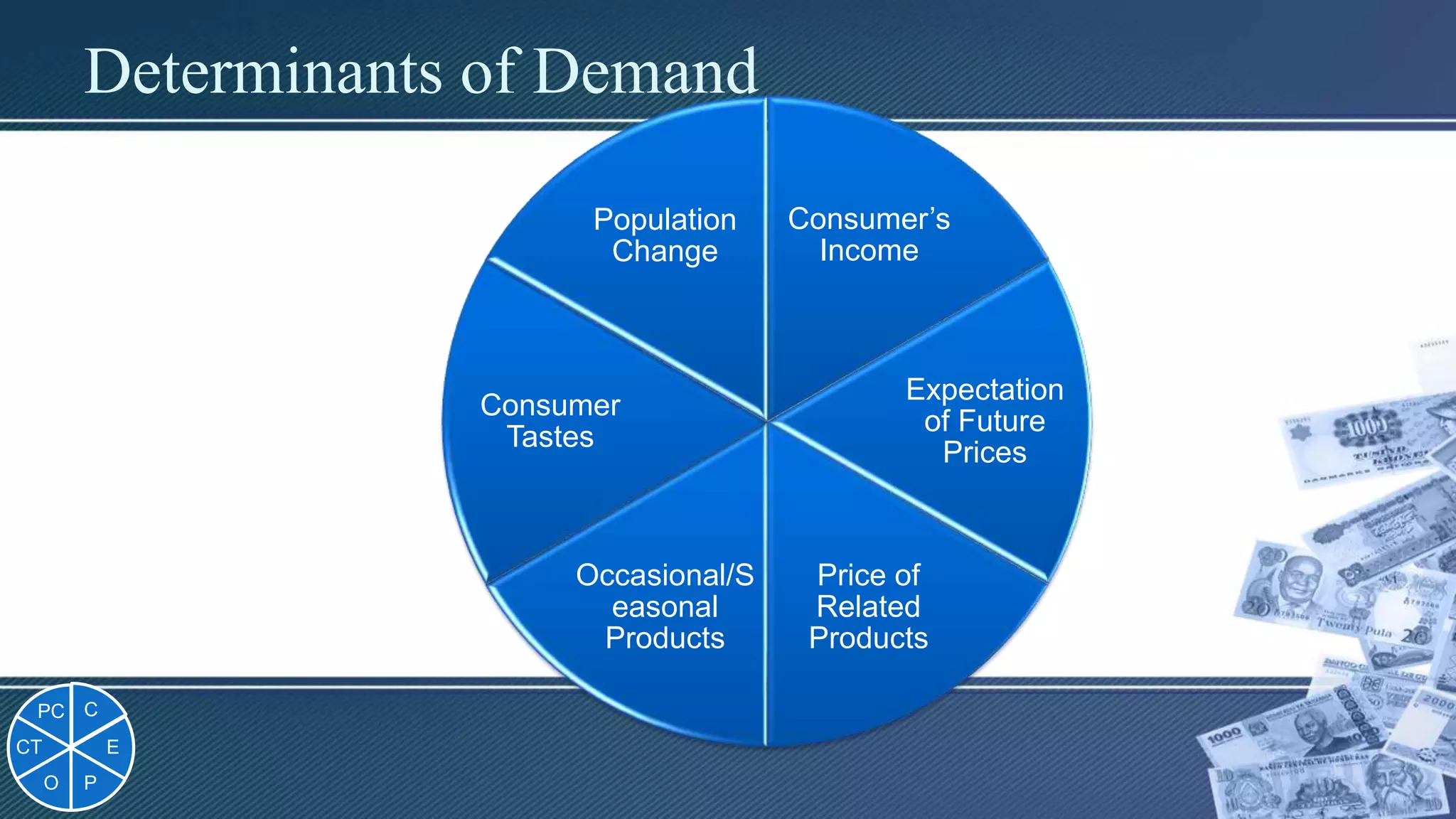

C

E

P

O

CT

PC

22.

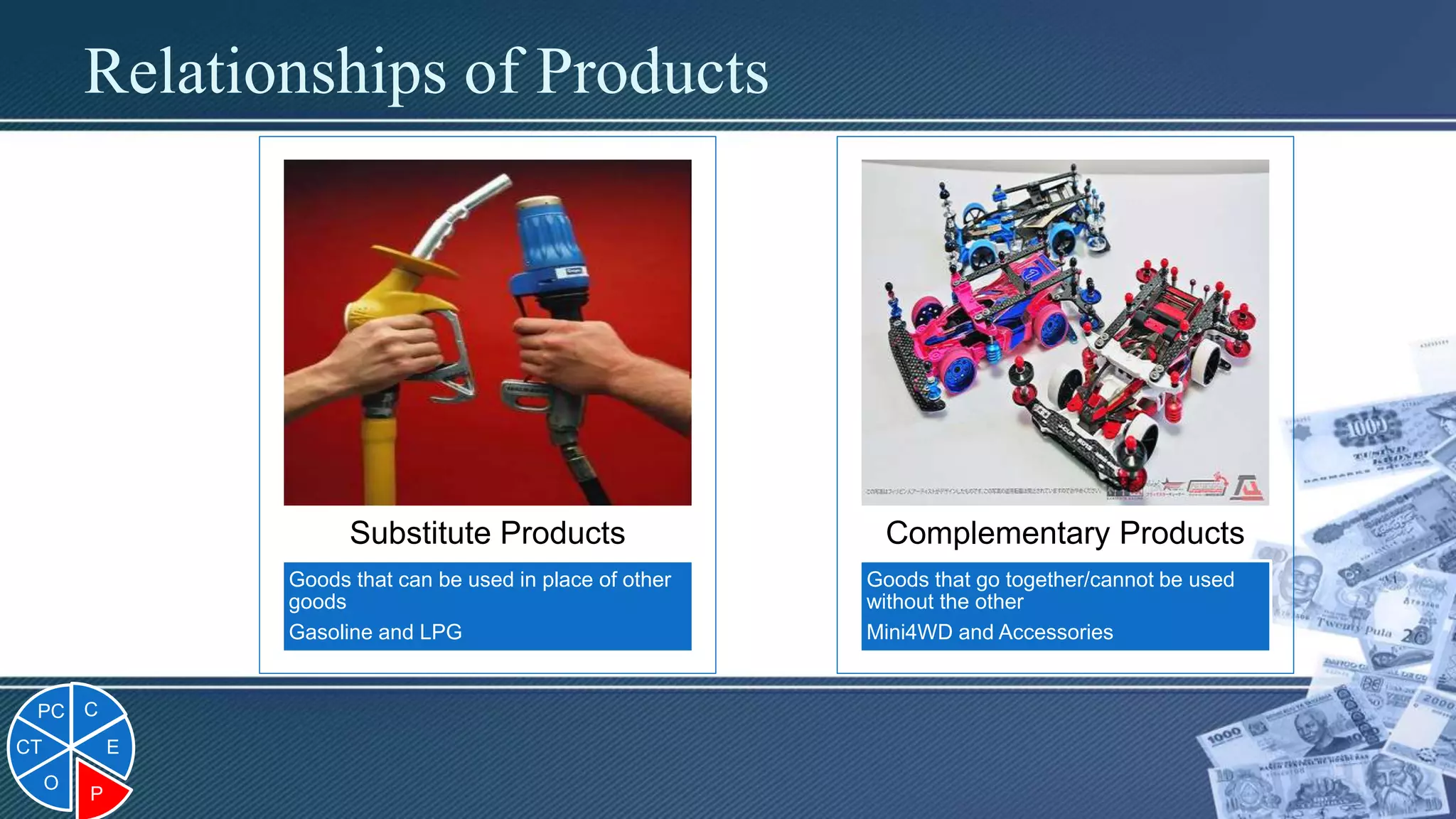

Relationships of Products

Goodsthat can be used in place of other

goods

Gasoline and LPG

Substitute Products

Goods that go together/cannot be used

without the other

Mini4WD and Accessories

Complementary Products

C

E

P

O

CT

PC

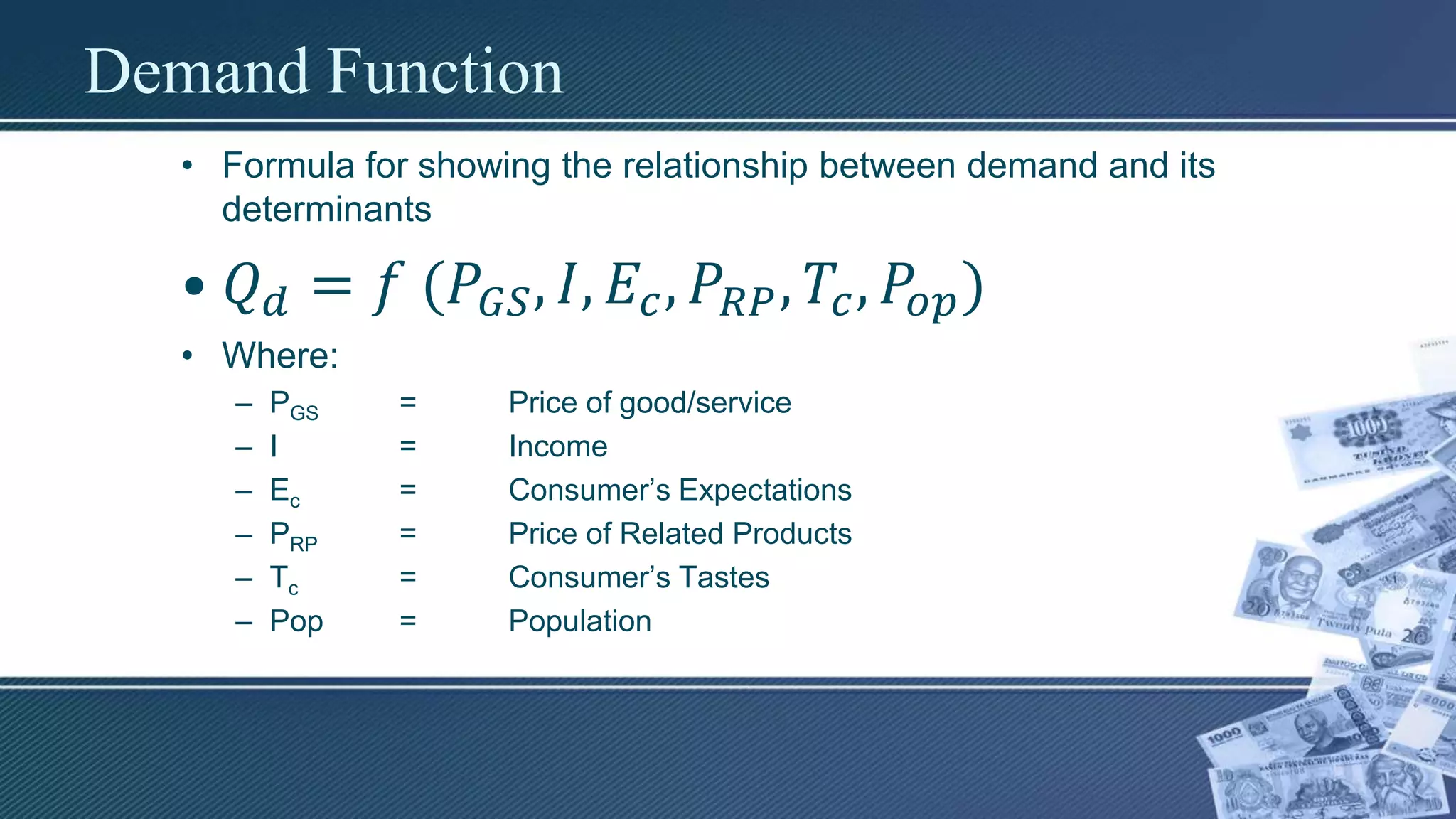

Demand Function

• Formulafor showing the relationship between demand and its

determinants

• 𝑄 𝑑 = 𝑓 (𝑃𝐺𝑆, 𝐼, 𝐸𝑐, 𝑃𝑅𝑃, 𝑇𝑐, 𝑃𝑜𝑝)

• Where:

– PGS = Price of good/service

– I = Income

– Ec = Consumer’s Expectations

– PRP = Price of Related Products

– Tc = Consumer’s Tastes

– Pop = Population

31.

