Downloaded 61 times

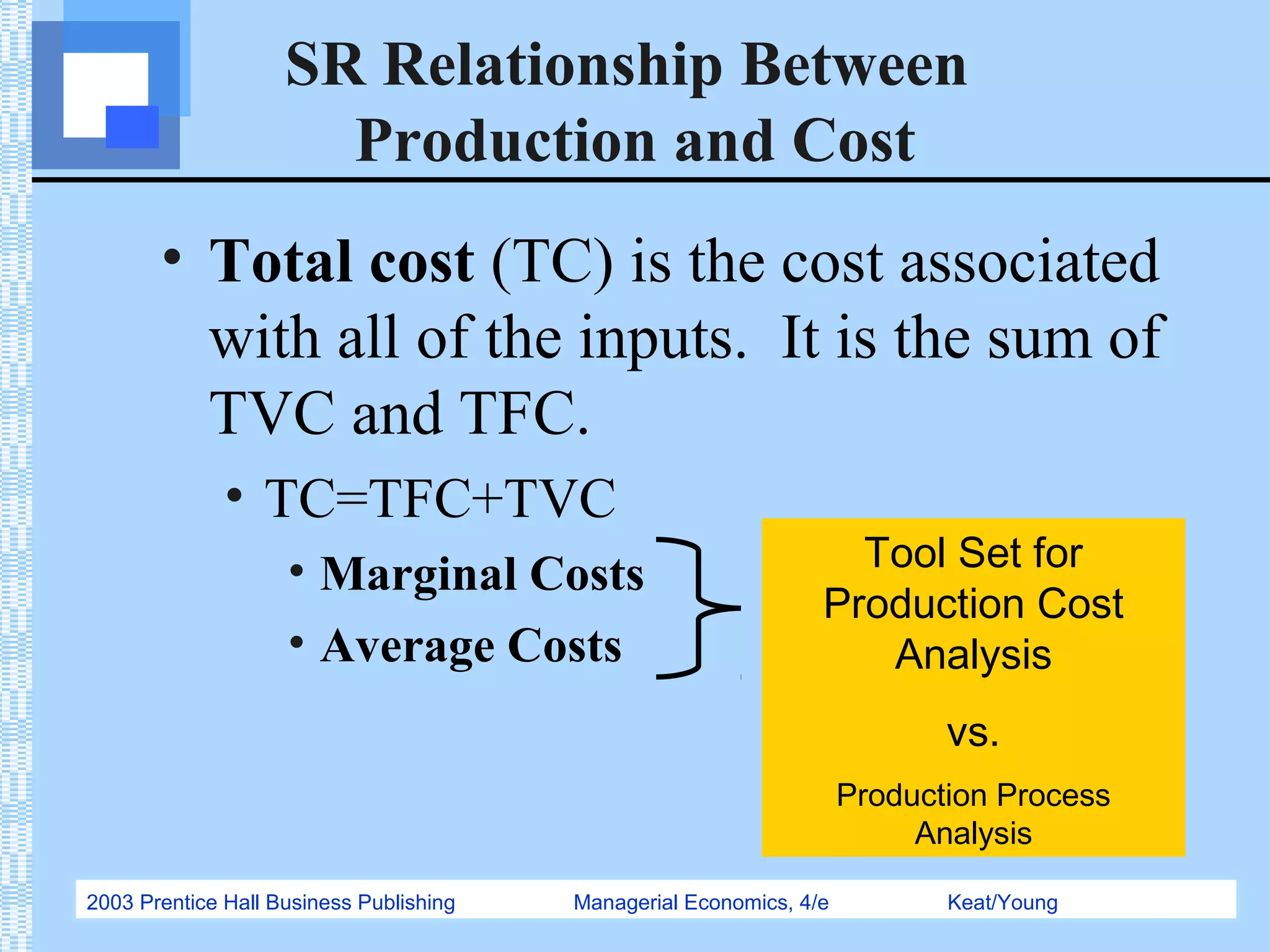

