Downloaded 2,030 times

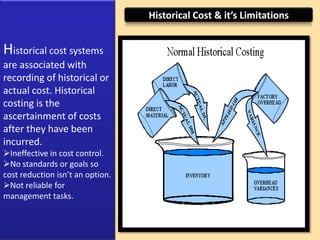

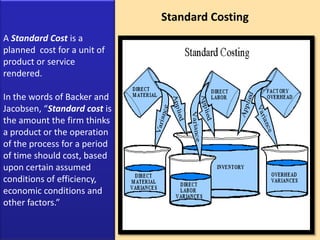

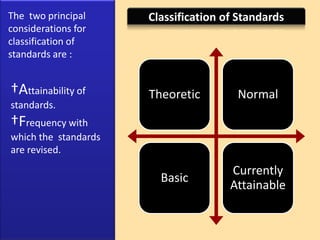

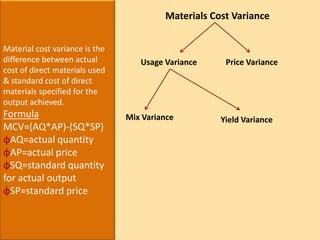

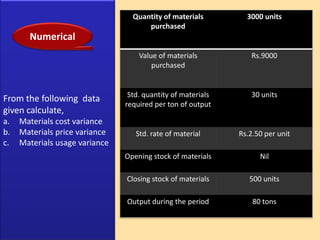

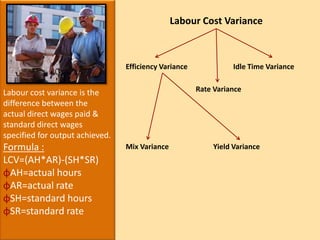

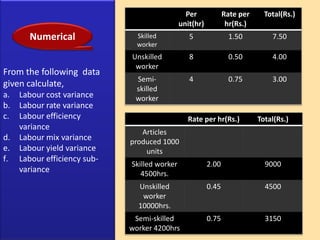

Standard costing involves setting standards for materials, labor, and overhead and comparing actual costs to the standards to calculate variances. It has several advantages as a management tool including cost control, finding inefficiencies, and measuring efficiency. Some limitations include difficulty setting standards for non-standard products and not considering all circumstances when setting standards. The document provides examples of calculating variances for materials, labor, and overhead costs based on standard and actual amounts. It also discusses classification of standards, revising standards, and advantages and limitations of standard costing.