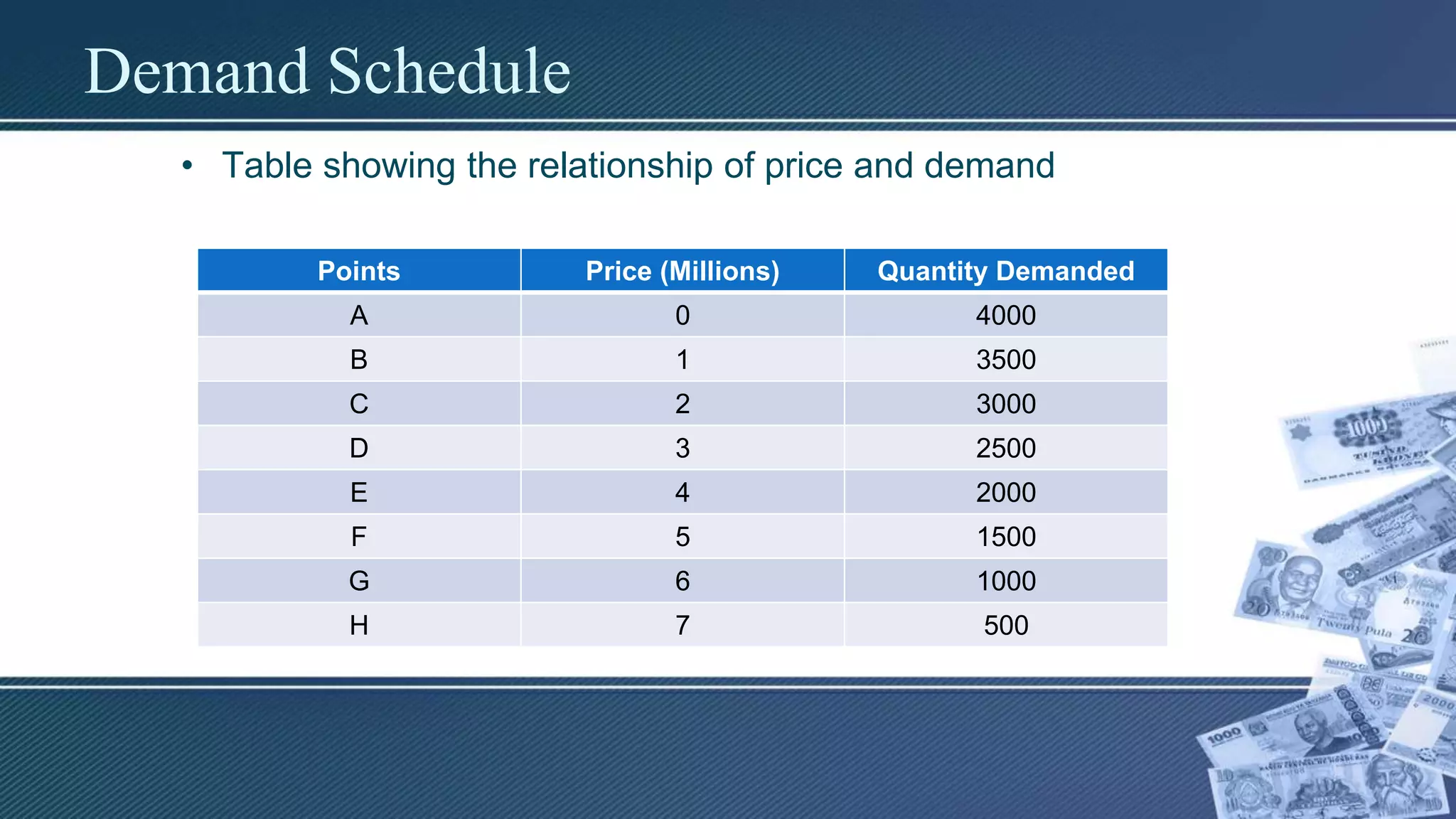

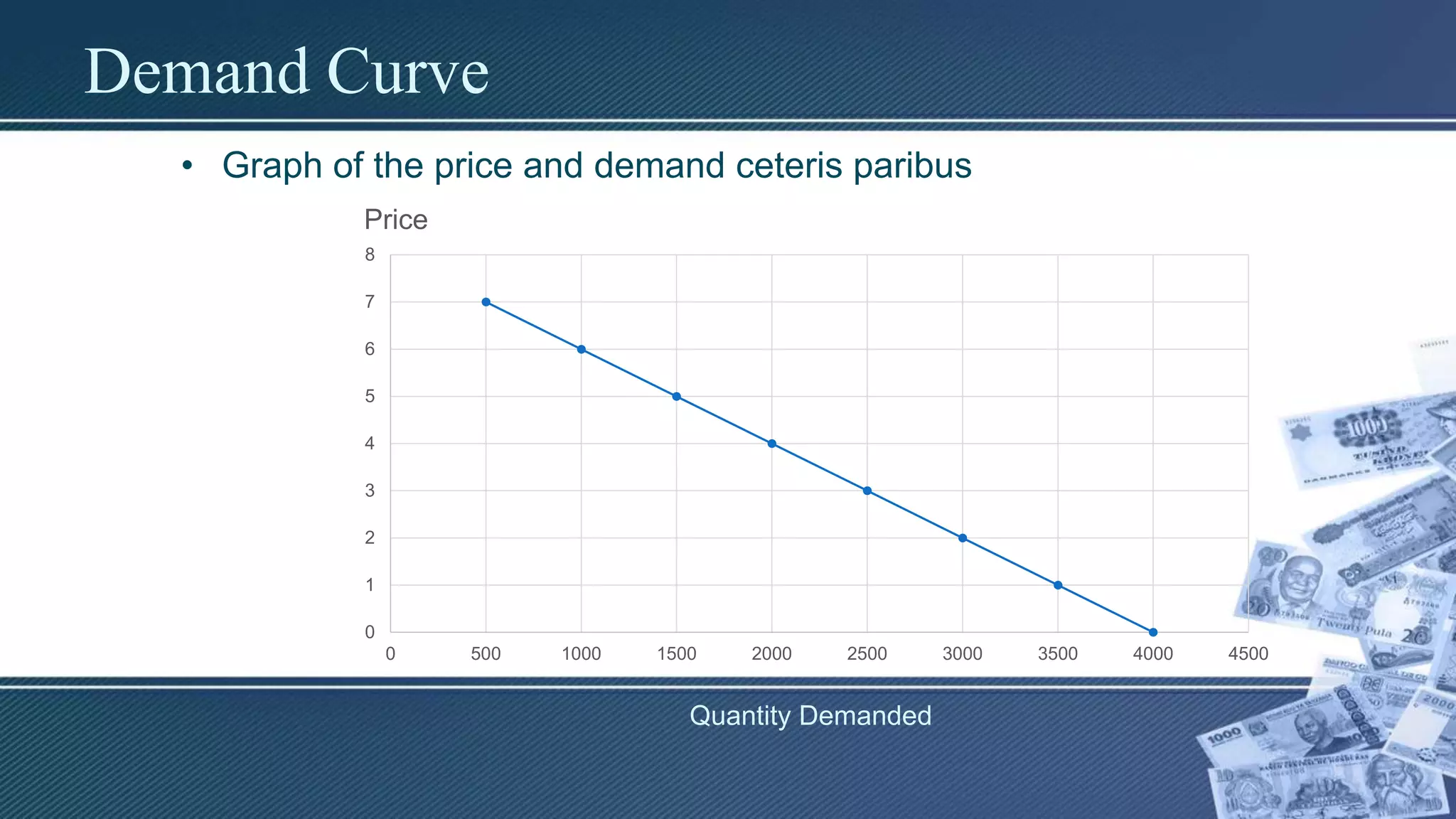

Demand Schedule

• Tableshowing the relationship of price and demand

Points Price (Millions) Quantity Demanded

A 0 4000

B 1 3500

C 2 3000

D 3 2500

E 4 2000

F 5 1500

G 6 1000

H 7 500

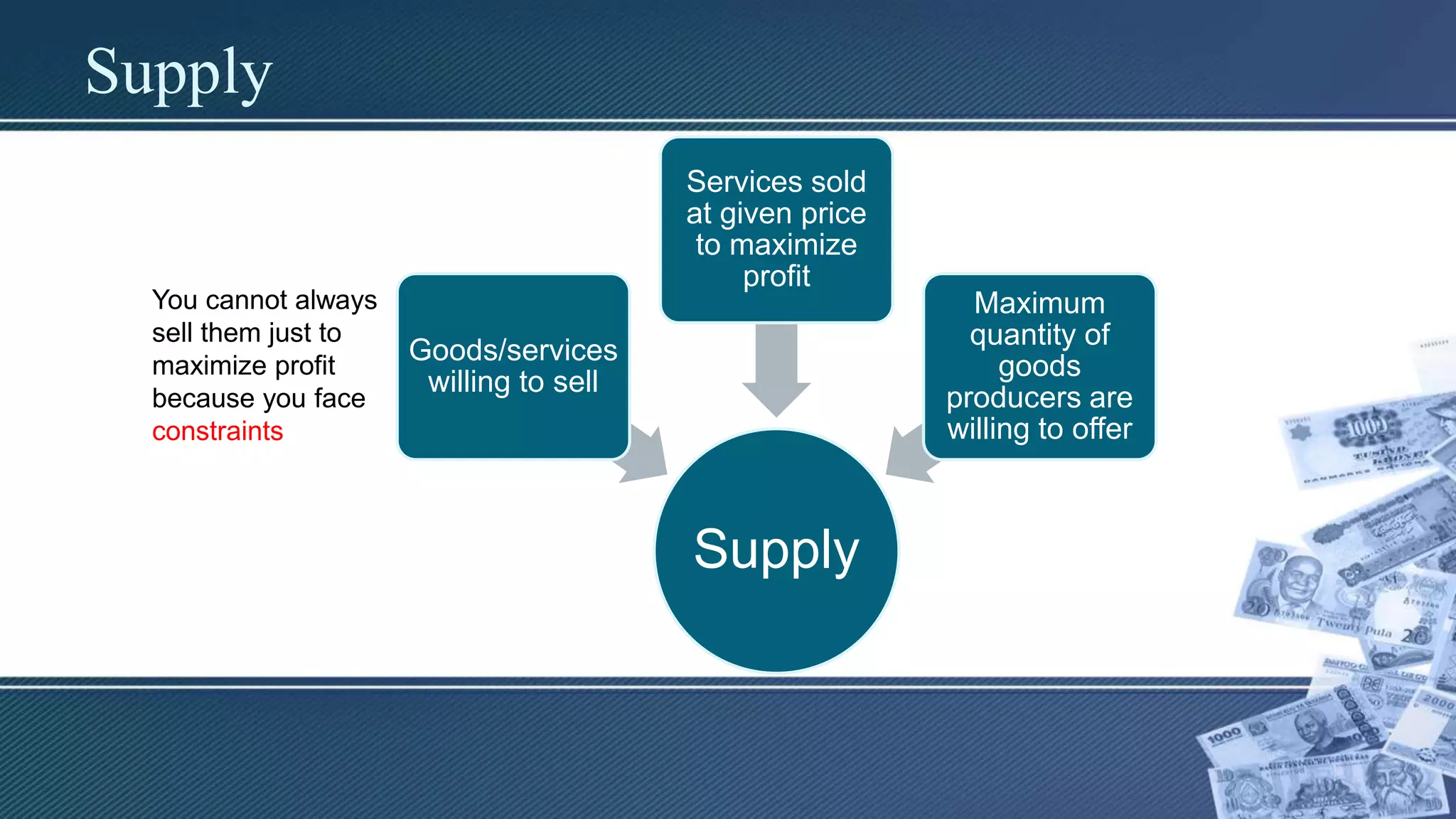

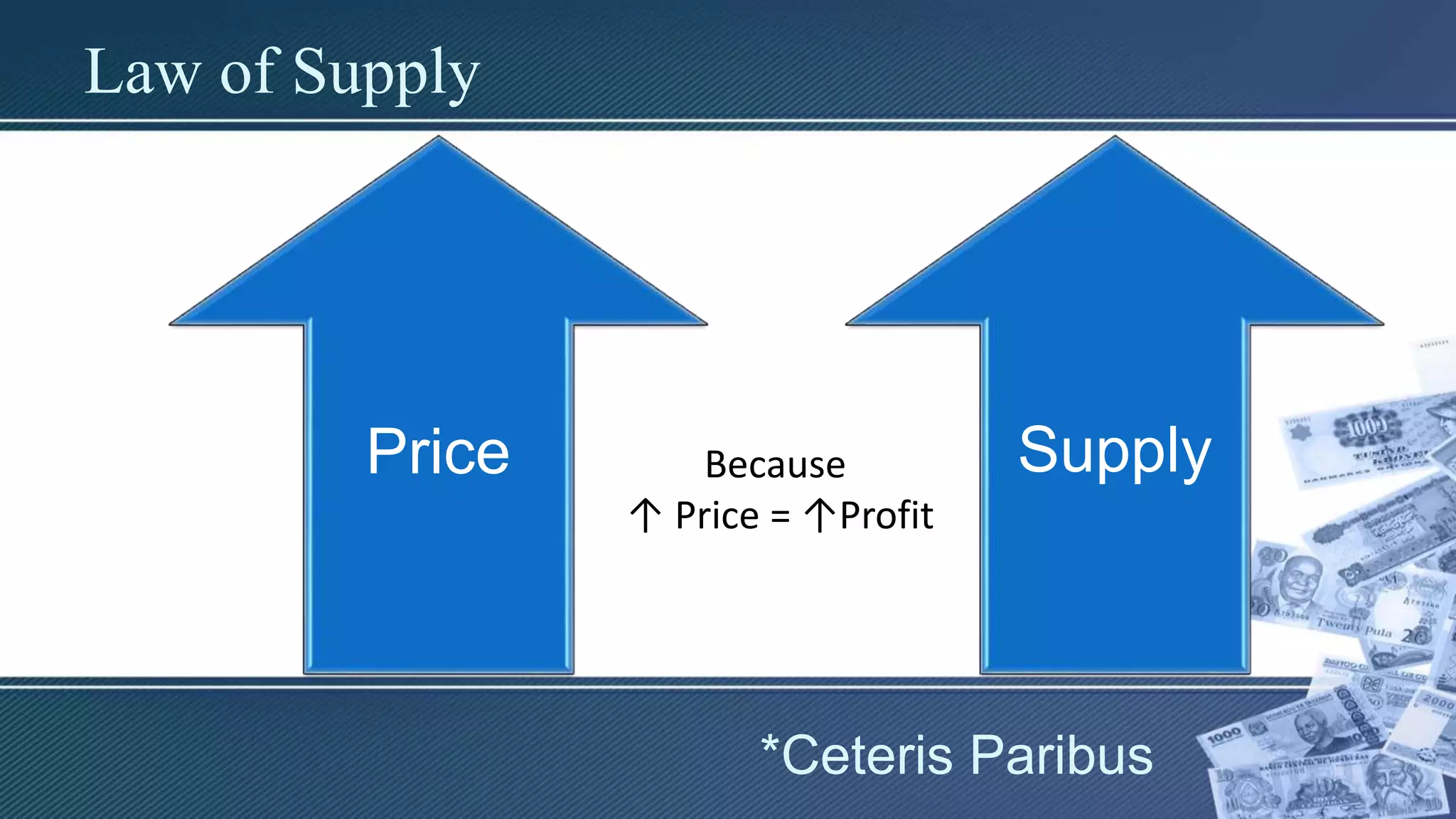

Supply

Supply

Goods/services

willing to sell

Servicessold

at given price

to maximize

profit

Maximum

quantity of

goods

producers are

willing to offer

You cannot always