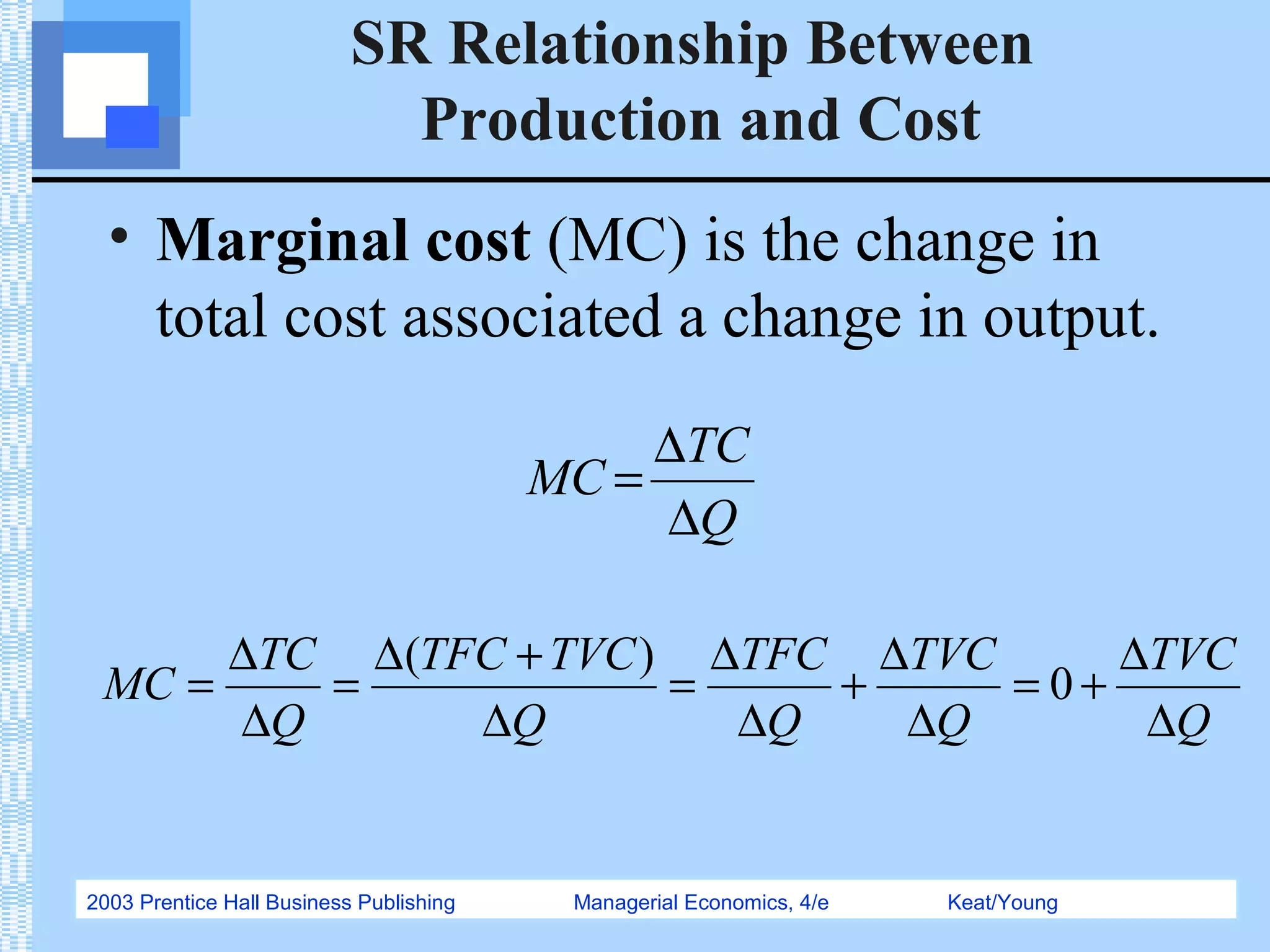

