INDEX

Definition ofstandard

Steps in standard costing

Types of standards

Variance

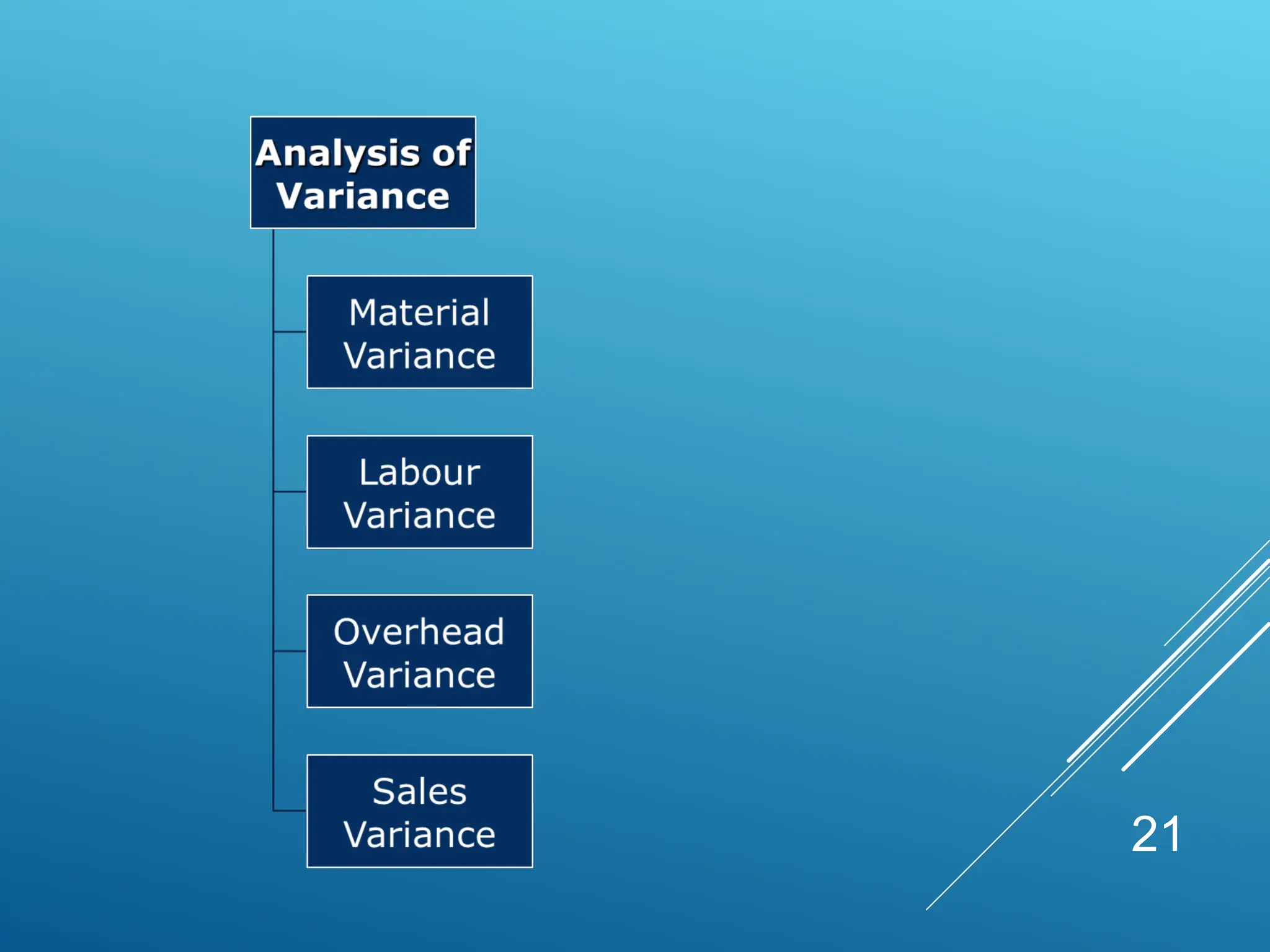

Types of variance

Variance Analysis

Advantages & disadvantages of Std costing

2

3.

3

STANDARD

It’s a normor bench mark

It is useful for comparison

it may indicate minimum quality

Eg. Standard of passing

4.

4

STANDARD COST

An estimatedor pre-determined

cost of performing an operation

or producing a good or service,

under normal conditions.

It is used as a basis for cost

control through variance

analysis.

5.

5

It ischosen to serve as a

benchmark in the standard

costing/ budgetary control

system.

It is a budget for the production

of one unit of product or service.

Standard Cost

6.

6

STANDARD COST

Itis a pre-determined cost which is

calculated from management’s standards

of efficient operation and the relevant

necessary expenditure.

It is a cost accounting technique for

cost control where standard costs are

determined and compared with

actual costs, to initiate corrective action.

7.

7

STANDARD COSTING

It isa control method involving

the preparation of detailed cost

and sales budgets.

A management tool used to

facilitate management by

exception.

STEPS IN STANDARD

COSTING

Setthe standard cost

A standard quantity is predetermined

and standard price per unit is

estimated.

Budgeted cost is calculated by using

standard cost.

9

10.

STEPS IN STANDARDCOSTING

• Record the actual cost

Calculate actual quantity and

cost incurred giving full details.

10

11.

STEPS IN STANDARDCOSTING

Variance Analysis

Comparison of the actual cost with the

budgeted cost.

The cost variance is used in controlling cost.

Create effective control system.

Resetting the budget, if required.

11

12.

TYPES OF STANDARDS

IdealStandards:

These represents the level of performance attainable

when prices for material and labour are most

favorable, when the highest output is achieved with

the best equipment and layout and when maximum

efficiency in utilization of resources results in

maximum output with minimum cost.

12

13.

Normal Standards:

These arethe standards that may be achieved

under normal operating conditions. The normal

activity has been defined as number of standard

hours which will produce normal efficiency

sufficient goods to meet the average sales

demand over a term of years.

13

14.

Basic orBogey standards:

When basic standards are in use, variances are not

calculated as the difference between standard and

actual cost. Instead, the actual cost is expressed

as a percentage of basic cost.

Does not consider the variable costs

14

15.

Current Standard:

Thesestandards reflect the management’s anticipation of

what actual cost will be for the current period. These

are the costs which the business will incur if the

anticipated prices are paid for goods and services and

the usage corresponds to that believed to be necessary

to produce the planned output.

15

16.

VARIANCE

The differencebetween standard cost and actual cost of the

actual output is defined as Variance. A variance may be

favorable or unfavorable.

If the actual cost is less than the standard cost, the

variance is favorable and if the actual cost is more than the

standard cost, the variance will be unfavorable.

It is not enough to know the figures of these variances in

fact it is required to trace their origin and causes of

occurrence for taking necessary remedial steps to reduce /

eliminate them.

16

17.

17

Variance - Types

Thepurpose of standard costing reports is

to investigate the reasons for significant

variances so as to identify the problems

and take corrective action. Variances are

broadly of two types, namely, controllable

and uncontrollable.

18.

VARIANCE ANALYSIS

Variance analysisis the dividing

of the cost variance into its

components to know their

causes, so that one can approach

for corrective measures.

18

19.

VARIANCE ANALYSIS

Variances ofEfficiency:

Variance arising due to the effectiveness in

use of material quantities, labour hours.

Here actual quantities are compared with

predetermined standards.

19

20.

Variances of PriceRates:

Variances arising due to change in unit material prices, standard

labour hour rates and standard allowances for indirect costs. Here

actual prices are compared with predetermined ones.

Variances of Due to Volume:

Variance due to effect of difference between actual activity and the

level of activity estimated when the standard was set.