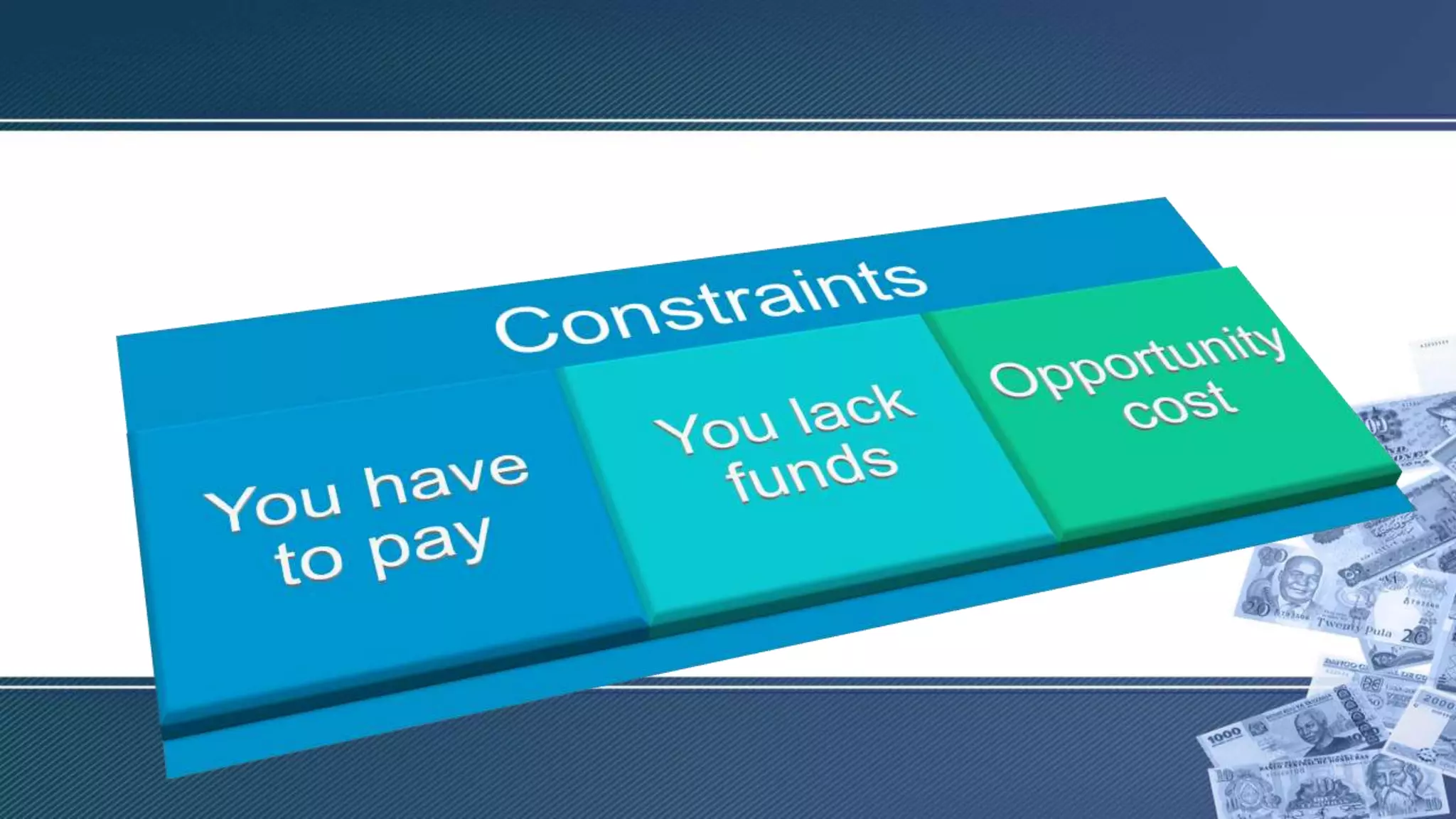

sell them just to

maximize profit

because you face

constraints

36.

Market Price

• Itis the price that the sellers can

charge their product in a

competitive market.

38.

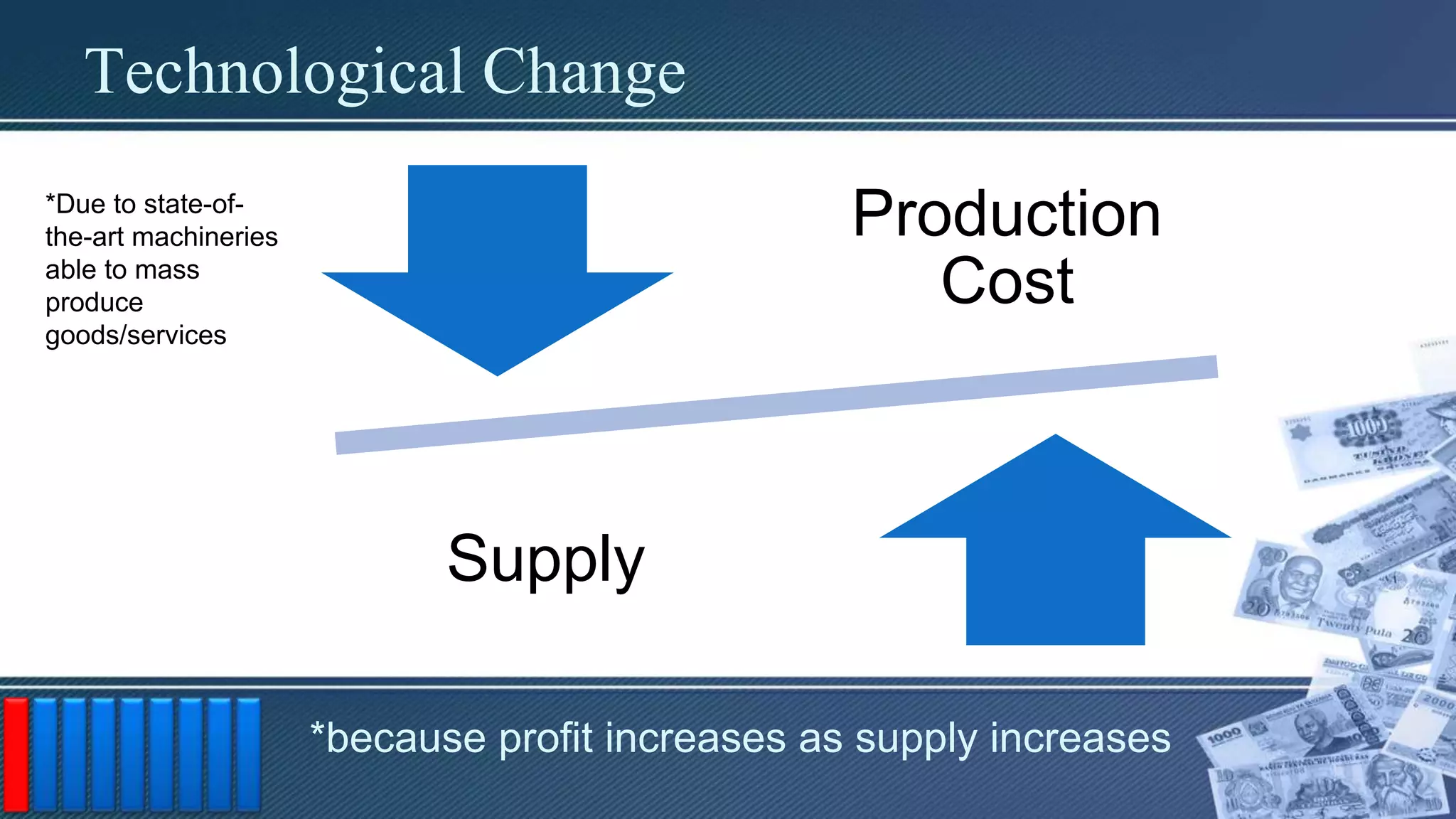

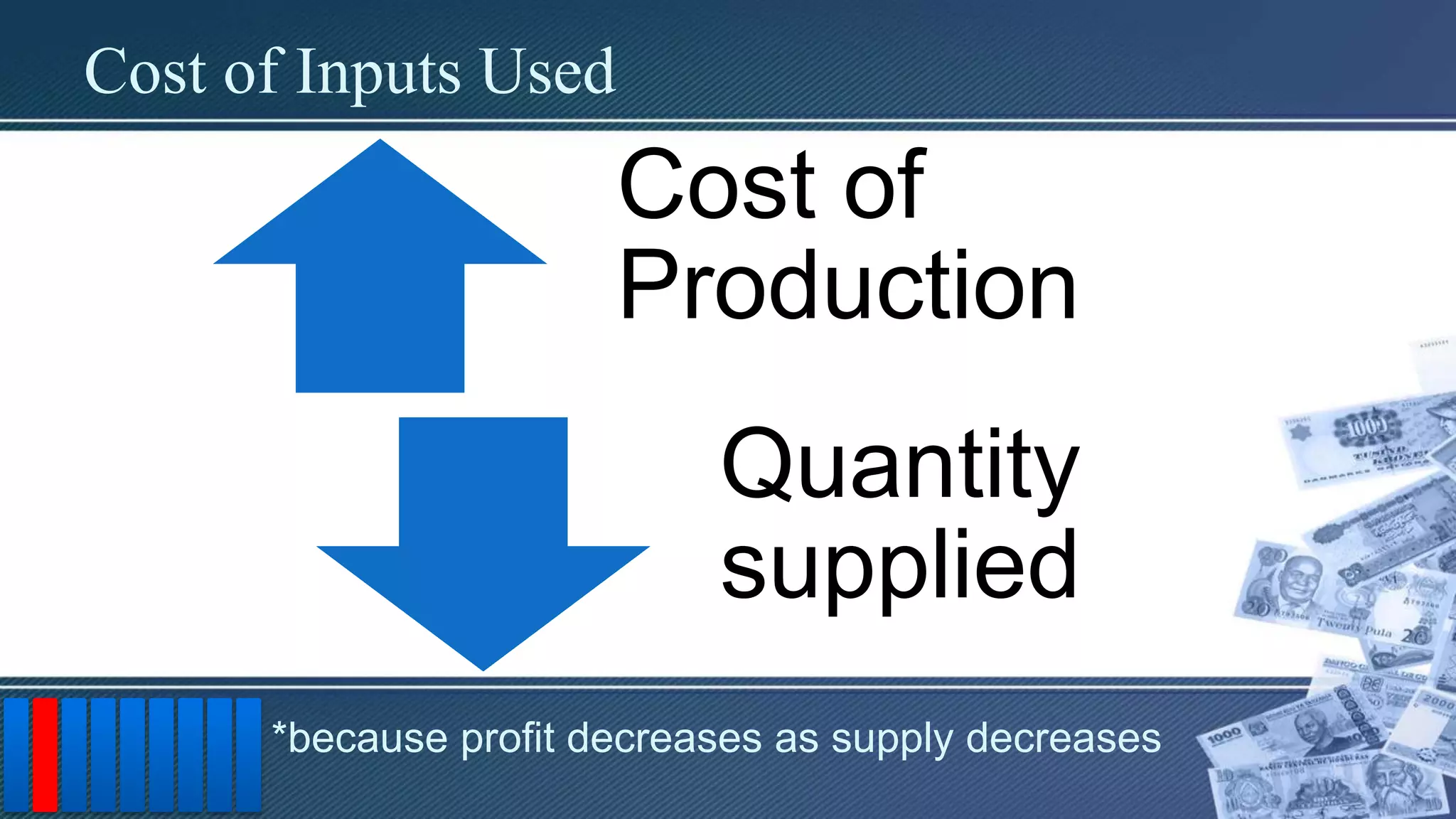

Cost of Production

•The costs of the production

process and the prices of inputs

that they have used to make the

product

Price of RelatedProducts

• Changes in the supply of goods have

significant effect in the supply of such goods.