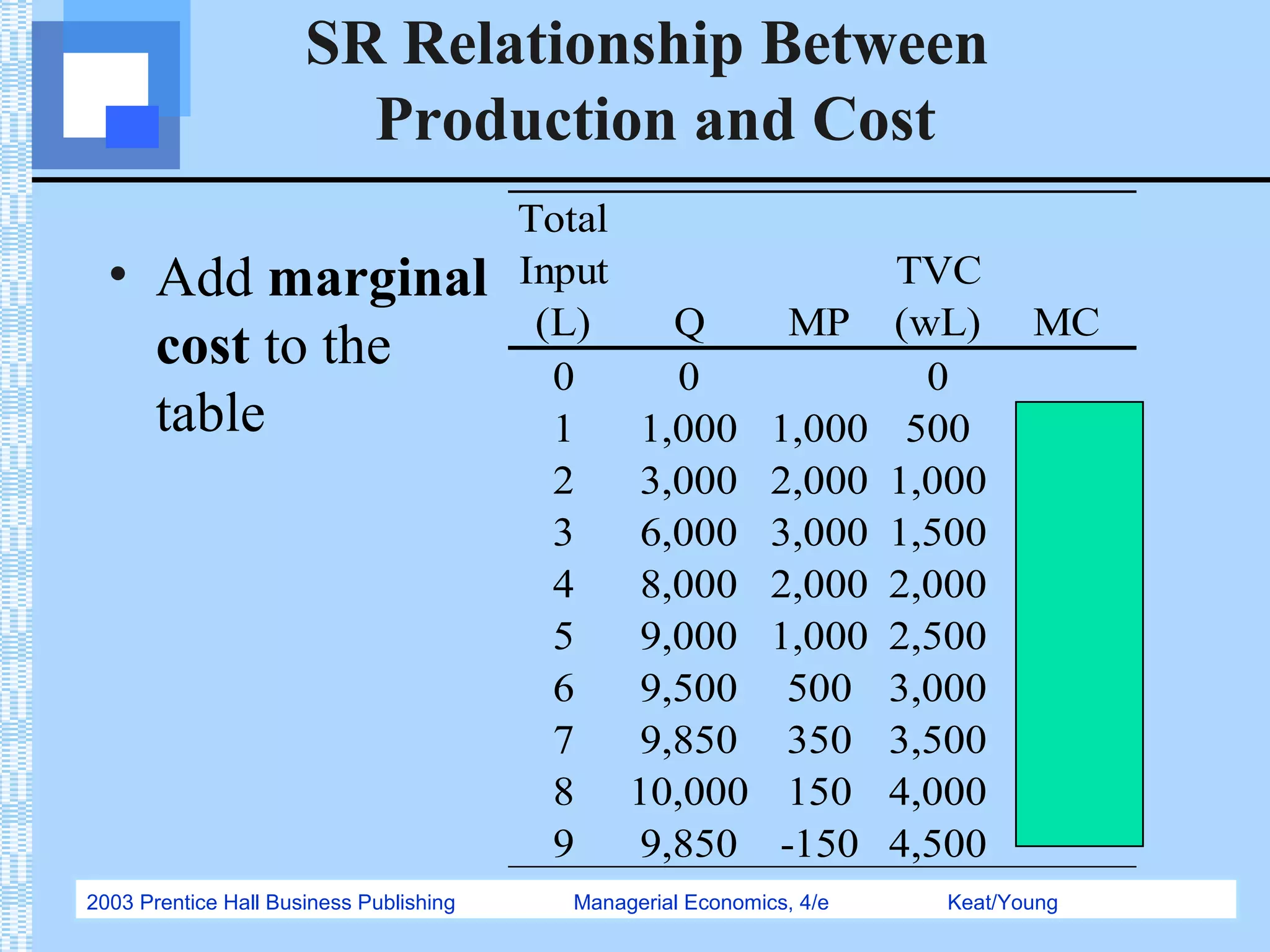