20

REASONS OF

MATERIAL VARIANCE

Changein Basic price

Fail to purchase anticipated standard

quantities at appropriate price

Use of sub-standard material

Ineffective use of materials

Pilferage

22

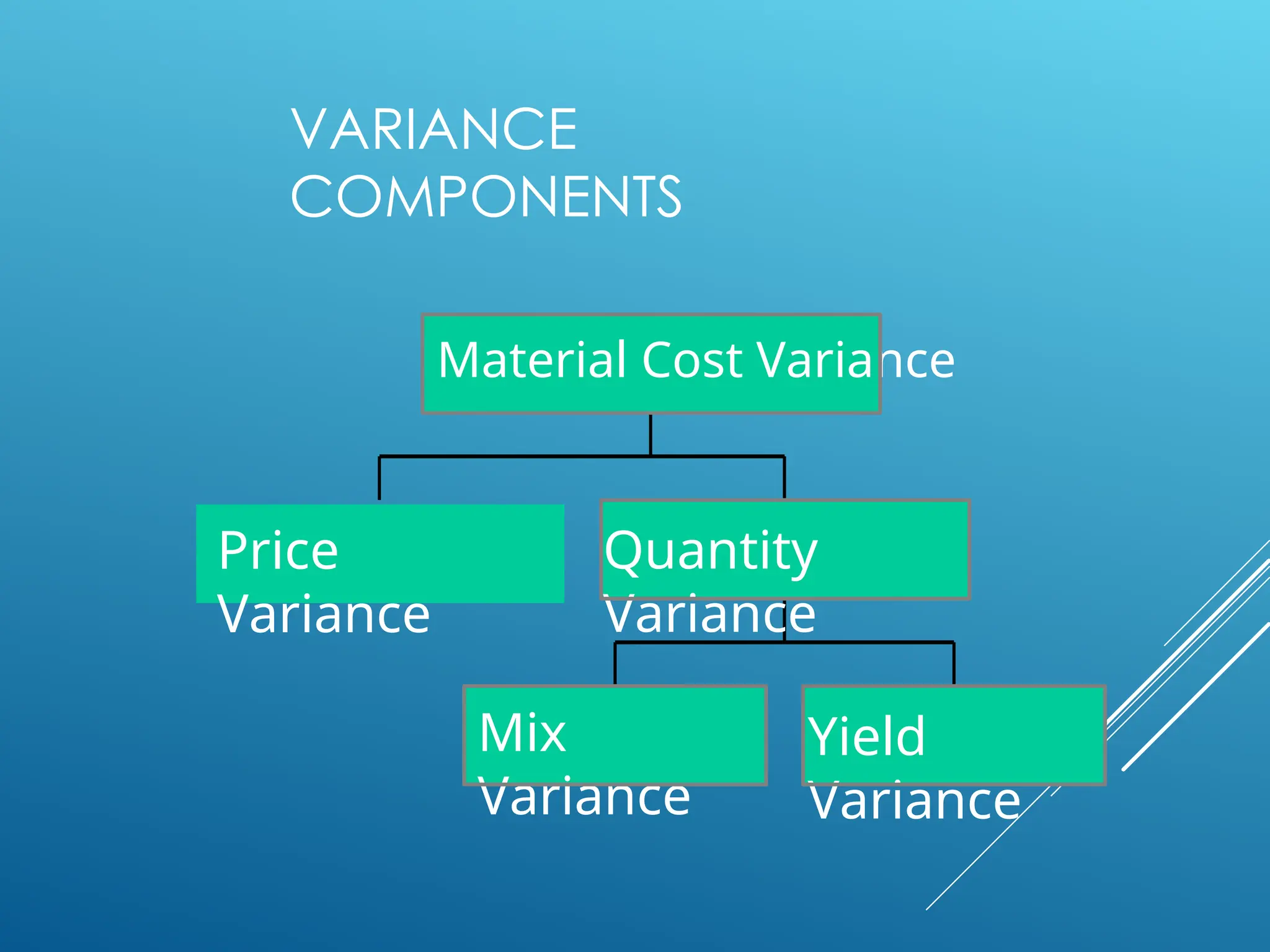

MATERIAL VARIANCE

Material CostVariance

Material Price Variance

Material Usage Variance

Can we sub-divide Usage Variance ?

What are its causes, when we have more

than one Raw Material ?

24

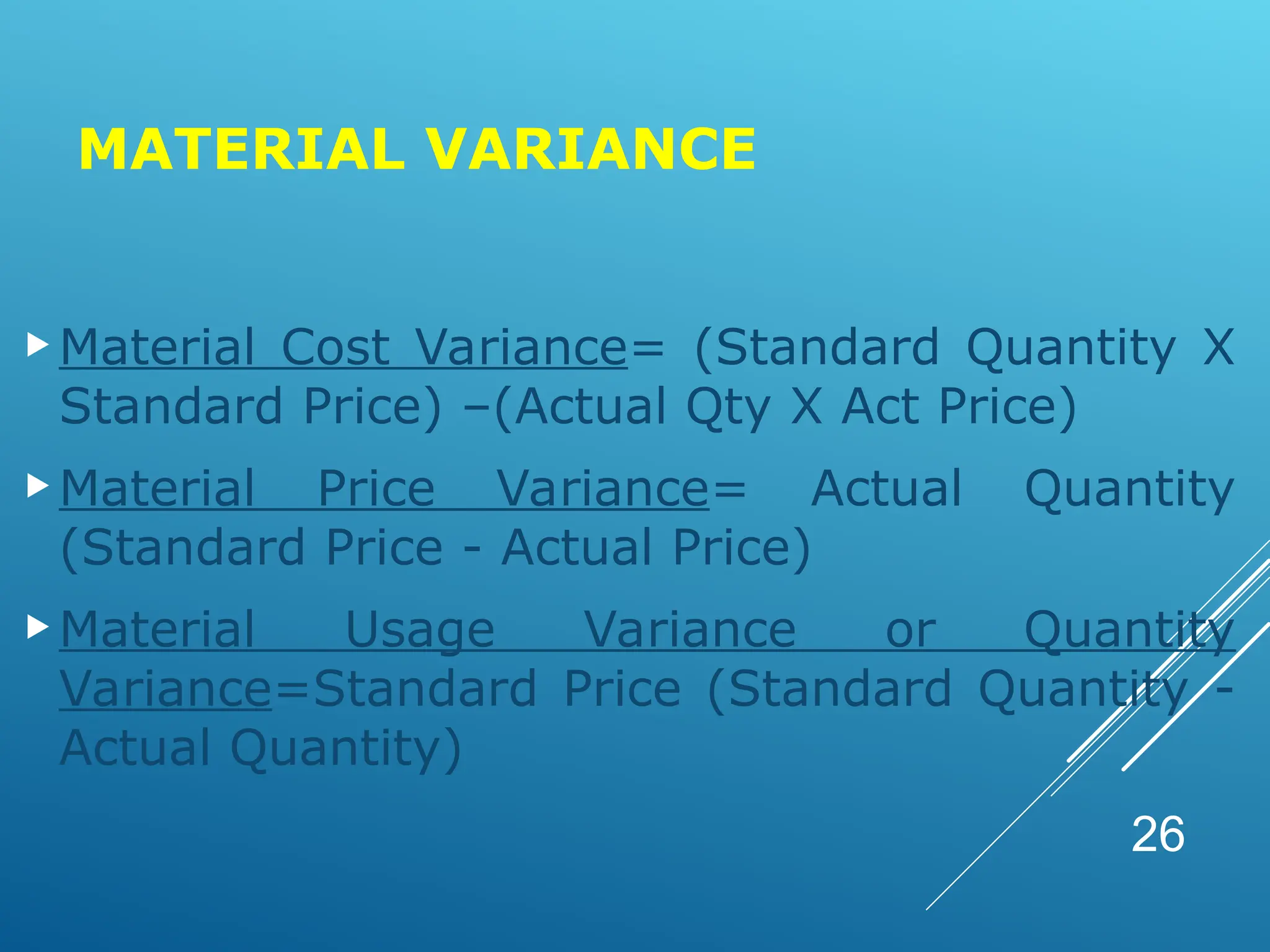

MATERIAL VARIANCE

Material CostVariance= (Standard Quantity X

Standard Price) –(Actual Qty X Act Price)

Material Price Variance= Actual Quantity

(Standard Price - Actual Price)

Material Usage Variance or Quantity

Variance=Standard Price (Standard Quantity -

Actual Quantity)

26

27.