47.

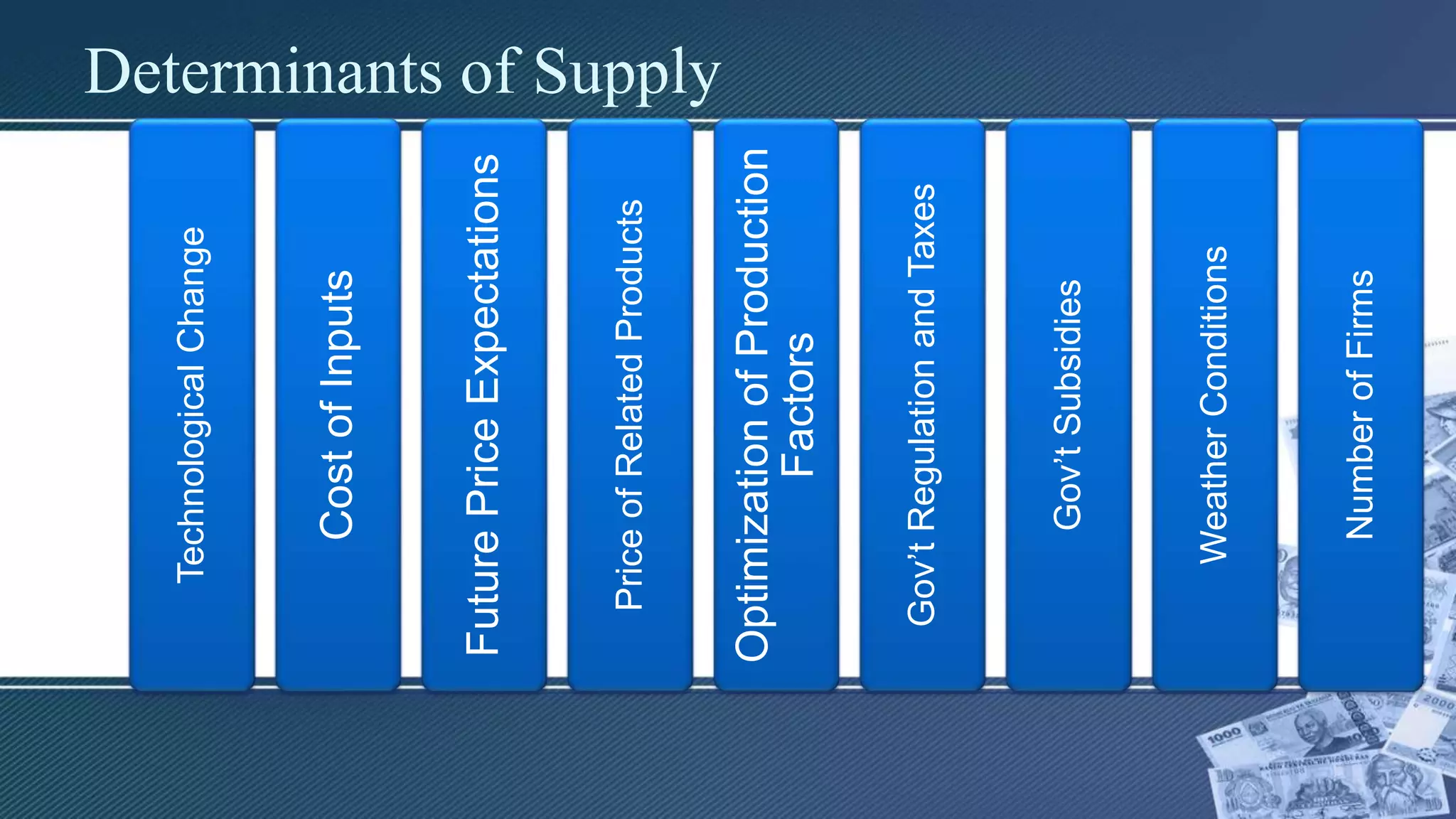

Optimization of ProductionFactors

• The process/methodology of making

something as fully perfect, functional, or

effective as possible.

• Efficient use of resources

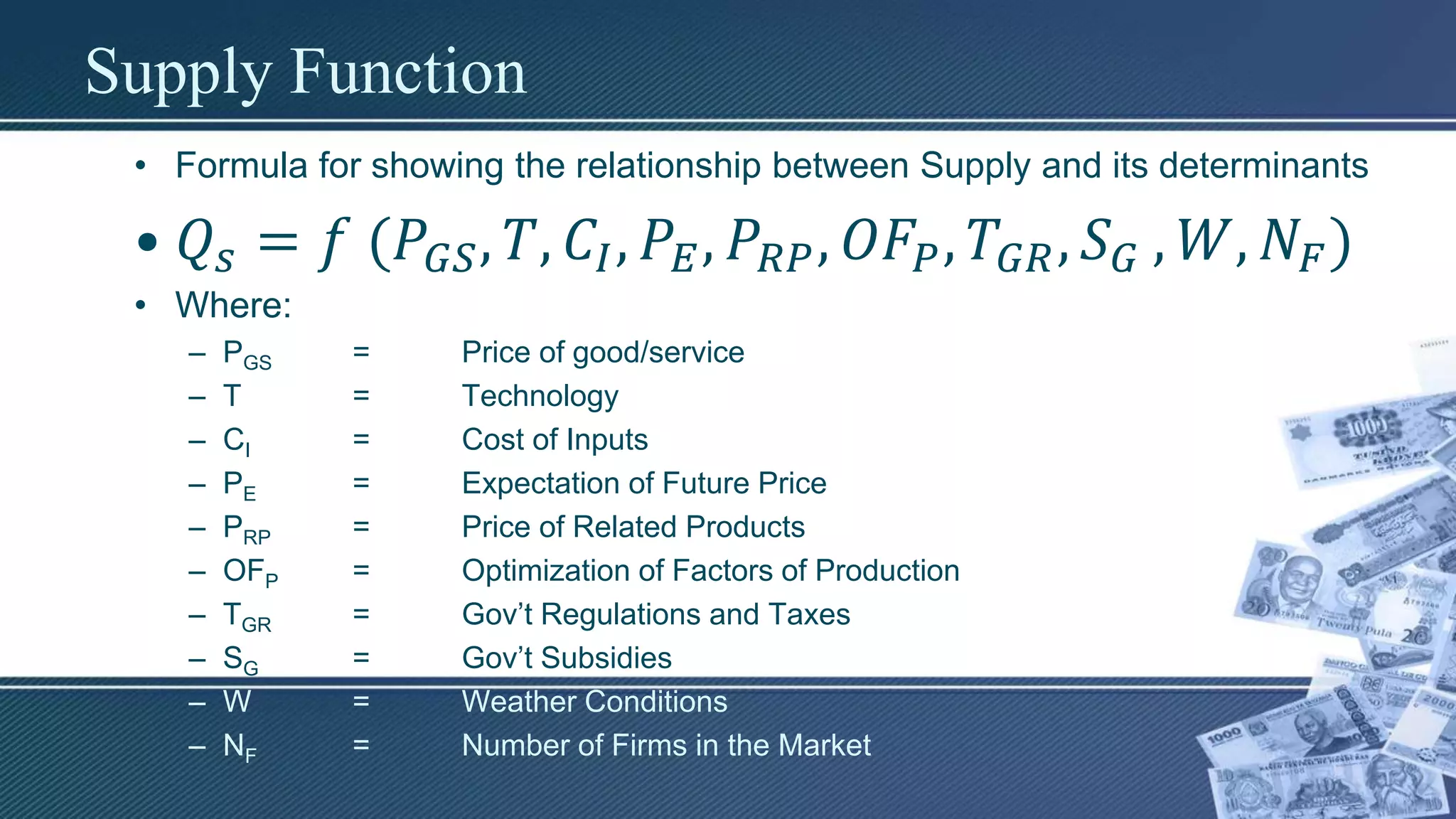

Supply Function

• Formulafor showing the relationship between Supply and its determinants

• 𝑄𝑠 = 𝑓 (𝑃𝐺𝑆, 𝑇, 𝐶𝐼, 𝑃𝐸, 𝑃𝑅𝑃, 𝑂𝐹𝑃, 𝑇𝐺𝑅, 𝑆 𝐺 , 𝑊, 𝑁𝐹)

• Where:

– PGS = Price of good/service

– T = Technology

– CI = Cost of Inputs

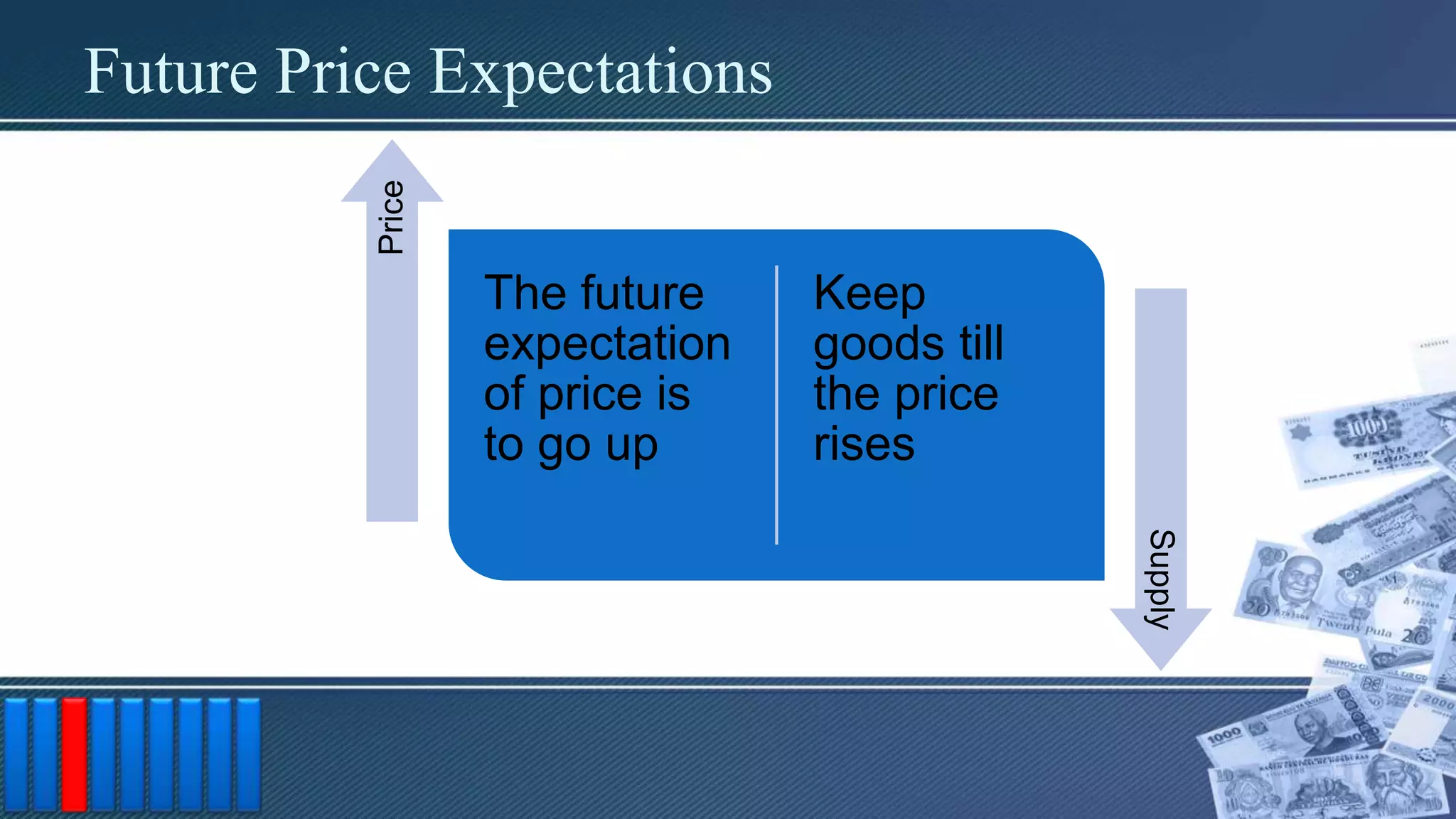

– PE = Expectation of Future Price

– PRP = Price of Related Products

– OFP = Optimization of Factors of Production

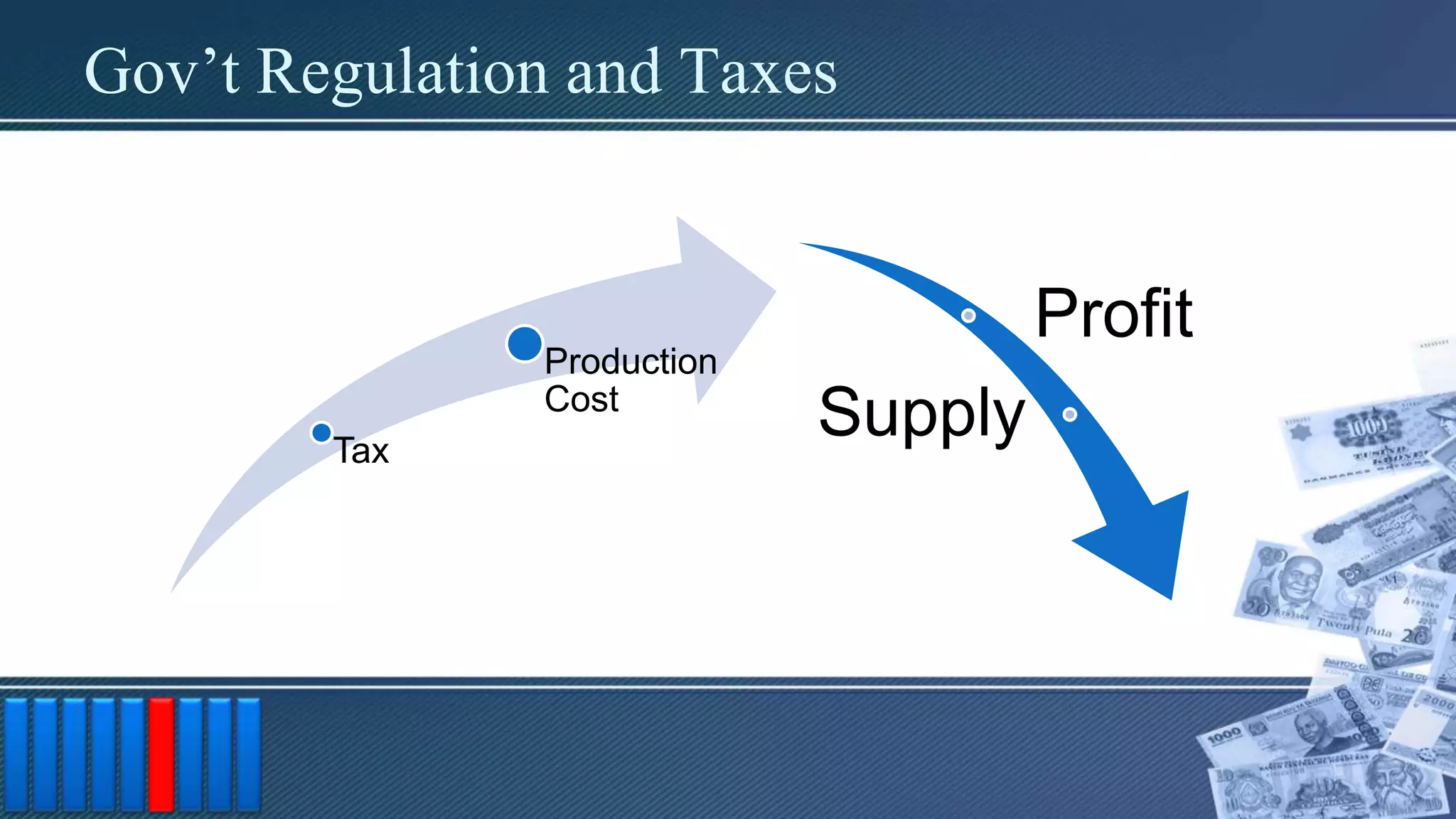

– TGR = Gov’t Regulations and Taxes

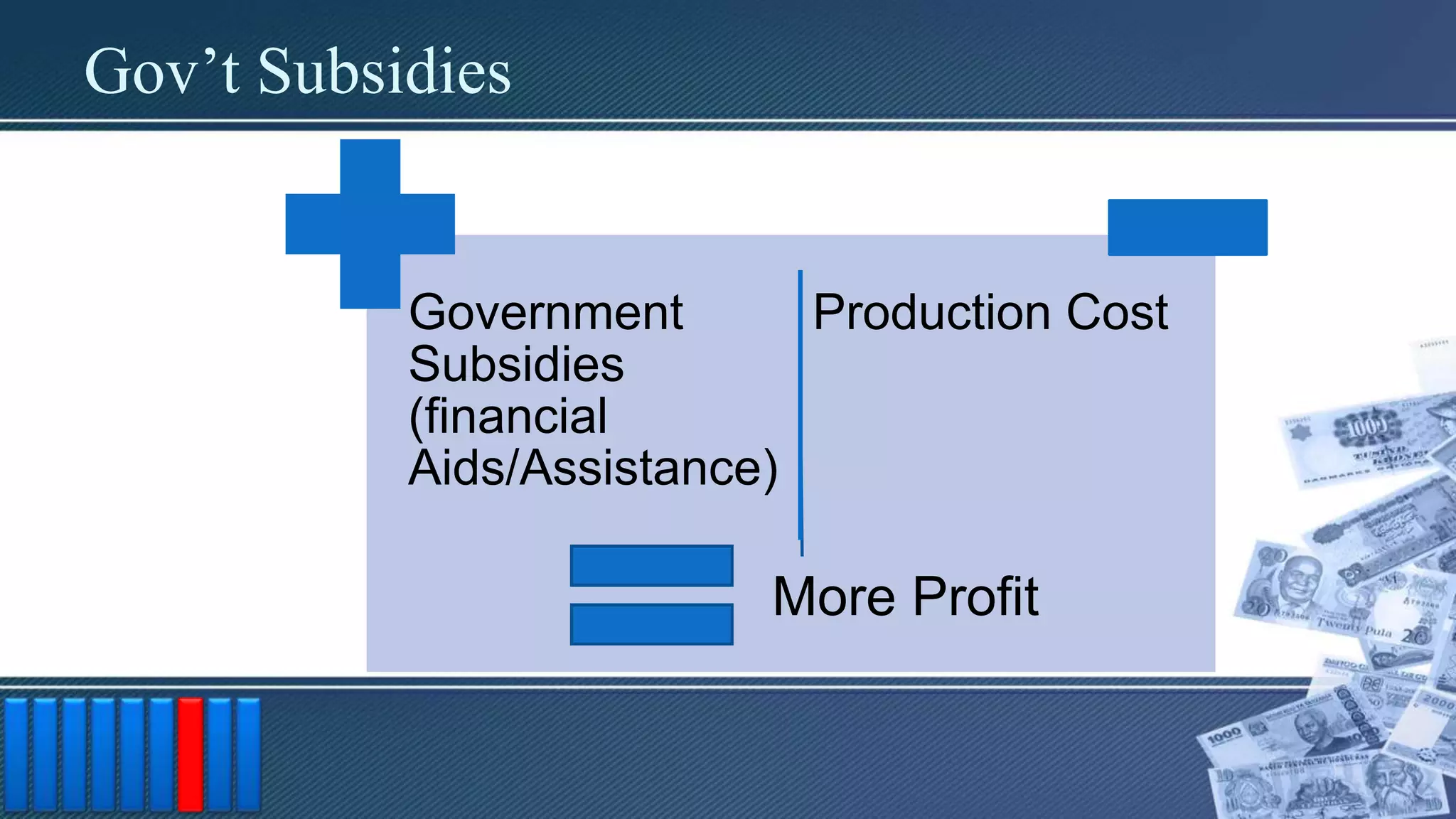

– SG = Gov’t Subsidies

– W = Weather Conditions

– NF = Number of Firms in the Market

54.