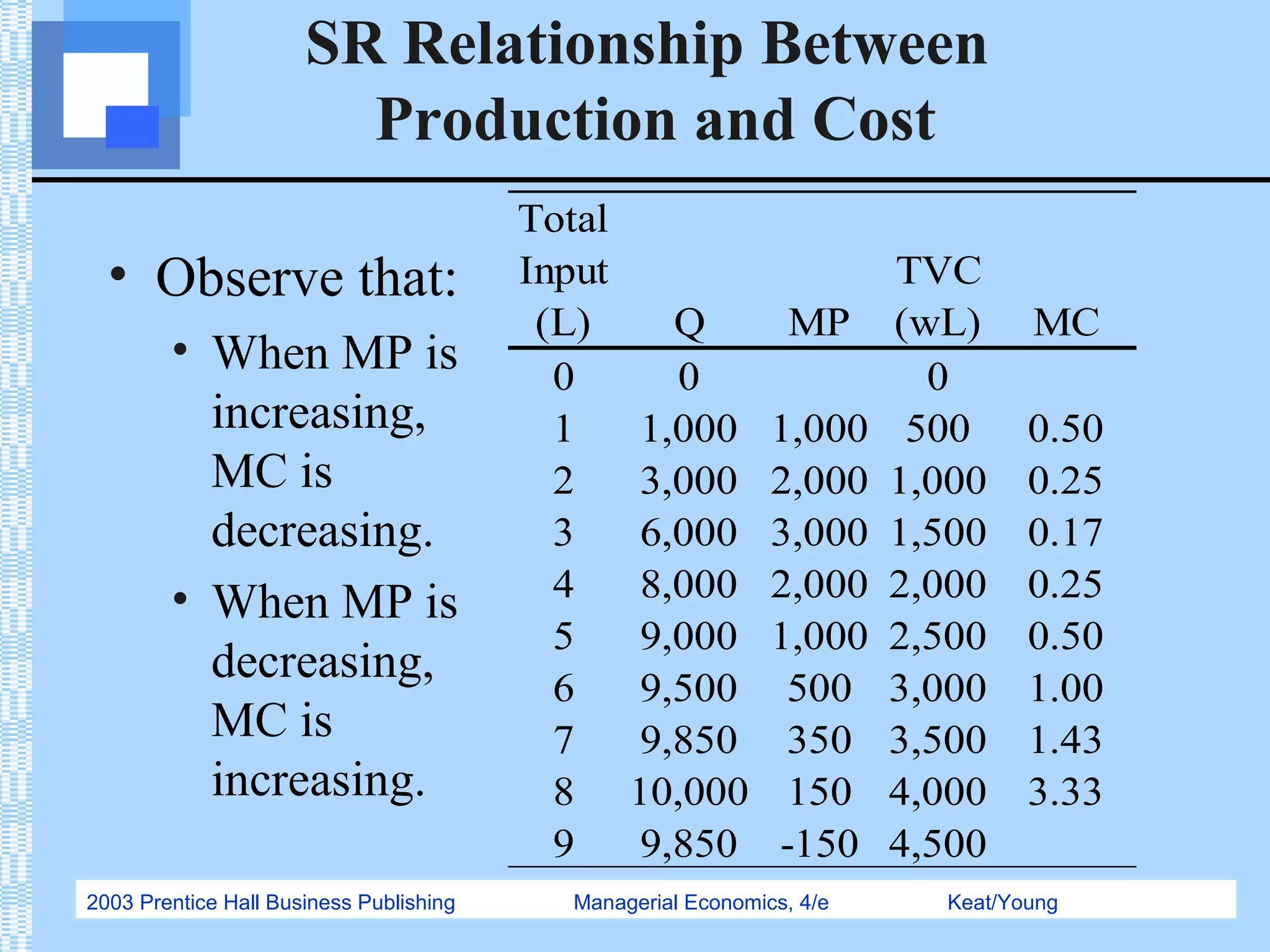

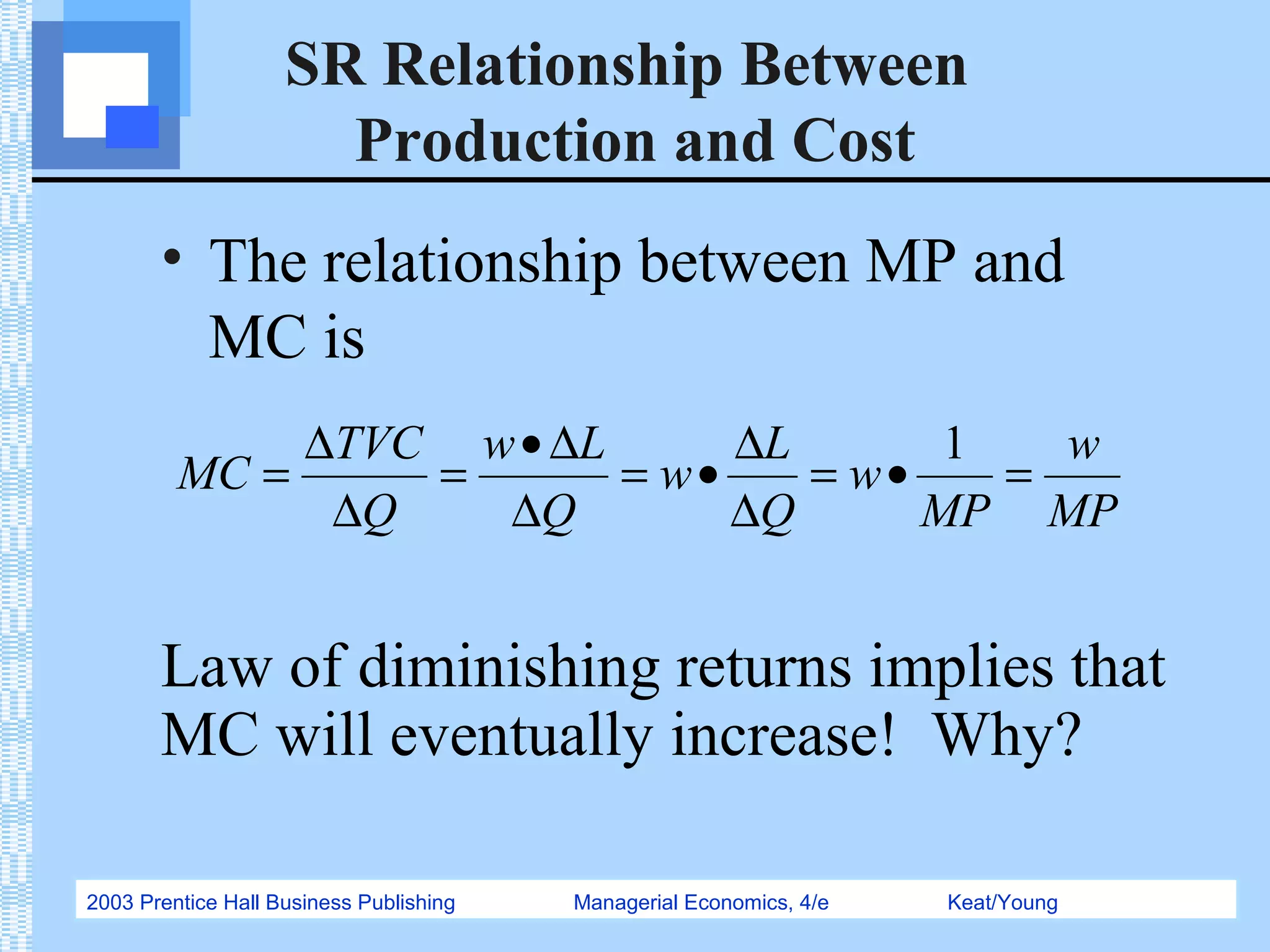