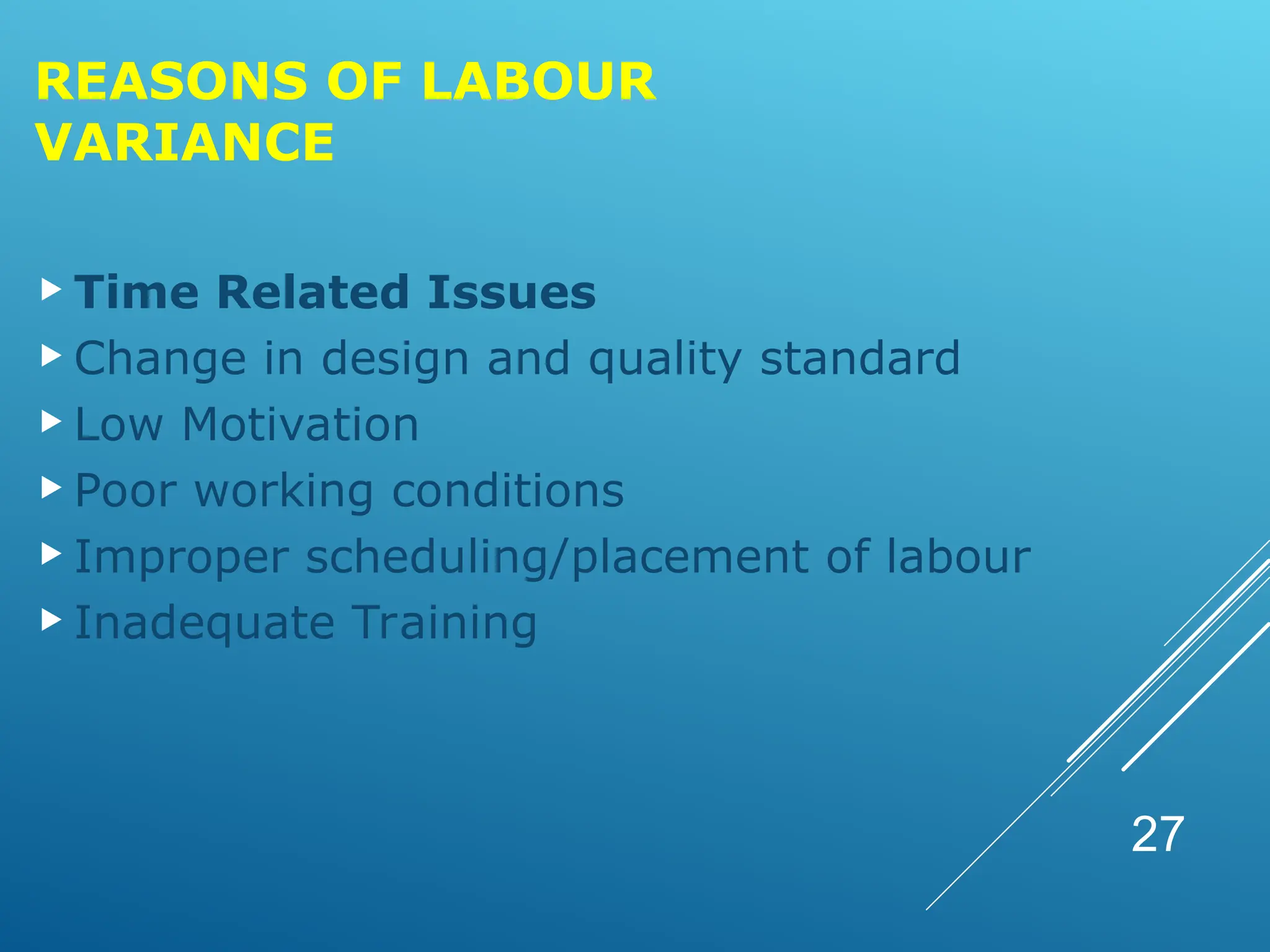

REASONS OF LABOUR

VARIANCE

Time Related Issues

Change in design and quality standard

Low Motivation

Poor working conditions

Improper scheduling/placement of labour

Inadequate Training

27

28.

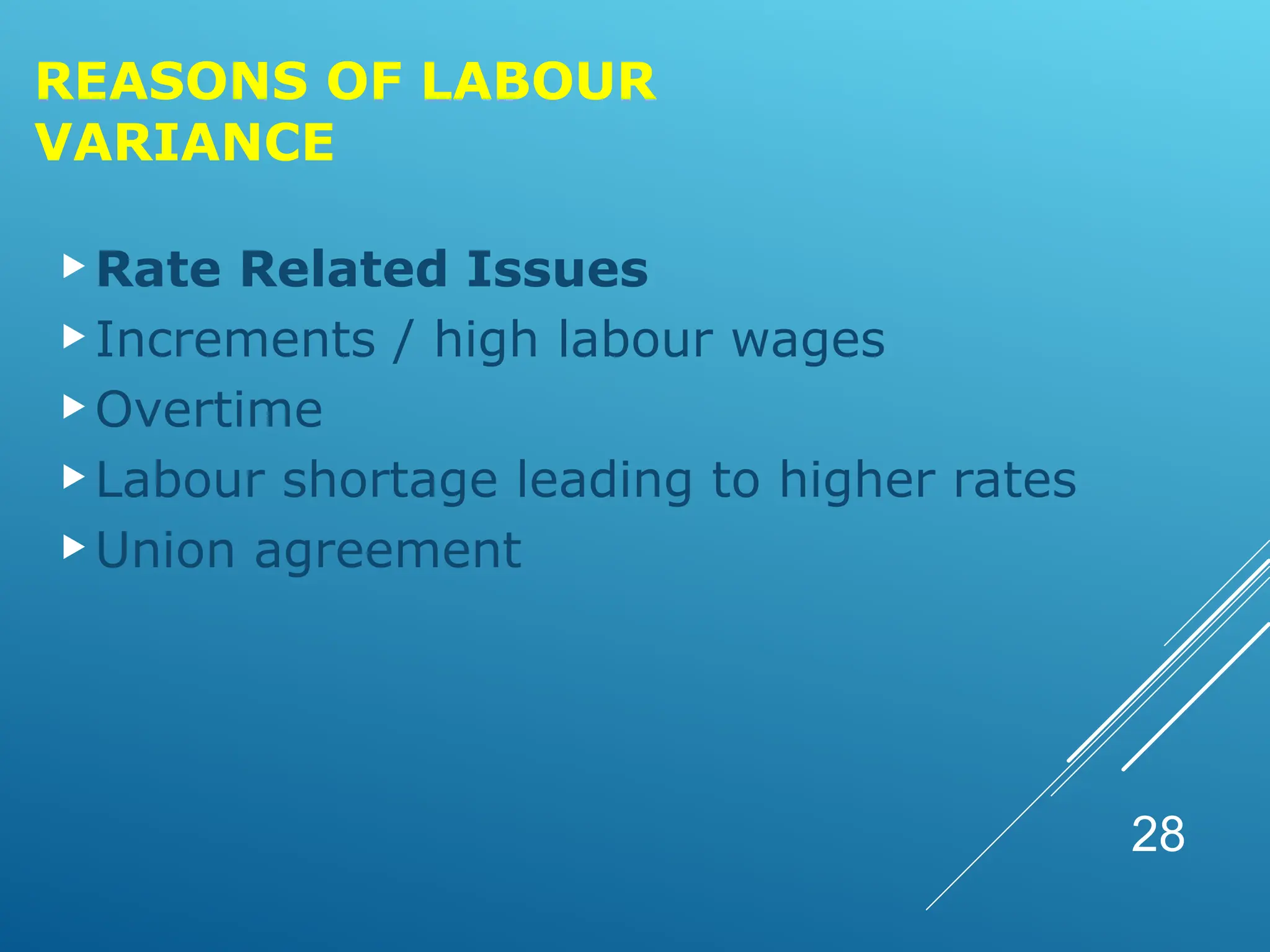

REASONS OF LABOUR

VARIANCE

RateRelated Issues

Increments / high labour wages

Overtime

Labour shortage leading to higher rates

Union agreement

28

LABOUR VARINACE

When outputis not given:

1.Labour Cost Variance: Total Standard

Labour Cost-Total Actual Labour Cost

2.Labour Rate Variance: AH[SR-AR]

3.Labour Efficiency Variance: SR[SH-

AH]

where

AH---Actual Hours SR---Standard Rate

AR---Actual Rate

SH---Standard Hours

31.

LABOUR VARINACE

When outputis given

1. Labor cost

variance:

Standard cost

Standard output

X Actual Output –Total actual

labour cost

2.Labour Rate Variance: AH[SR-AR]

3.Labour Efficiency Variance:

SR[Standard Hrs. of A X Actual Output –Actual

Hrs.A] Standard Output

32.

LABOUR VARINACE

4. LabourMix Variance:

SR[Standard Hrs. of A X Total Actual Hrs -Actual Hrs. of A]

Total Standard Hrs

5. Labour Yield Variance:

SR[Actual Yield-Standard output X Total Actual Hrs.

Total Standard Hrs.

Where SR=Standard Cost

Standard Output

6. Idle Time Variance:

Idle Time X Standard Rate

When Idle time=0,then LTEV=LEV

33.