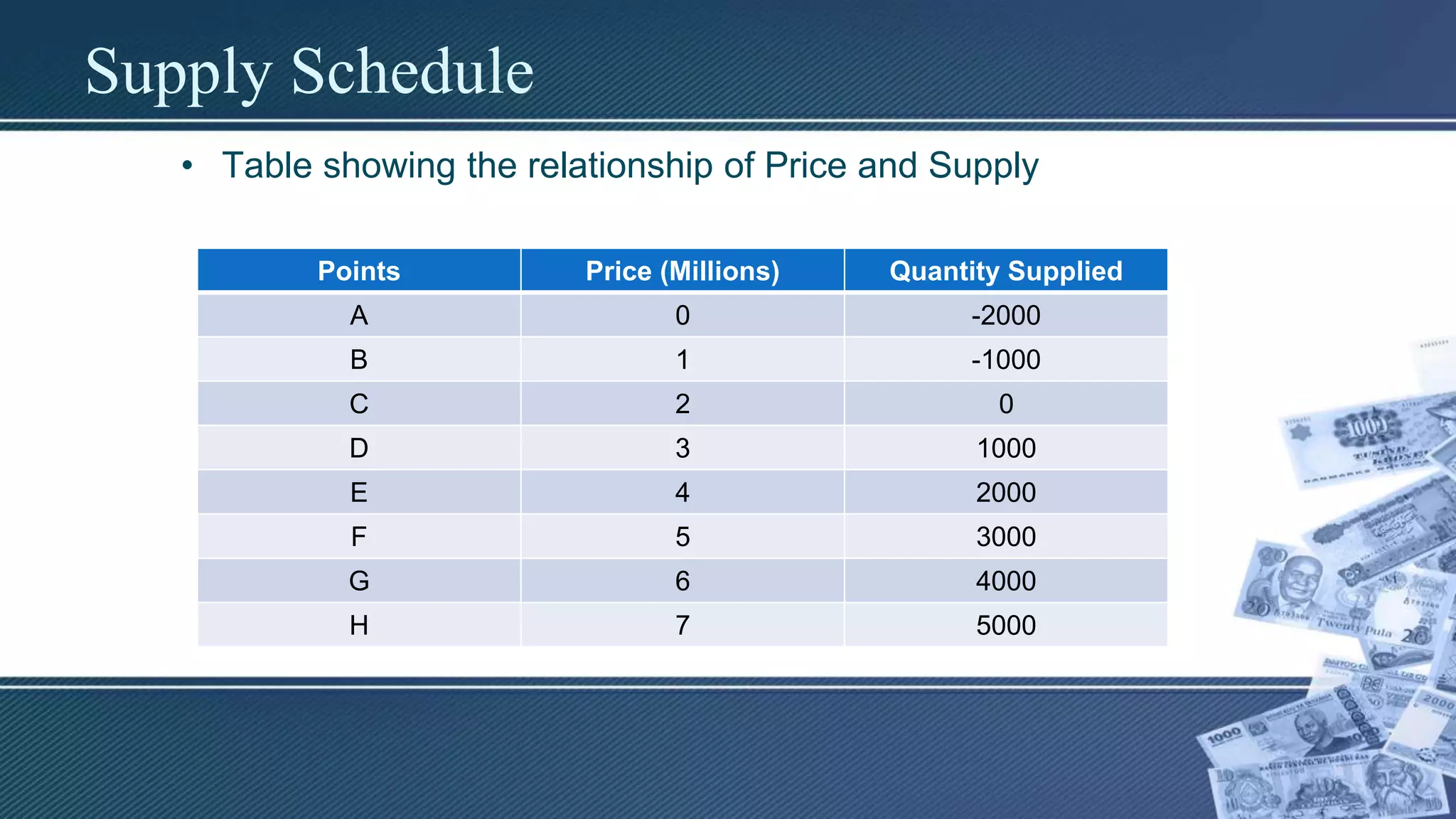

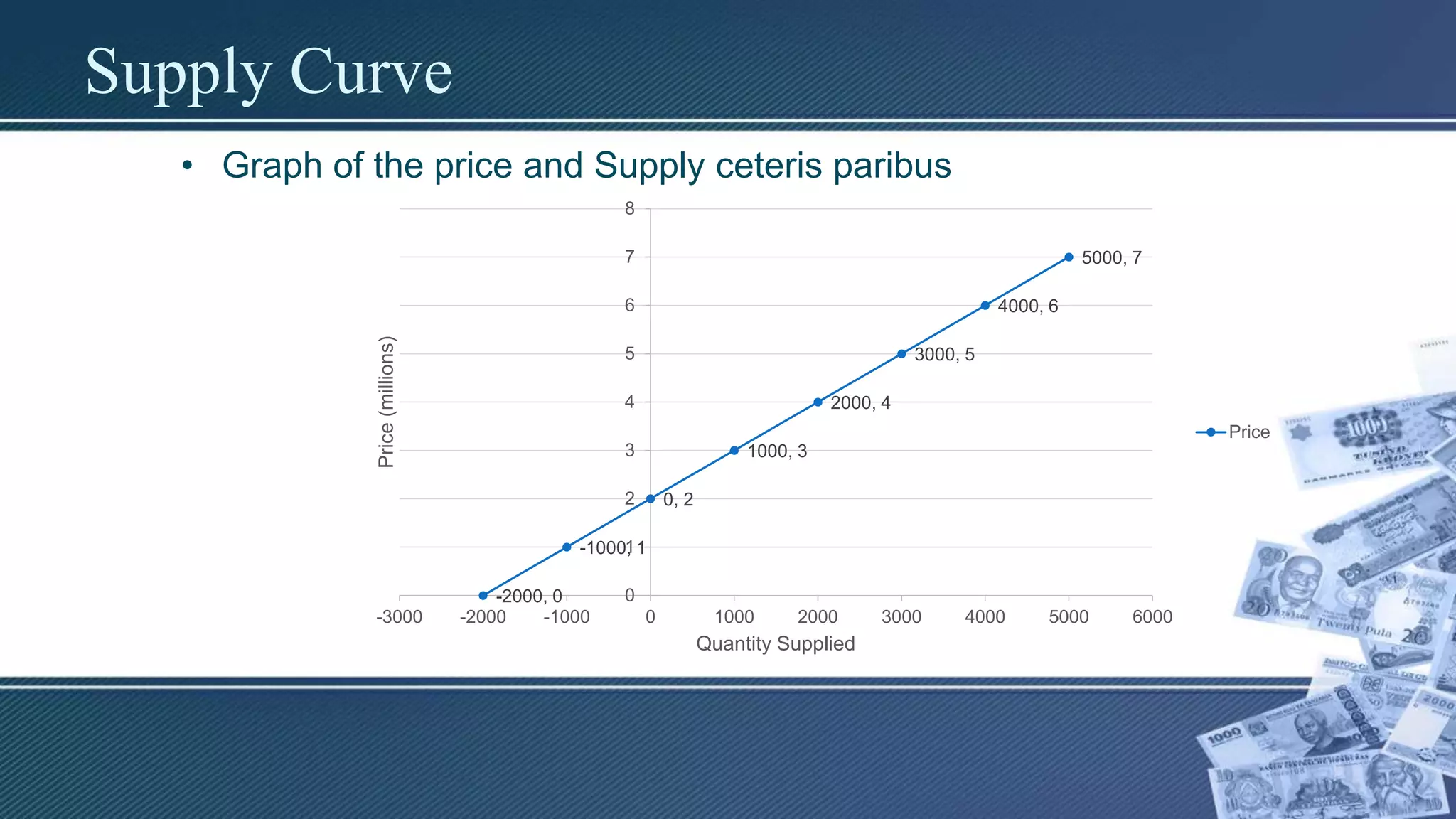

Supply Schedule

• Tableshowing the relationship of Price and Supply

Points Price (Millions) Quantity Supplied

A 0 -2000

B 1 -1000

C 2 0

D 3 1000

E 4 2000

F 5 3000

G 6 4000

H 7 5000

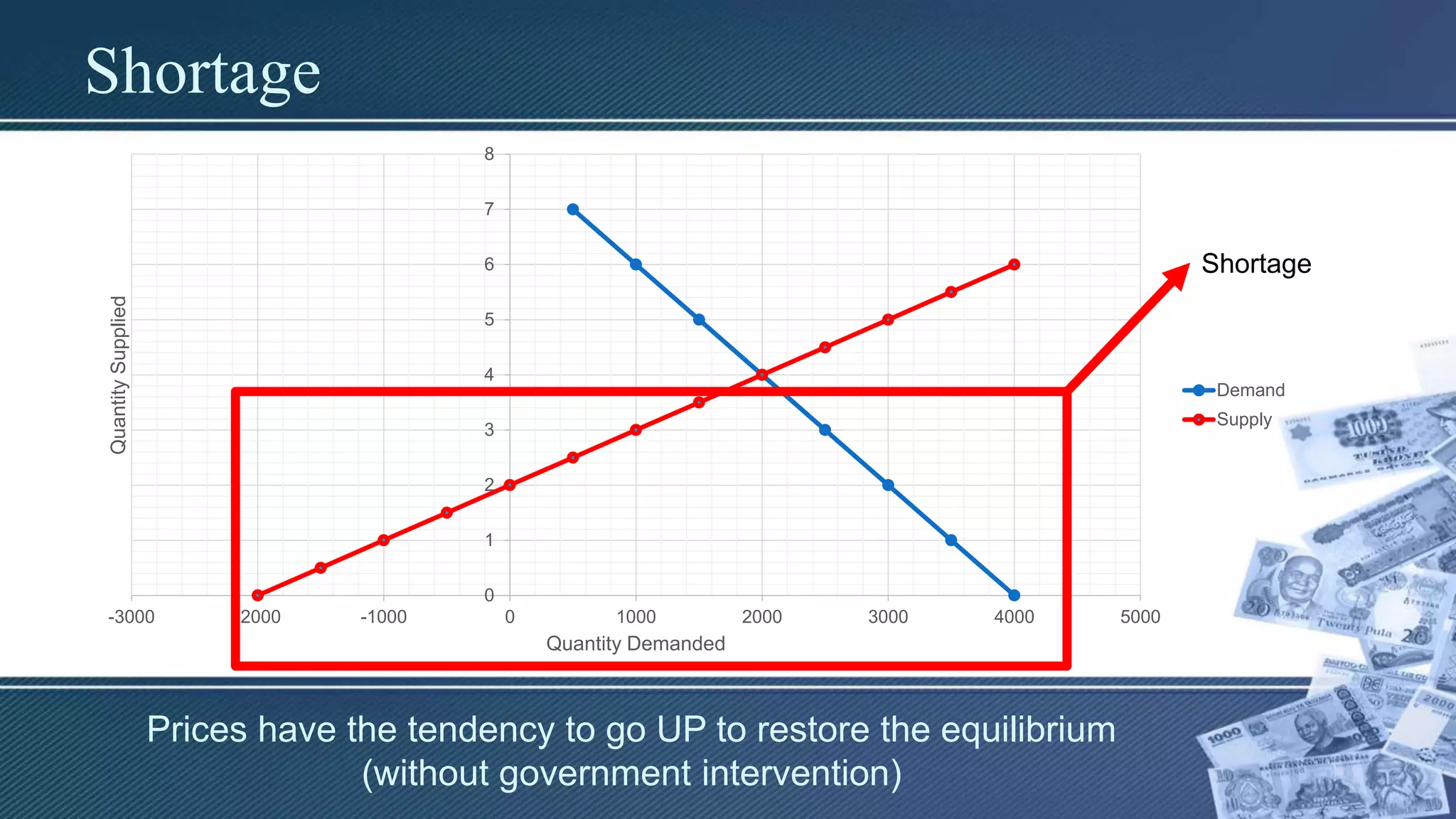

Shortage

0

1

2

3

4

5

6

7

8

-3000 -2000 -10000 1000 2000 3000 4000 5000

QuantitySupplied

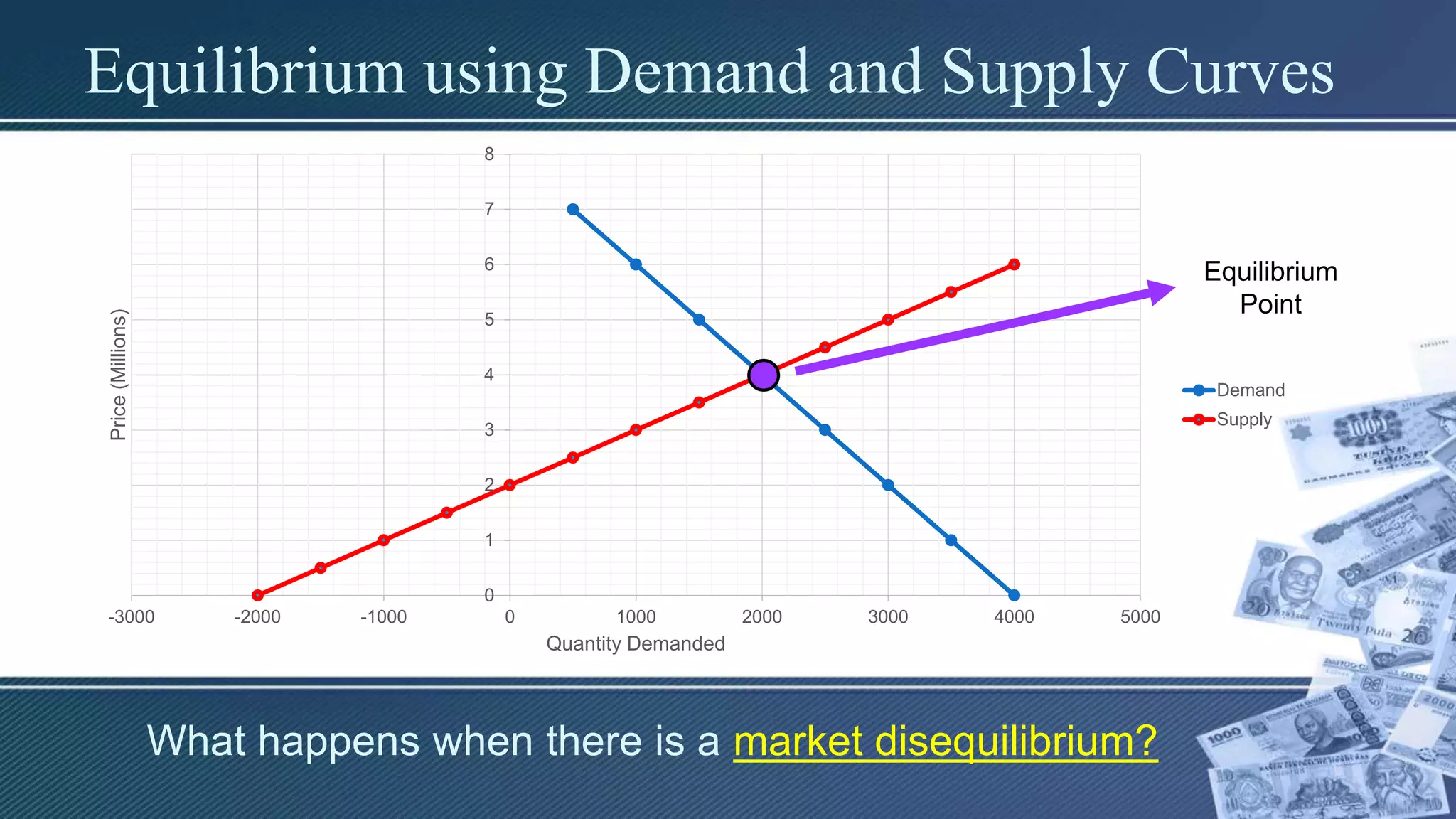

Quantity Demanded

Demand

Supply

Shortage

Prices have the tendency to go UP to restore the equilibrium

(without government intervention)

65.

