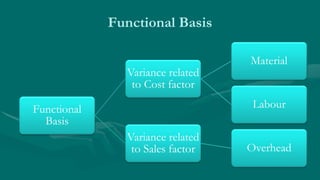

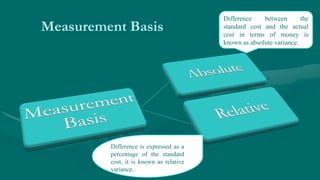

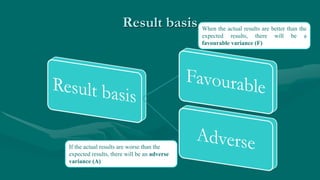

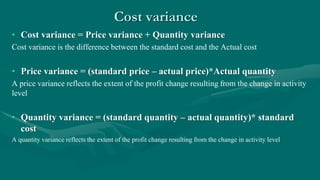

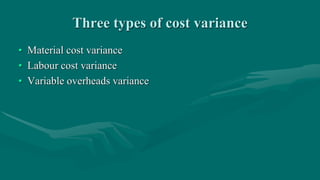

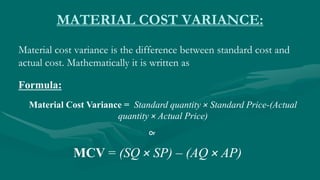

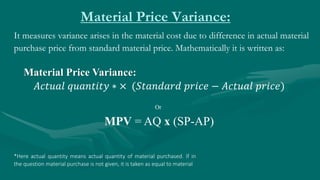

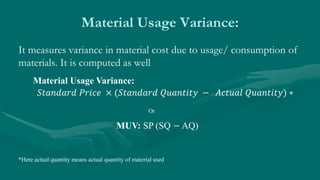

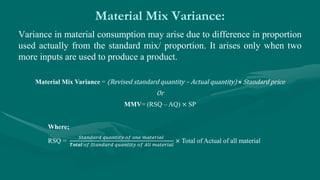

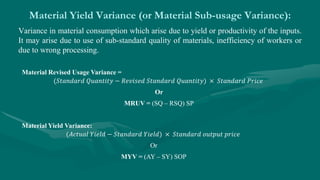

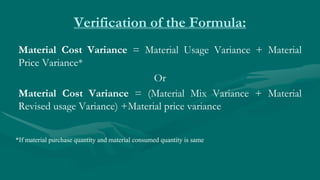

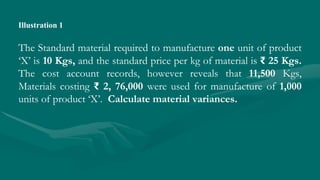

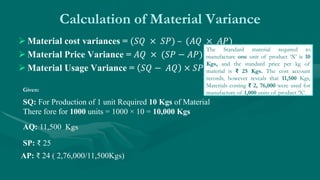

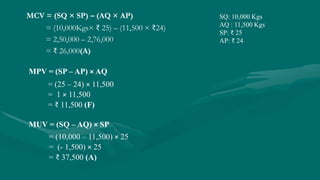

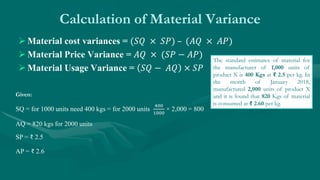

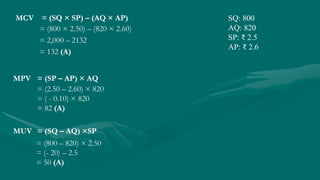

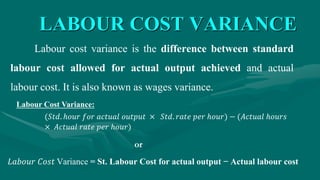

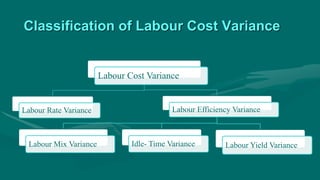

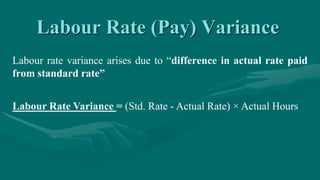

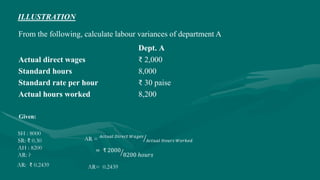

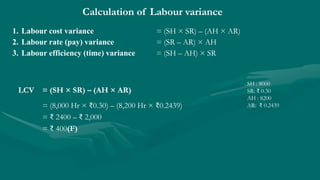

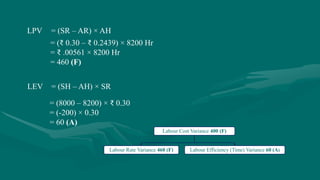

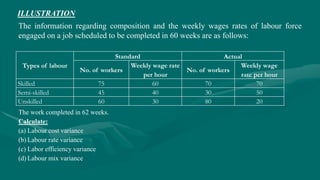

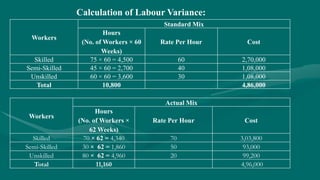

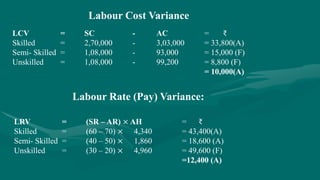

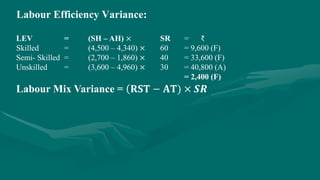

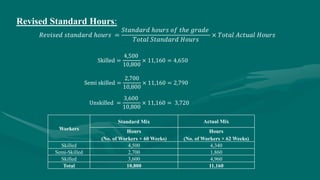

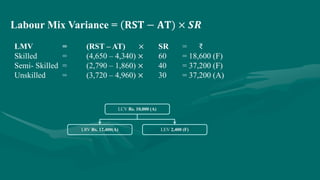

Standard costing is a technique used to measure differences between actual and expected costs. A variance is the difference between standards and actual performance. Material, labor, and overhead variances can be classified by function, measurement, or result. Material variances include price, usage, mix, and yield variances. Labor variances include rate, efficiency, idle time, mix, and yield variances. Variances are either favorable if actual is lower than standard or adverse if actual exceeds standard. Examples show how to calculate variances for a manufacturing company.