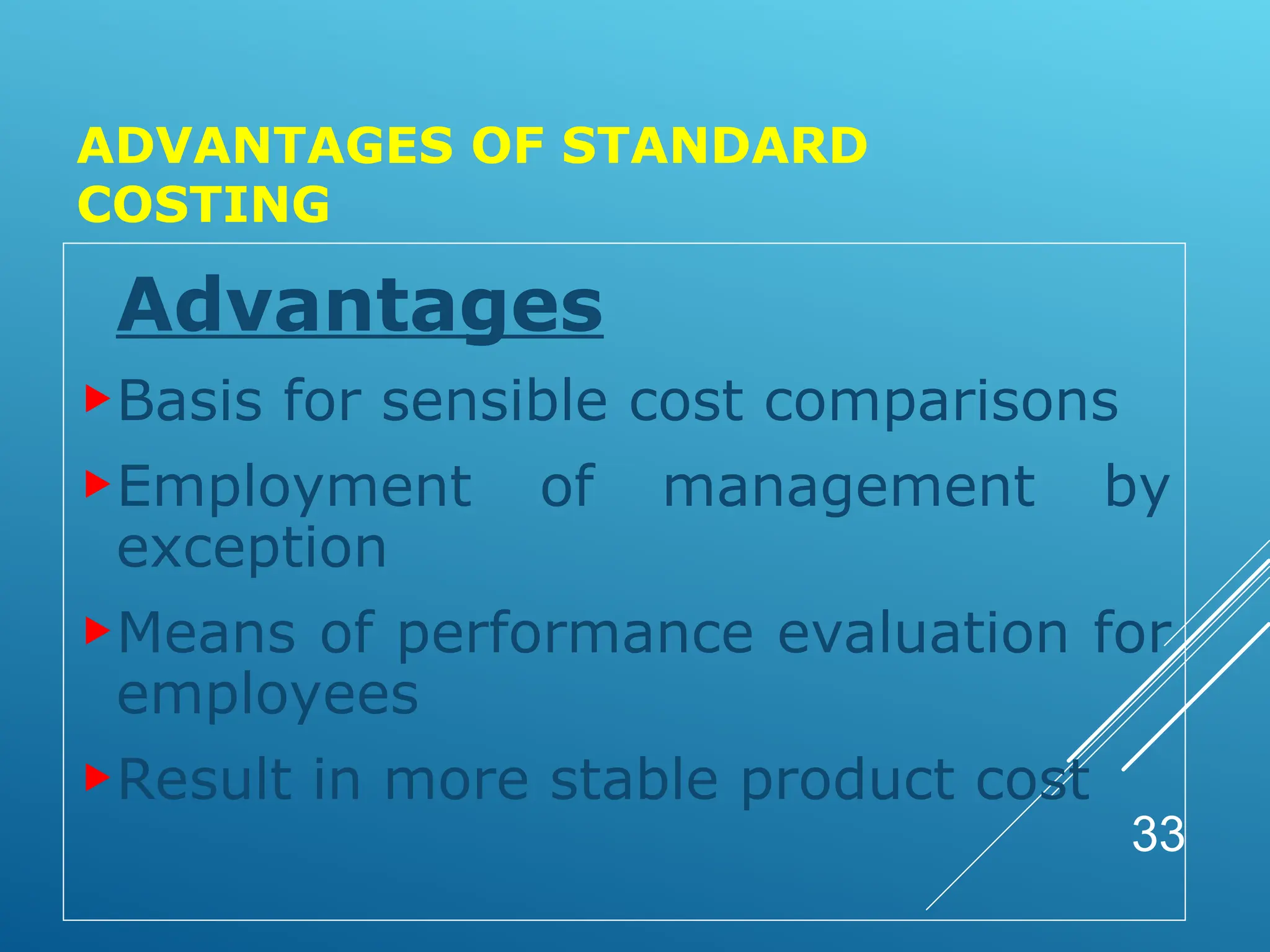

ADVANTAGES OF STANDARD

COSTING

Advantages

Basisfor sensible cost comparisons

Employment of management by

exception

Means of performance evaluation for

employees

Result in more stable product cost

33

PRACTICAL PROBLEMS

1. Afurniture company uses sunmica tops for tables. It provides the

following data:

St. Quantity for sunmica per table 4 sq. ft

St. price per sq. ft of sunmica Rs. 5

Actual prod. Of tables 1000

Sunmica actually used 4,300 sq.ft

Actual purchase price per sq. ft Rs. 5.50.

Calculate Material variances.

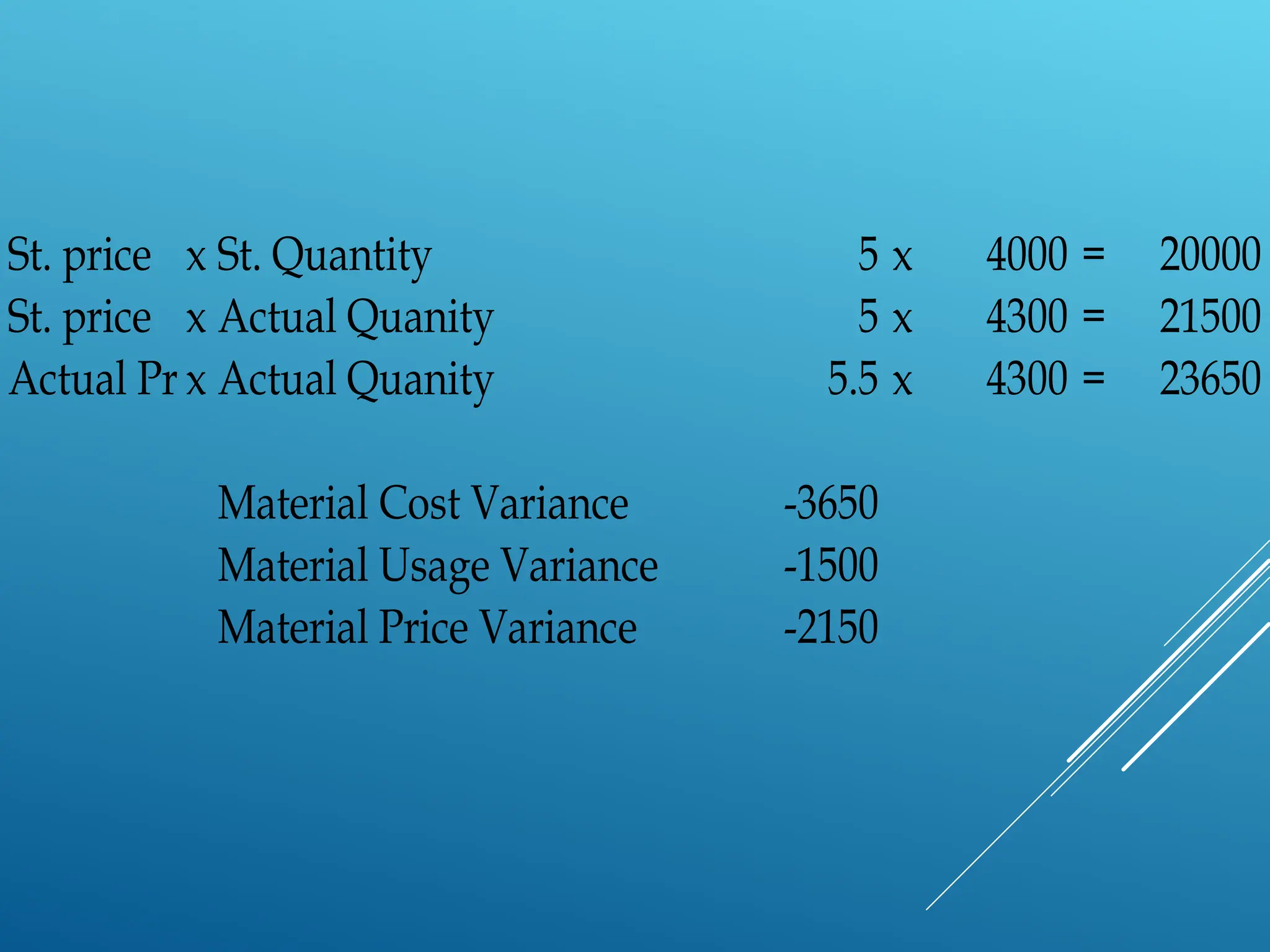

36.

St. price xSt. Quantity 5 x 4000 = 20000

St. price x Actual Quanity 5 x 4300 = 21500

Actual Price

x Actual Quanity 5.5 x 4300 = 23650

Material Cost Variance -3650

Material Usage Variance -1500

Material Price Variance -2150

37.