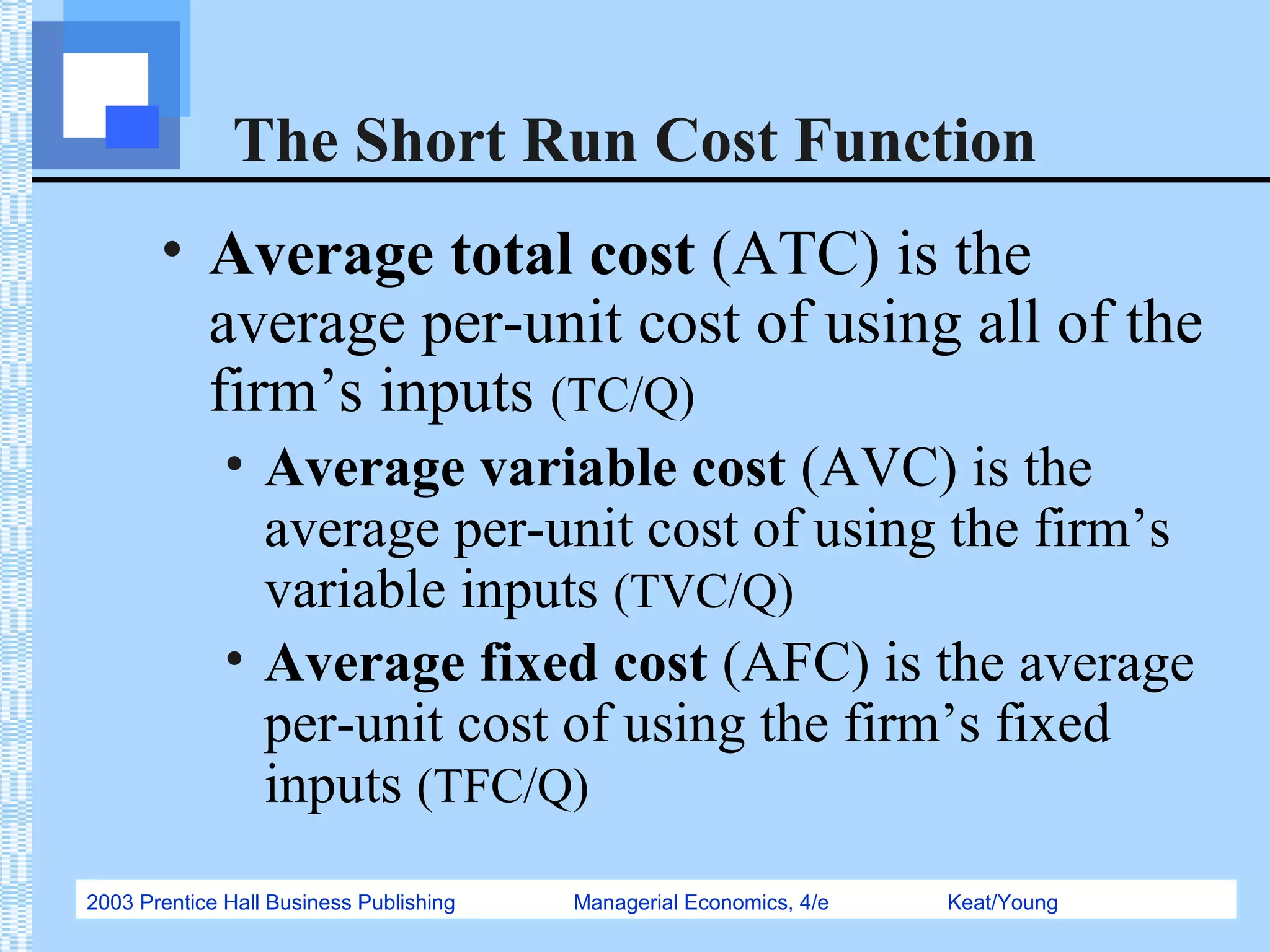

