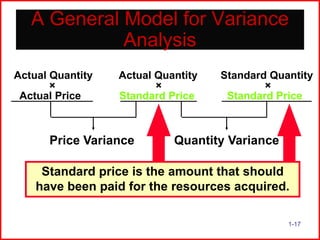

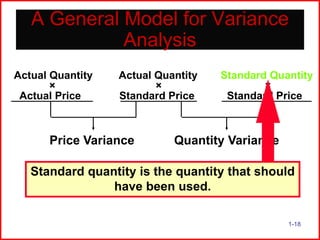

Downloaded 99 times

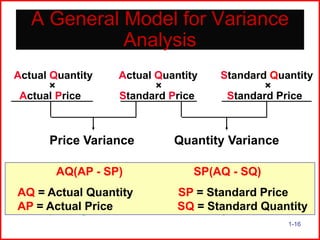

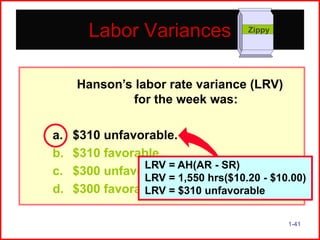

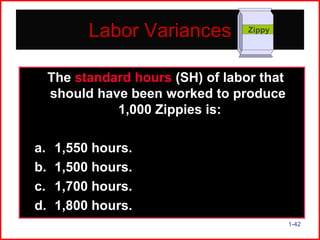

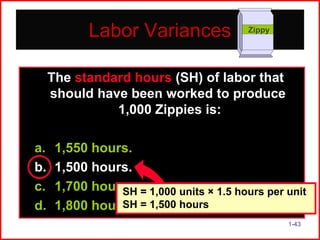

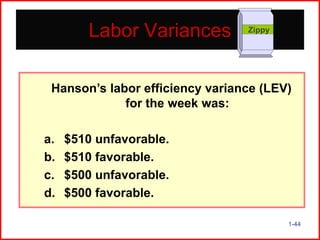

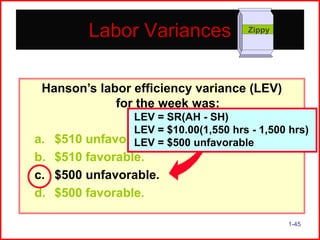

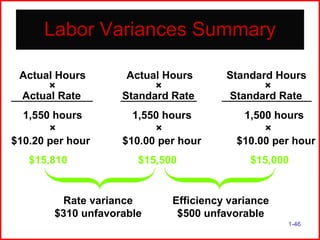

Here are the steps to calculate direct labor variances for Hanson Inc: 1. Standard hours to produce 1,000 Zippies = 1,000 x 1.5 = 1,500 hours 2. Standard direct labor cost = Standard hours x Standard rate = 1,500 hours x $10/hour = $15,000 3. Actual direct labor hours worked last week = 1,550 hours 4. Actual direct labor cost = Actual hours x Actual rate = Let's assume the actual rate is $10/hour = 1,550 hours x $10/hour = $15,500 5. Labor efficiency variance = Standard hours - Actual hours = 1,500 -