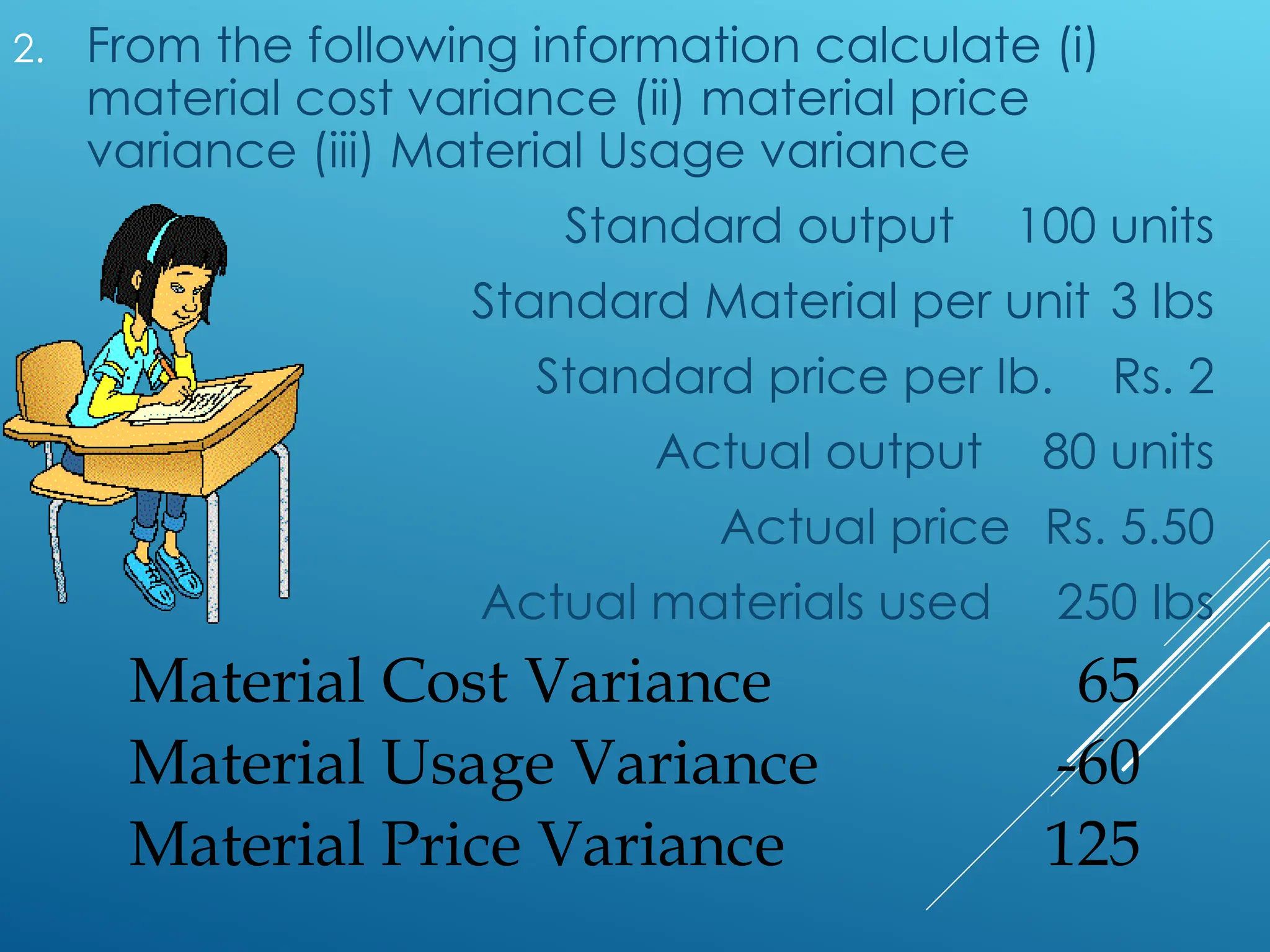

2. From thefollowing information calculate (i)

material cost variance (ii) material price

variance (iii) Material Usage variance

Standard output 100 units

Standard Material per unit 3 Ibs

Standard price per Ib. Rs. 2

Actual output 80 units

Actual price Rs. 5.50

Actual materials used 250 Ibs

Material Cost Variance 65

Material Usage Variance -60

Material Price Variance 125

38.

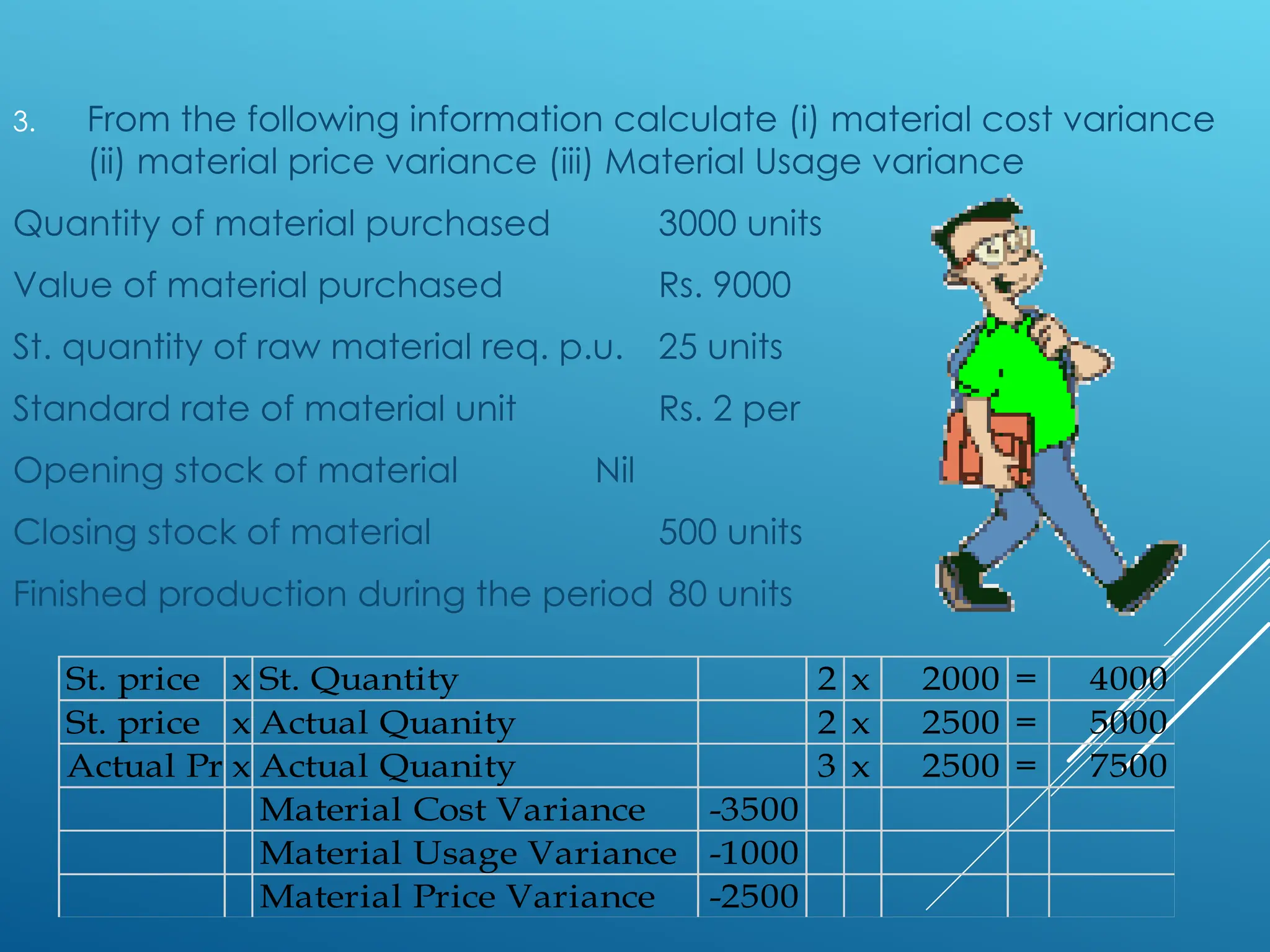

3. From thefollowing information calculate (i) material cost variance

(ii) material price variance (iii) Material Usage variance

Quantity of material purchased 3000 units

Value of material purchased Rs. 9000

St. quantity of raw material req. p.u. 25 units

Standard rate of material unit Rs. 2 per

Opening stock of material Nil

Closing stock of material 500 units

Finished production during the period 80 units

St. price x St. Quantity 2 x 2000 = 4000

St. price x Actual Quanity 2 x 2500 = 5000

Actual Price

x Actual Quanity 3 x 2500 = 7500

Material Cost Variance -3500

Material Usage Variance -1000

Material Price Variance -2500

39.