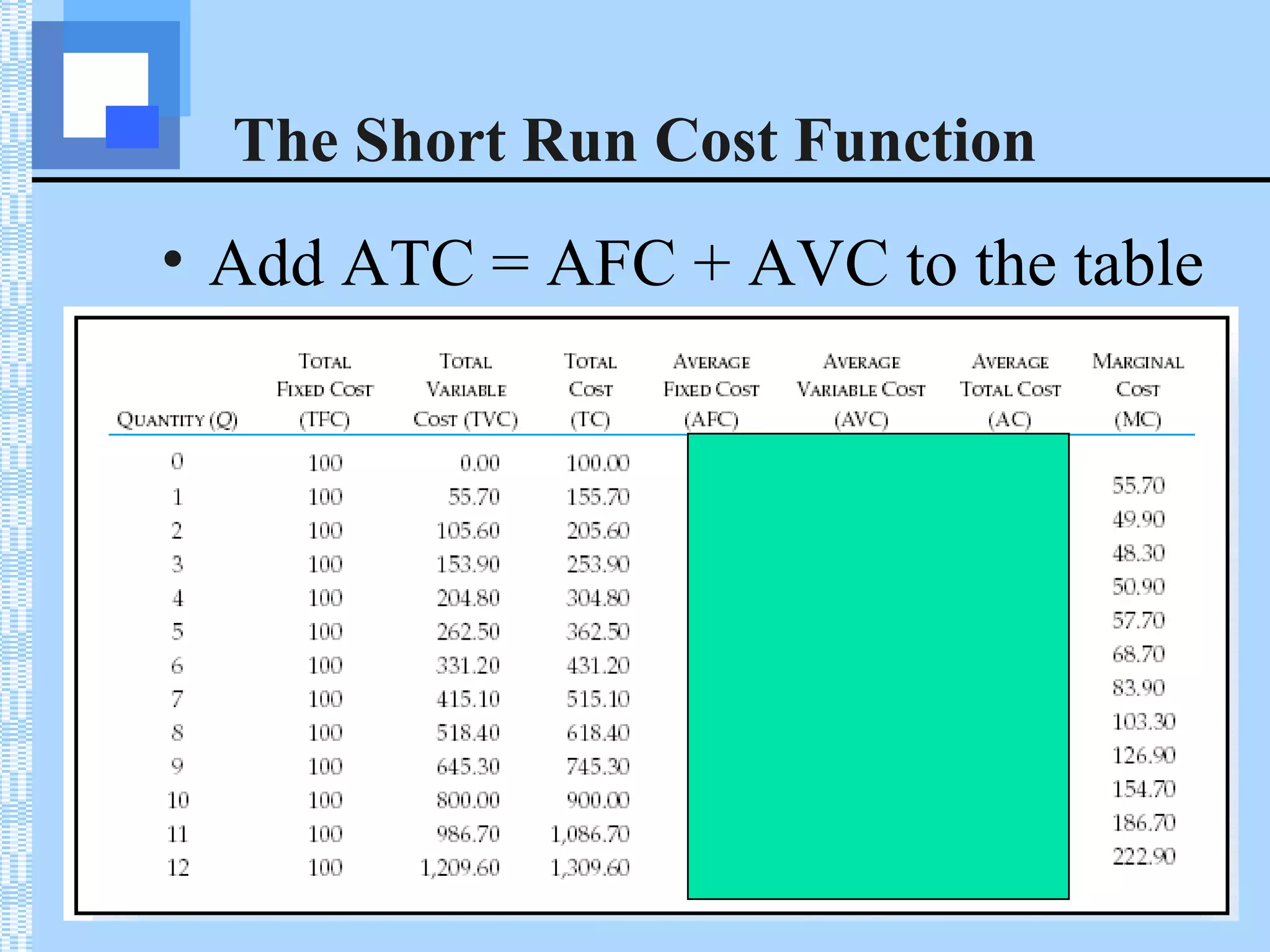