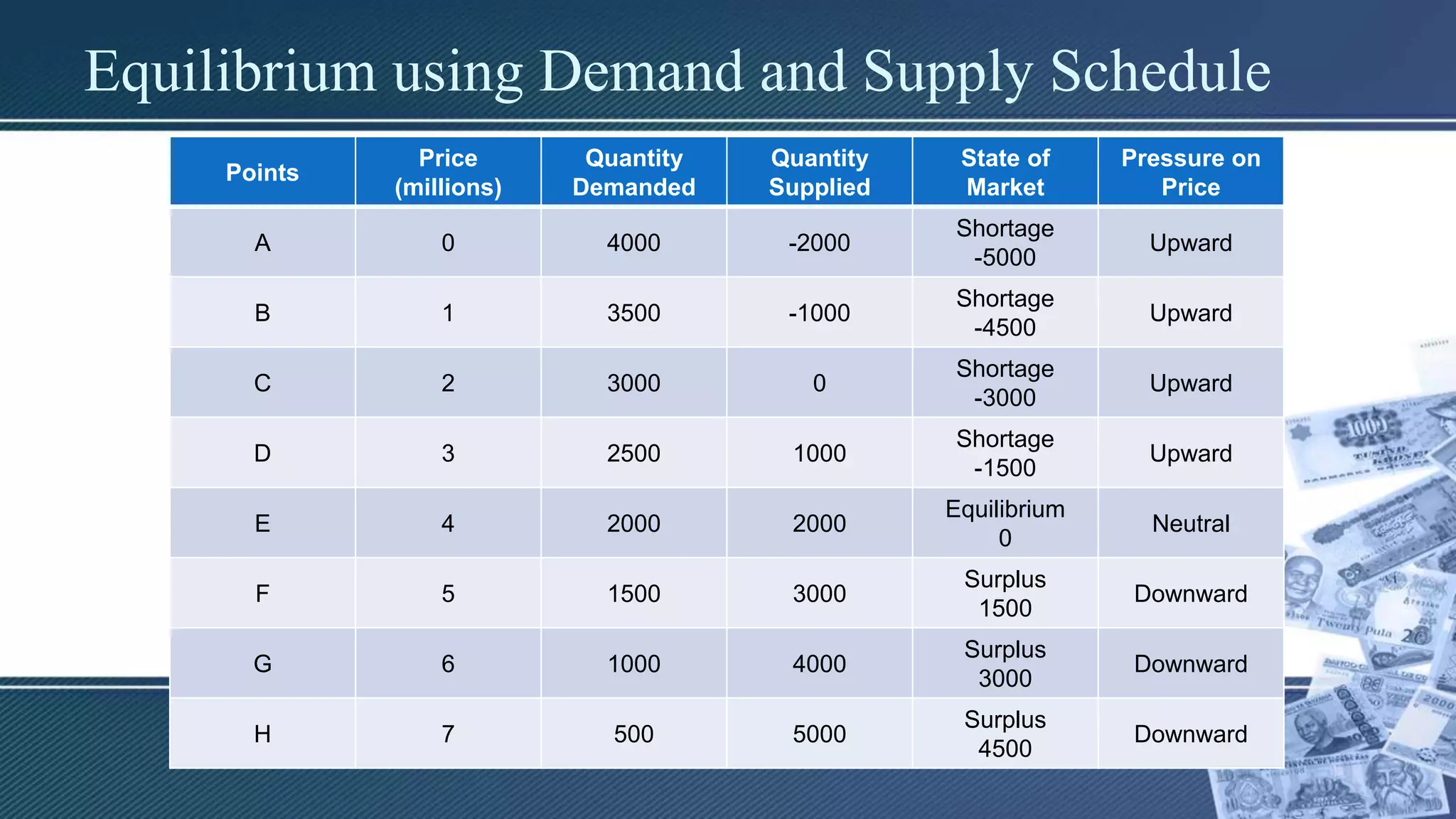

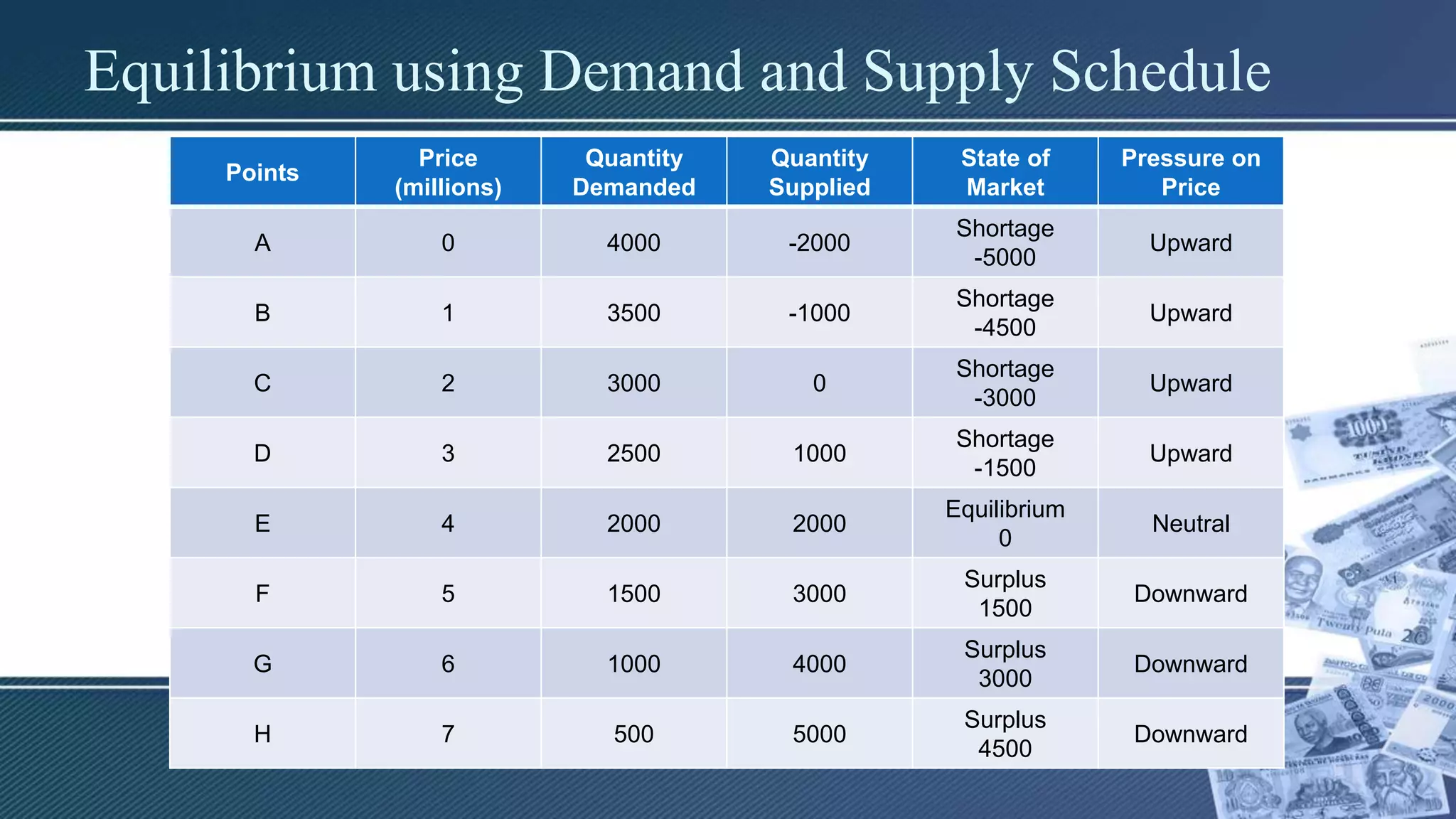

Equilibrium using Demandand Supply Schedule

Points

Price

(millions)

Quantity

Demanded

Quantity

Supplied

State of

Market

Pressure on

Price

A 0 4000 -2000

Shortage

-5000

Upward

B 1 3500 -1000

Shortage

-4500

Upward

C 2 3000 0

Shortage

-3000

Upward

D 3 2500 1000

Shortage

-1500

Upward

E 4 2000 2000

Equilibrium

0

Neutral

F 5 1500 3000

Surplus

1500

Downward

G 6 1000 4000

Surplus

3000

Downward

H 7 500 5000

Surplus

4500

Downward

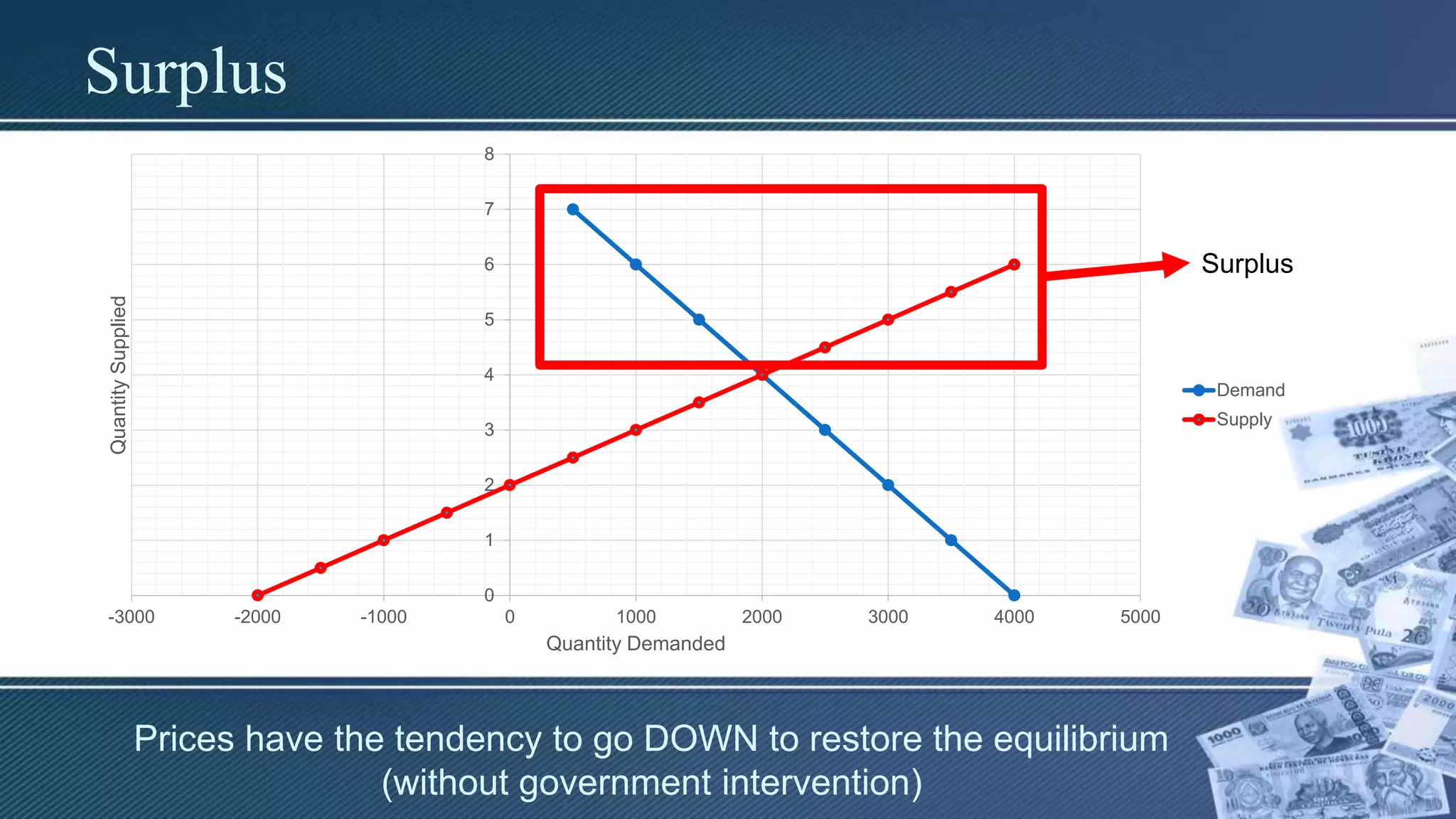

Surplus

0

1

2

3

4

5

6

7

8

-3000 -2000 -10000 1000 2000 3000 4000 5000

QuantitySupplied

Quantity Demanded

Demand

Supply

Surplus

Prices have the tendency to go DOWN to restore the equilibrium

(without government intervention)

69.