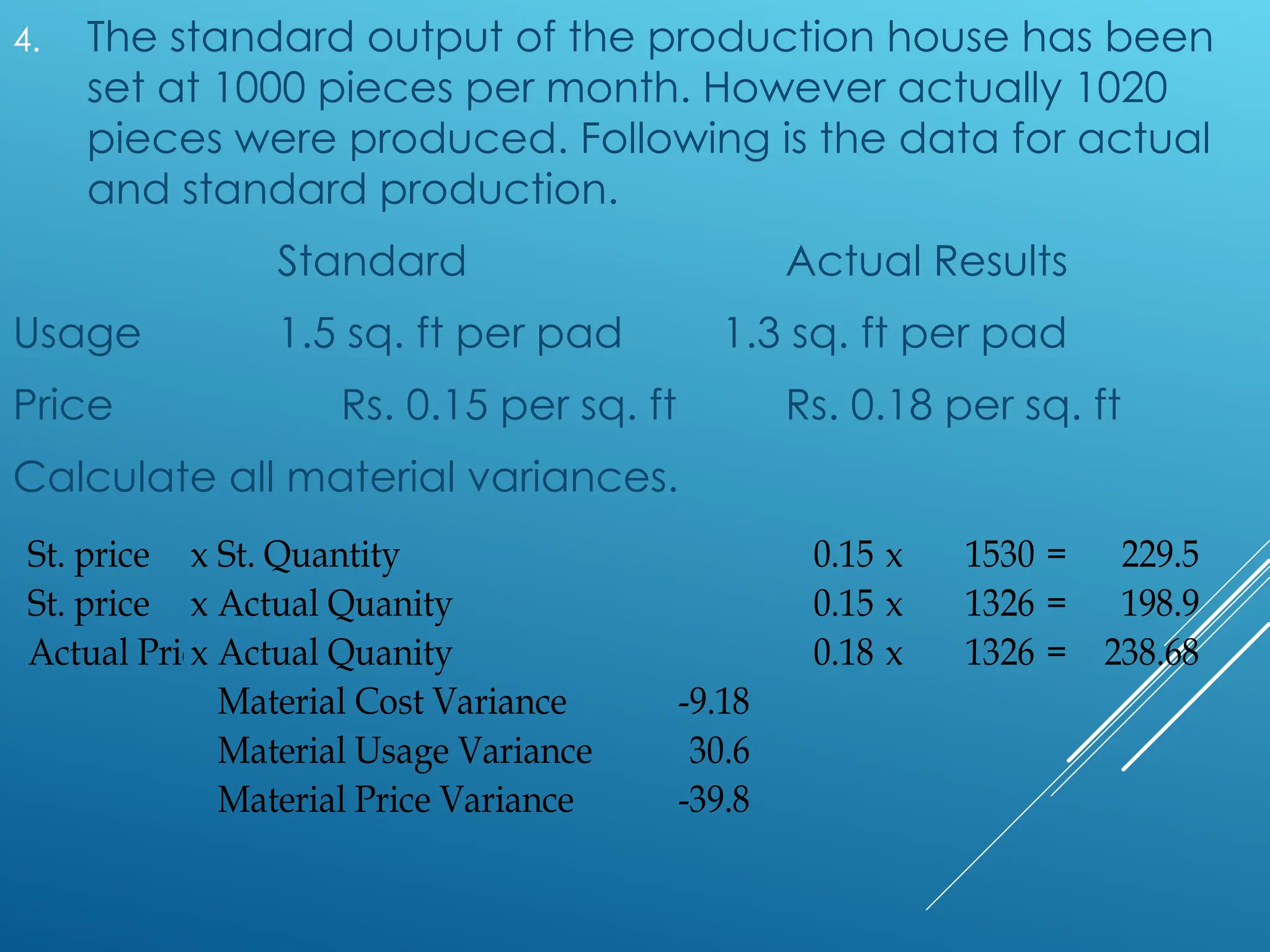

4. The standardoutput of the production house has been

set at 1000 pieces per month. However actually 1020

pieces were produced. Following is the data for actual

and standard production.

Standard Actual Results

Usage 1.5 sq. ft per pad 1.3 sq. ft per pad

Price Rs. 0.15 per sq. ft Rs. 0.18 per sq. ft

Calculate all material variances.

St. price x St. Quantity 0.15 x 1530 = 229.5

St. price x Actual Quanity 0.15 x 1326 = 198.9

Actual Price

x Actual Quanity 0.18 x 1326 = 238.68

Material Cost Variance -9.18

Material Usage Variance 30.6

Material Price Variance -39.8

40.

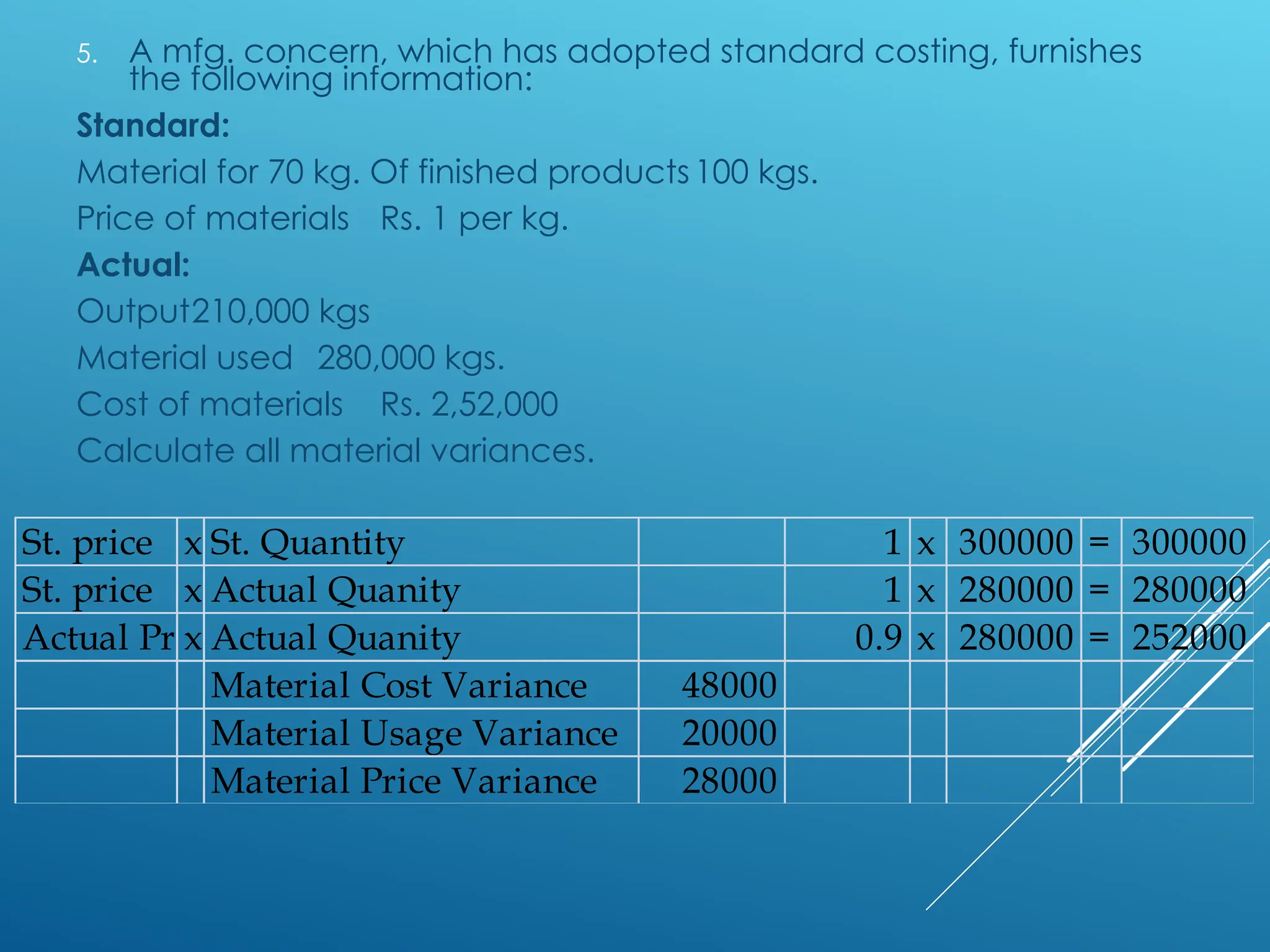

St. price xSt. Quantity 1 x 300000 = 300000

St. price x Actual Quanity 1 x 280000 = 280000

Actual Price

x Actual Quanity 0.9 x 280000 = 252000

Material Cost Variance 48000

Material Usage Variance 20000

Material Price Variance 28000

5. A mfg. concern, which has adopted standard costing, furnishes

the following information:

Standard:

Material for 70 kg. Of finished products100 kgs.