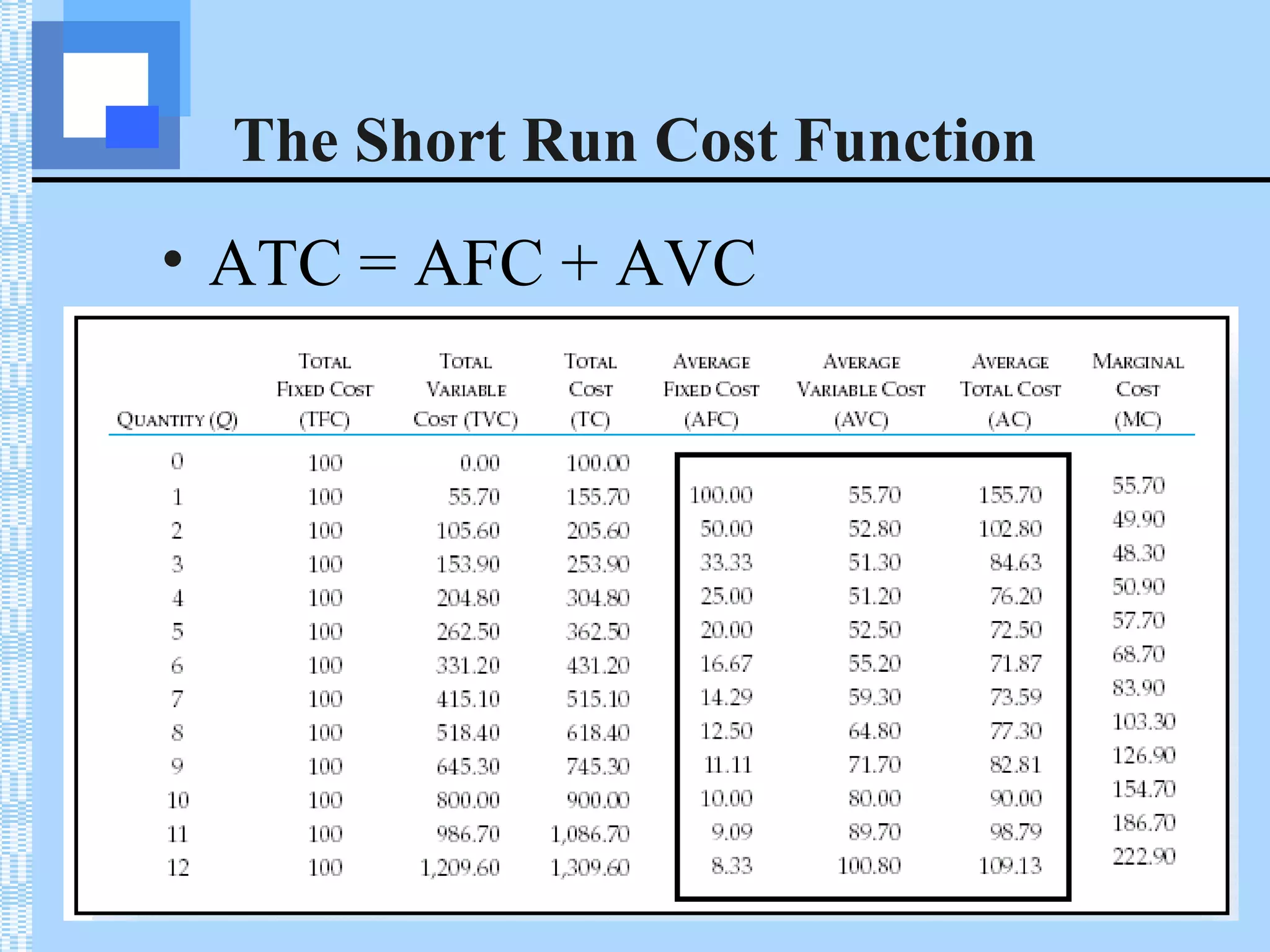

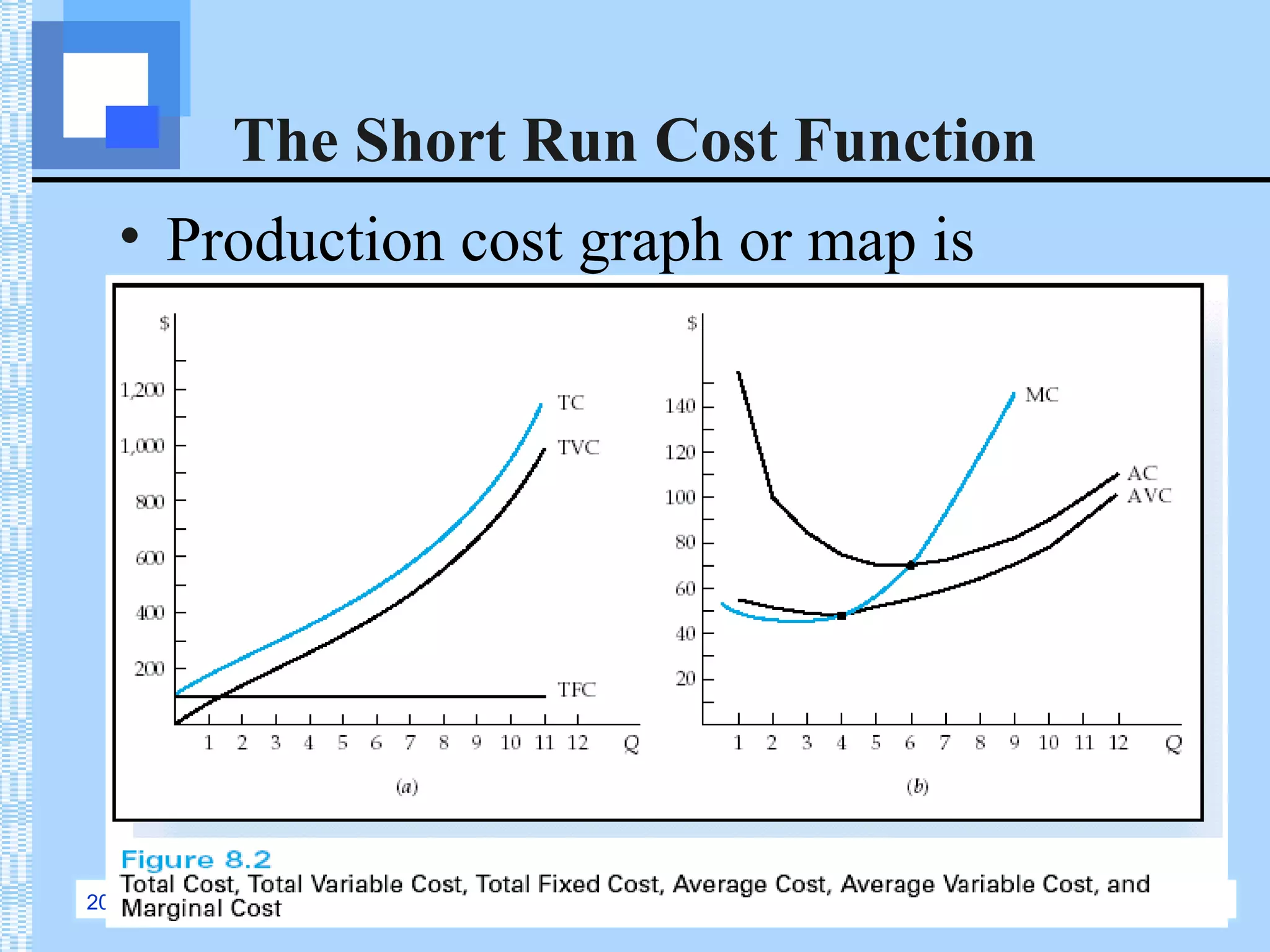

