Downloaded 272 times

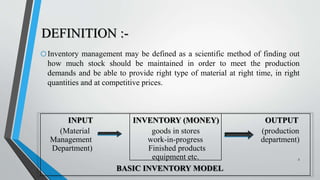

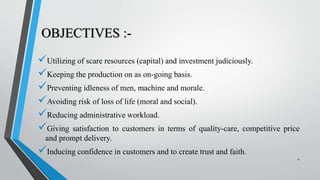

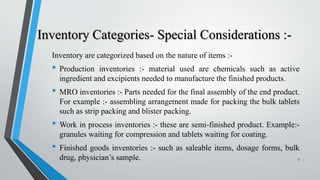

1) Inventory management involves maintaining optimal stock levels to meet production demands on time and at competitive prices. It aims to utilize resources efficiently while avoiding production interruptions. 2) Inventory is categorized based on the production stage - raw materials, work in process, finished goods. Special considerations are given to critical spare parts. 3) Factors like long lead times, seasonal demand, and material cost fluctuations influence inventory levels. Selective controls like A-B-C analysis prioritize high-value, critical items for close monitoring.