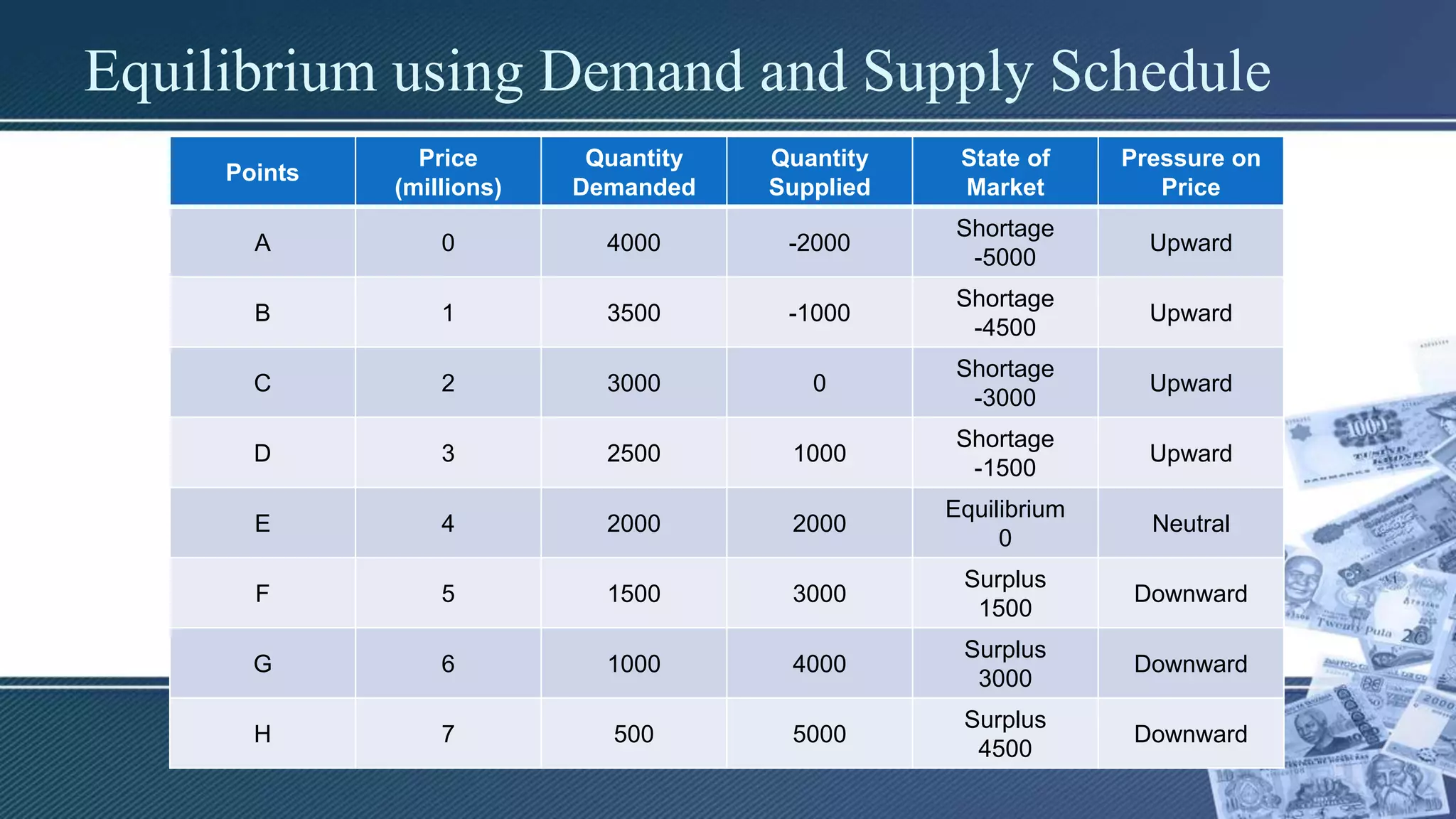

Equilibrium using Demandand Supply Schedule

Points

Price

(millions)

Quantity

Demanded

Quantity

Supplied

State of

Market

Pressure on

Price

A 0 4000 -2000

Shortage

-5000

Upward

B 1 3500 -1000

Shortage

-4500

Upward

C 2 3000 0

Shortage

-3000

Upward

D 3 2500 1000

Shortage

-1500

Upward

E 4 2000 2000

Equilibrium

0

Neutral

F 5 1500 3000

Surplus

1500

Downward

G 6 1000 4000

Surplus

3000

Downward

H 7 500 5000

Surplus

4500

Downward

Market Interference

• utilizedsupply and demand models are only

possible in an unregulated market

• In real world situations, governments around

the world try to control prices because:

–Some sectors do not benefit

–Some sectors take advantage of price controls

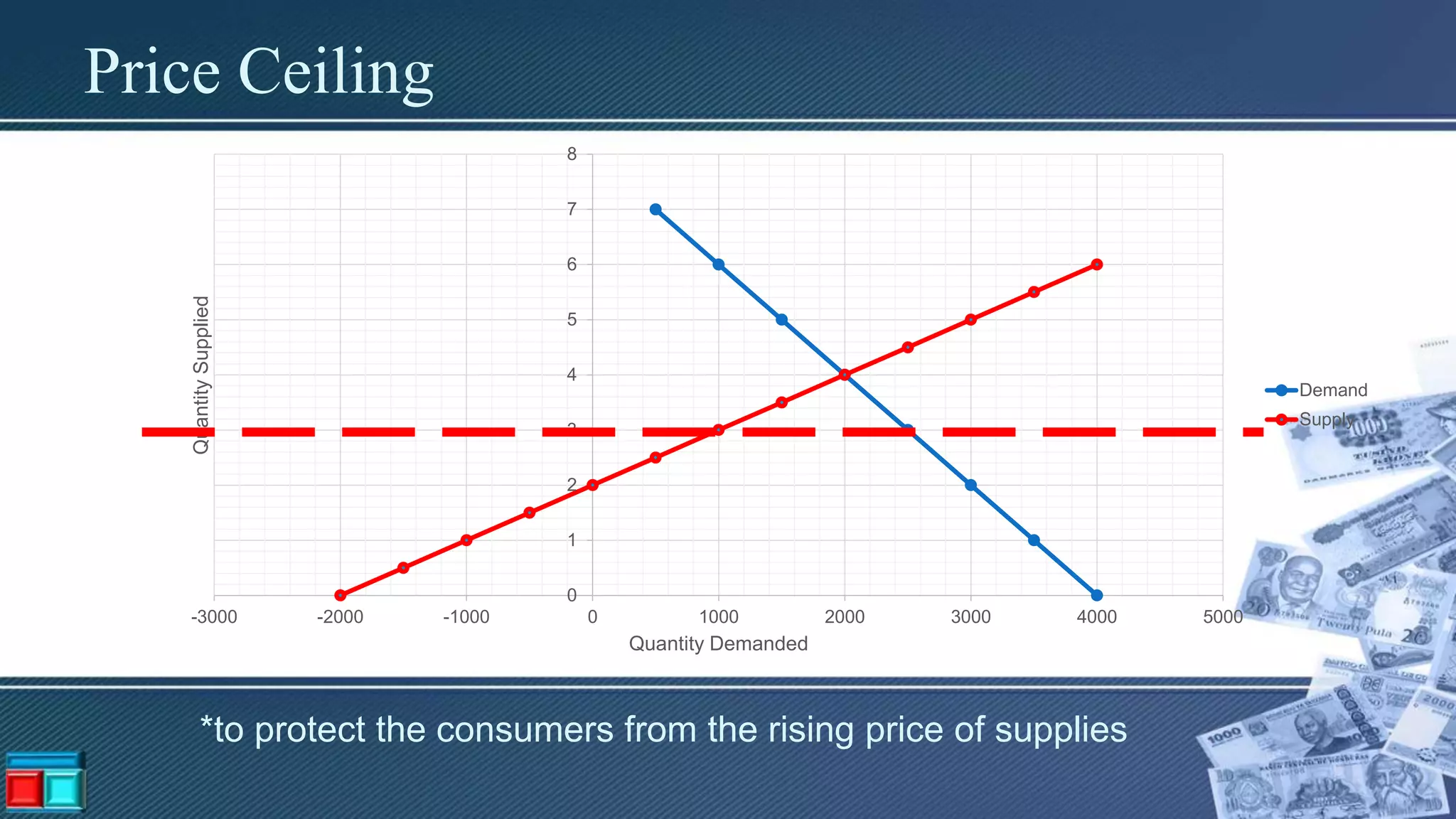

Price Ceiling

• Legalmaximum price imposed by the

government.

• Used only by the government if there is a

persistent SHORTAGE OF GOODS

75.

Price Ceiling

0

1

2

3

4

5

6

7

8

-3000 -2000-1000 0 1000 2000 3000 4000 5000

QuantitySupplied

Quantity Demanded

Demand

Supply

*to protect the consumers from the rising price of supplies

77.

Price Floor

• LegalMINIMUM PRICE imposed by the

government.

• Used only by the government if there is a

persistent SURPLUS OF GOODS

78.

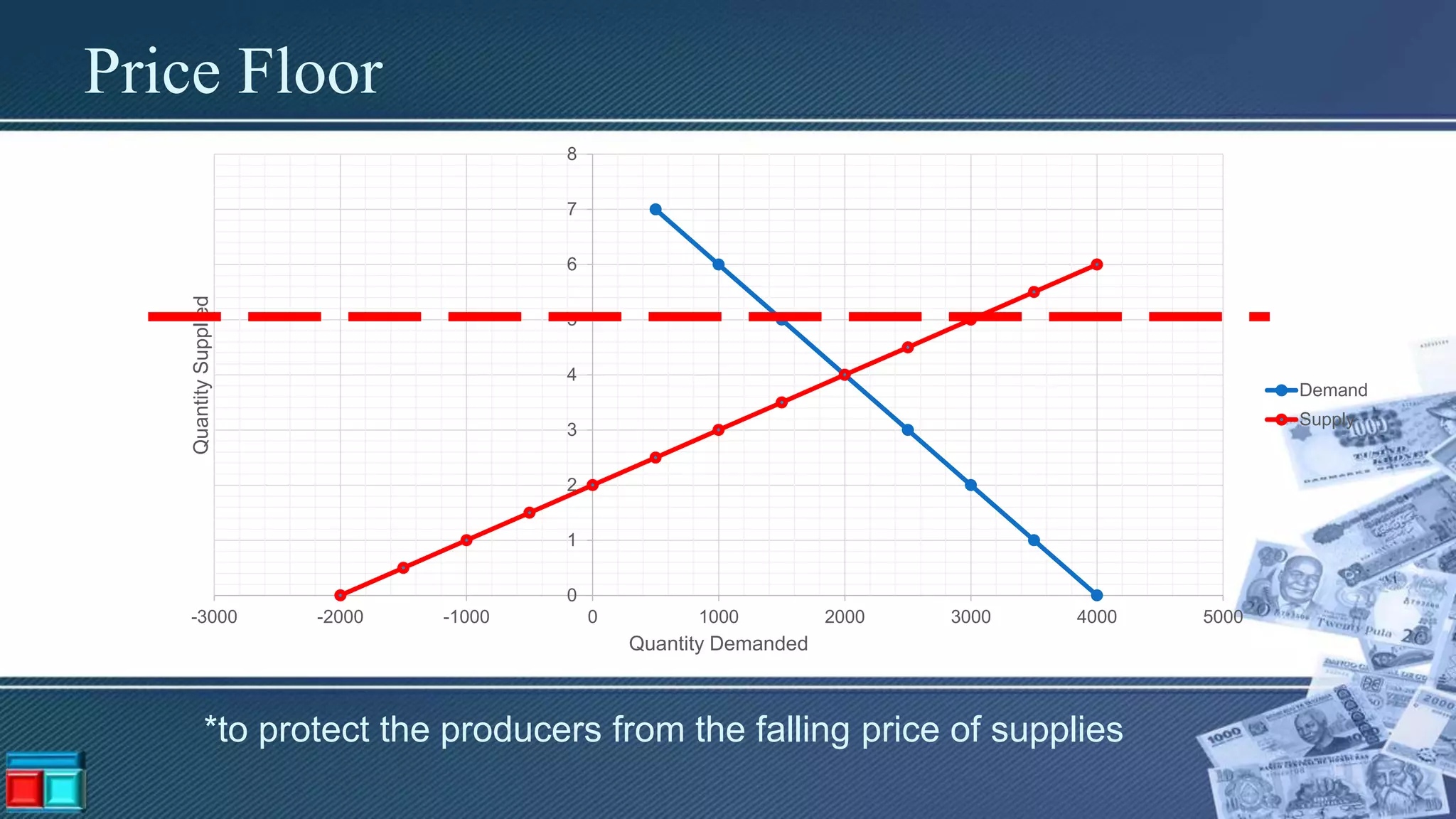

Price Floor

0

1

2

3

4

5

6

7

8

-3000 -2000-1000 0 1000 2000 3000 4000 5000

QuantitySupplied

Quantity Demanded

Demand

Supply

*to protect the producers from the falling price of supplies

79.

Humans and animalsare both selfish. They virtually don’t

care about others. They say clever things, make relationships

where both sides use each other, and look for a way to profit

themselves while limiting the loss for the other group.