Price of materials Rs. 1 per kg.

Actual:

Output210,000 kgs

Material used 280,000 kgs.

Cost of materials Rs. 2,52,000

Calculate all material variances.

41.

MATERIAL MIX VARIANCE

Material Mix Variance

= [Revised St. Qty – Actual Qty] x St. Price

Rev. St. Qty = St. Qty of 1 Mat. x Actual Total

Standard Total

42.

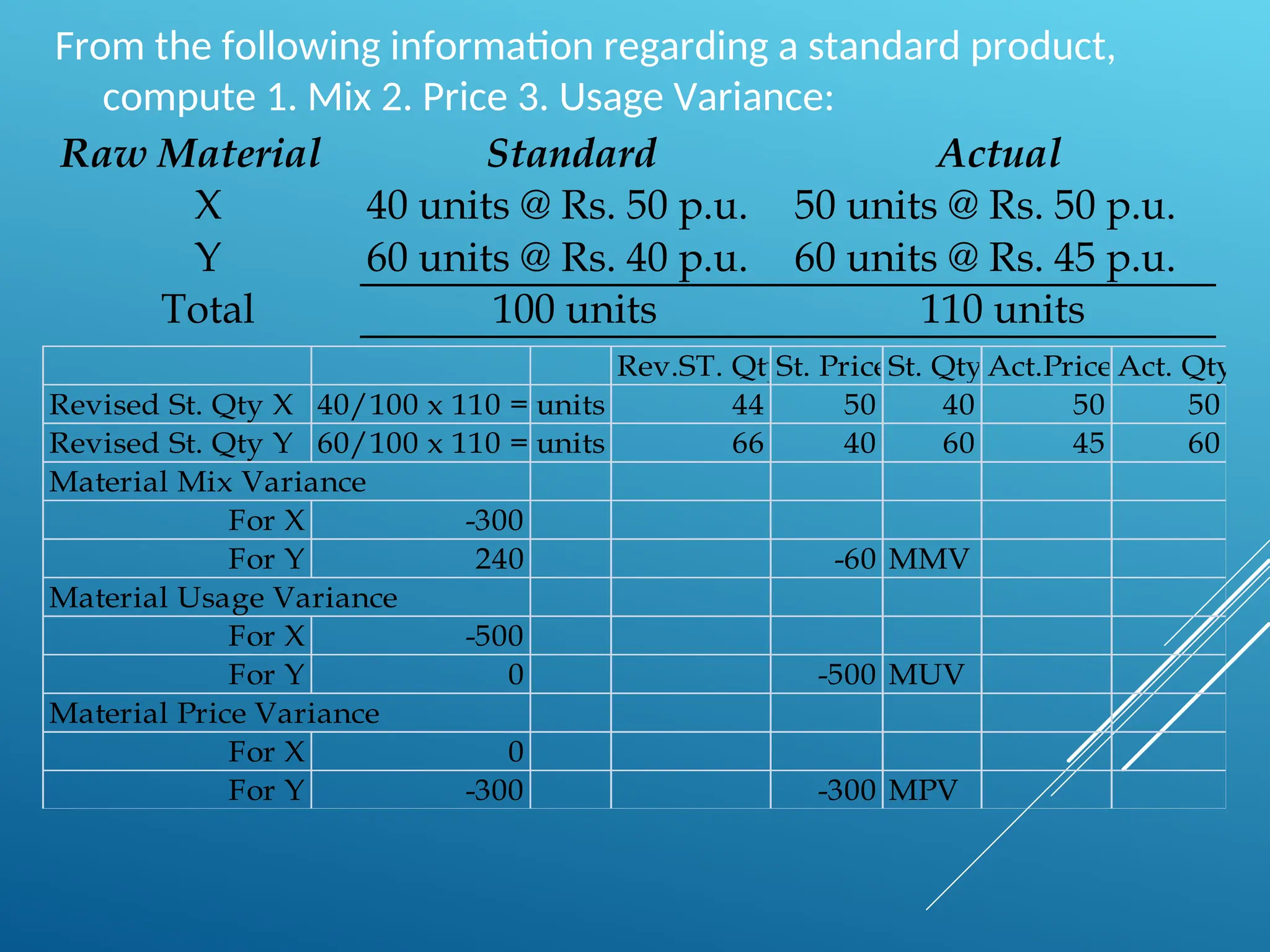

From the followinginformation regarding a standard product,

compute 1. Mix 2. Price 3. Usage Variance:

Raw Material Standard Actual

X 40 units @ Rs. 50 p.u. 50 units @ Rs. 50 p.u.

Y 60 units @ Rs. 40 p.u. 60 units @ Rs. 45 p.u.

Total 100 units 110 units

Rev.ST. Qty

St. PriceSt. QtyAct.Price Act. Qty

Revised St. Qty X 40/100 x 110 = units 44 50 40 50 50

Revised St. Qty Y 60/100 x 110 = units 66 40 60 45 60

Material Mix Variance

For X -300

For Y 240 -60 MMV

Material Usage Variance

For X -500

For Y 0 -500 MUV

Material Price Variance

For X 0

For Y -300 -300 MPV

43.

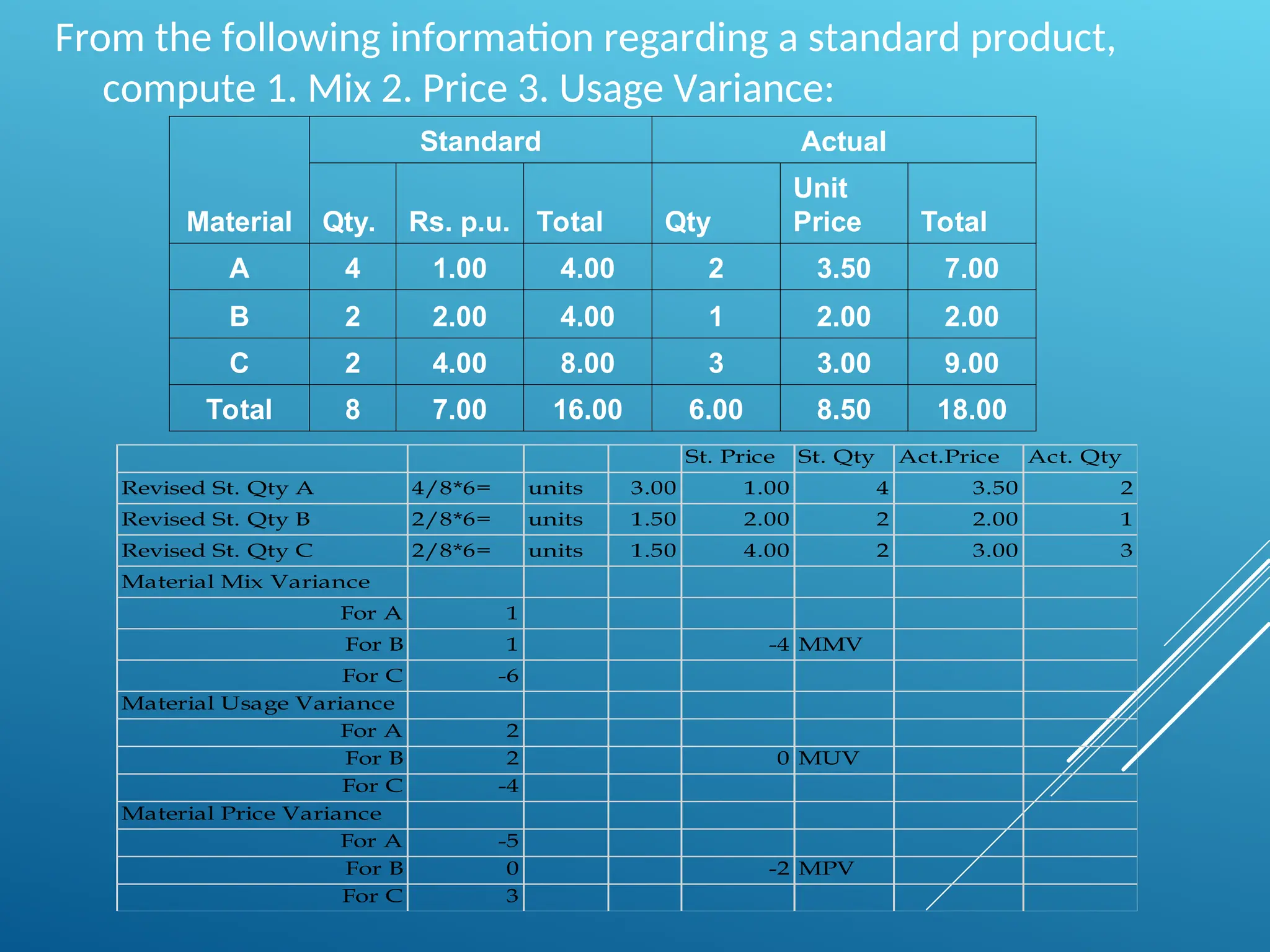

From the followinginformation regarding a standard product,

compute 1. Mix 2. Price 3. Usage Variance:

Material

Standard Actual

Qty. Rs. p.u. Total Qty

Unit

Price Total

A 4 1.00 4.00 2 3.50 7.00

B 2 2.00 4.00 1 2.00 2.00

C 2 4.00 8.00 3 3.00 9.00

Total 8 7.00 16.00 6.00 8.50 18.00

St. Price St. Qty Act.Price Act. Qty

Revised St. Qty A 4/8*6= units 3.00 1.00 4 3.50 2

Revised St. Qty B 2/8*6= units 1.50 2.00 2 2.00 1

Revised St. Qty C 2/8*6= units 1.50 4.00 2 3.00 3

Material Mix Variance

For A 1

For B 1 -4 MMV

For C -6

Material Usage Variance

For A 2

For B 2 0 MUV

For C -4

Material Price Variance

For A -5

For B 0 -2 MPV

For C 3

44.

Material variances

• LabourCost Variance SH*SR – AH*AR

• Labour Usage/Efficie. Var (SH-AHactual)*SR

• Labour Rate Variance (SR-AR)* AH

• Idle time Variance SR*Idle time

LABOUR VARIANCES

45.

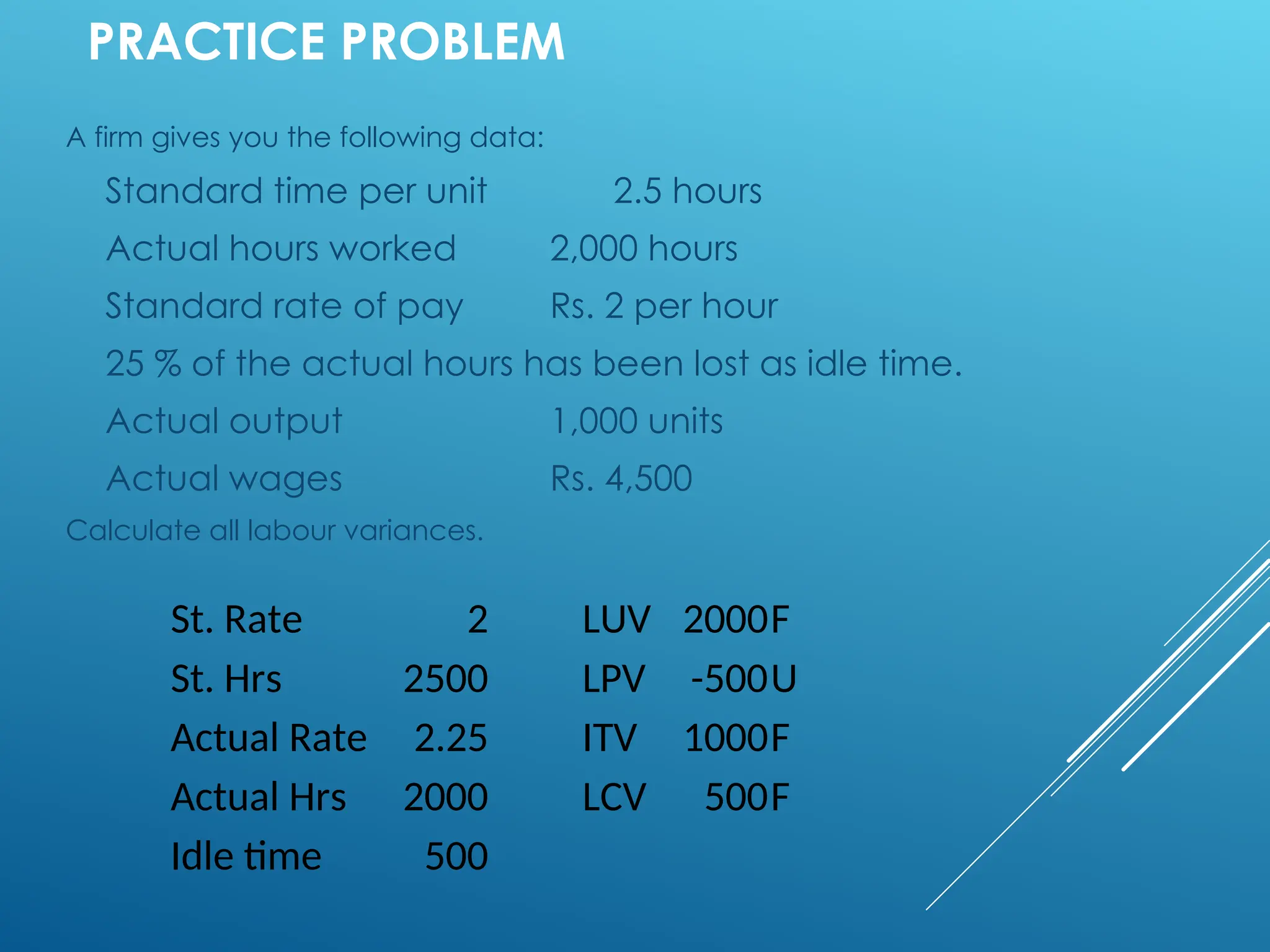

PRACTICE PROBLEM

A firmgives you the following data:

Standard time per unit 2.5 hours

Actual hours worked 2,000 hours

Standard rate of pay Rs. 2 per hour

25 % of the actual hours has been lost as idle time.

Actual output 1,000 units

Actual wages Rs. 4,500

Calculate all labour variances.

St. Rate 2 LUV 2000F

St. Hrs 2500 LPV -500U

Actual Rate 2.25 ITV 1000F

Actual Hrs 2000 LCV 500F

Idle time 500

46.

PRACTICE PROBLEMS

Compute theLabour variances from the

information given below:

Standard time 3 hours per unit

Standard rate of wages Rs. 6 per hour

Actual production 700 units

Actual time taken 2000 hours

Actual Wages Rs. 14000

Idle time 50 hours

St. Rate 6 LUV 900F

St. Hrs 2100 LPV -2000U

Actual Rate 7 LCV -1400U

Actual Hrs 2000 IDV 300

Idle time 50

![LABOUR VARINACE

When output is not given:

1.Labour Cost Variance: Total Standard

Labour Cost-Total Actual Labour Cost

2.Labour Rate Variance: AH[SR-AR]

3.Labour Efficiency Variance: SR[SH-

AH]

where

AH---Actual Hours SR---Standard Rate

AR---Actual Rate

SH---Standard Hours](https://image.slidesharecdn.com/unit2standardcosting-250311045920-51569f22/75/Unit-2-Standard-costing-ppt-finance-and-costing-30-2048.jpg)

![LABOUR VARINACE

When output is given

1. Labor cost

variance:

Standard cost

Standard output

X Actual Output –Total actual

labour cost

2.Labour Rate Variance: AH[SR-AR]

3.Labour Efficiency Variance:

SR[Standard Hrs. of A X Actual Output –Actual

Hrs.A] Standard Output](https://image.slidesharecdn.com/unit2standardcosting-250311045920-51569f22/75/Unit-2-Standard-costing-ppt-finance-and-costing-31-2048.jpg)

![LABOUR VARINACE

4. Labour Mix Variance:

SR[Standard Hrs. of A X Total Actual Hrs -Actual Hrs. of A]

Total Standard Hrs

5. Labour Yield Variance:

SR[Actual Yield-Standard output X Total Actual Hrs.

Total Standard Hrs.

Where SR=Standard Cost

Standard Output

6. Idle Time Variance:

Idle Time X Standard Rate

When Idle time=0,then LTEV=LEV](https://image.slidesharecdn.com/unit2standardcosting-250311045920-51569f22/75/Unit-2-Standard-costing-ppt-finance-and-costing-32-2048.jpg)

![MATERIAL MIX VARIANCE

Material Mix Variance

= [Revised St. Qty – Actual Qty] x St. Price

Rev. St. Qty = St. Qty of 1 Mat. x Actual Total

Standard Total](https://image.slidesharecdn.com/unit2standardcosting-250311045920-51569f22/75/Unit-2-Standard-costing-ppt-finance-and-costing-41-2048.jpg)