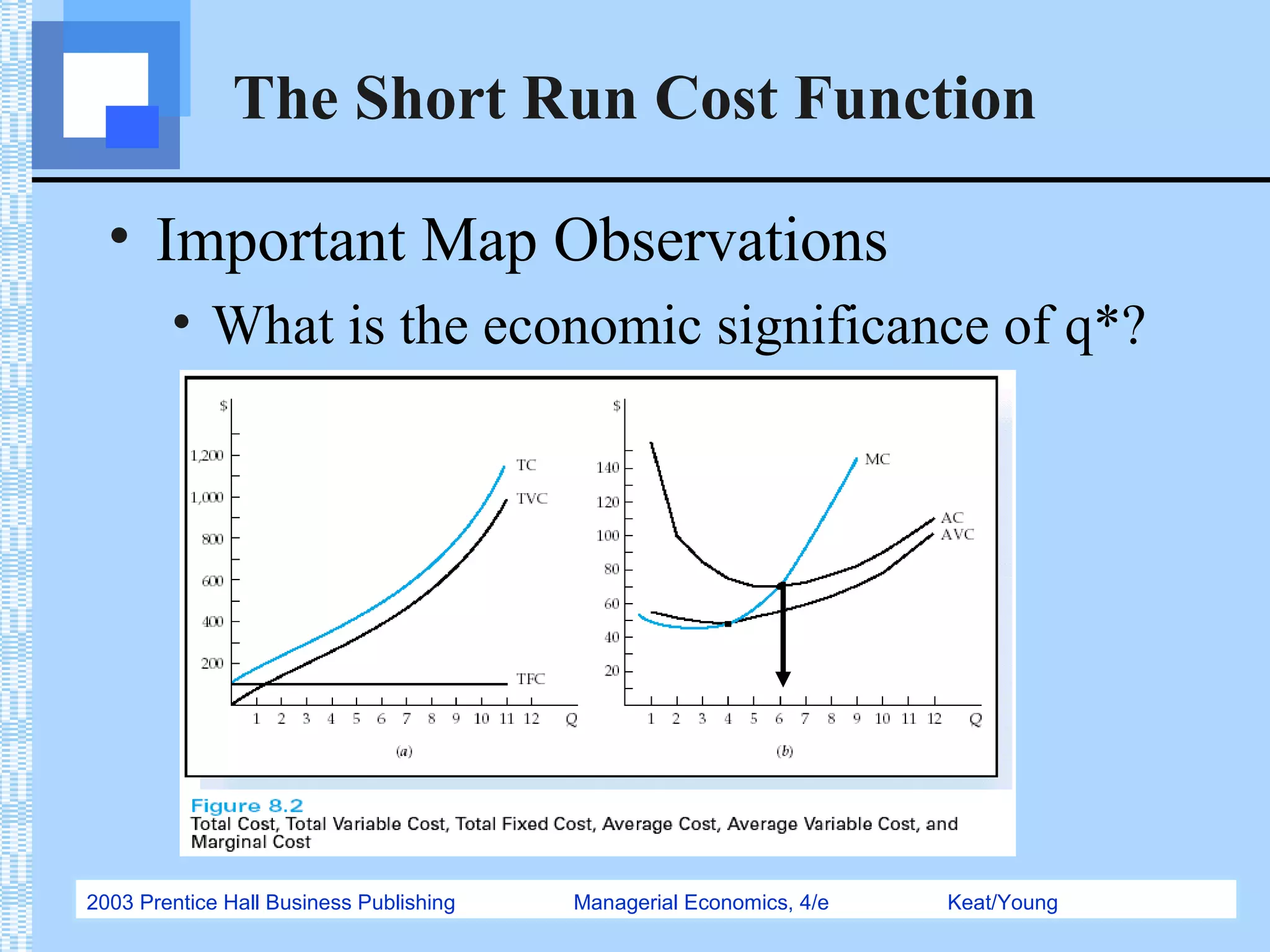

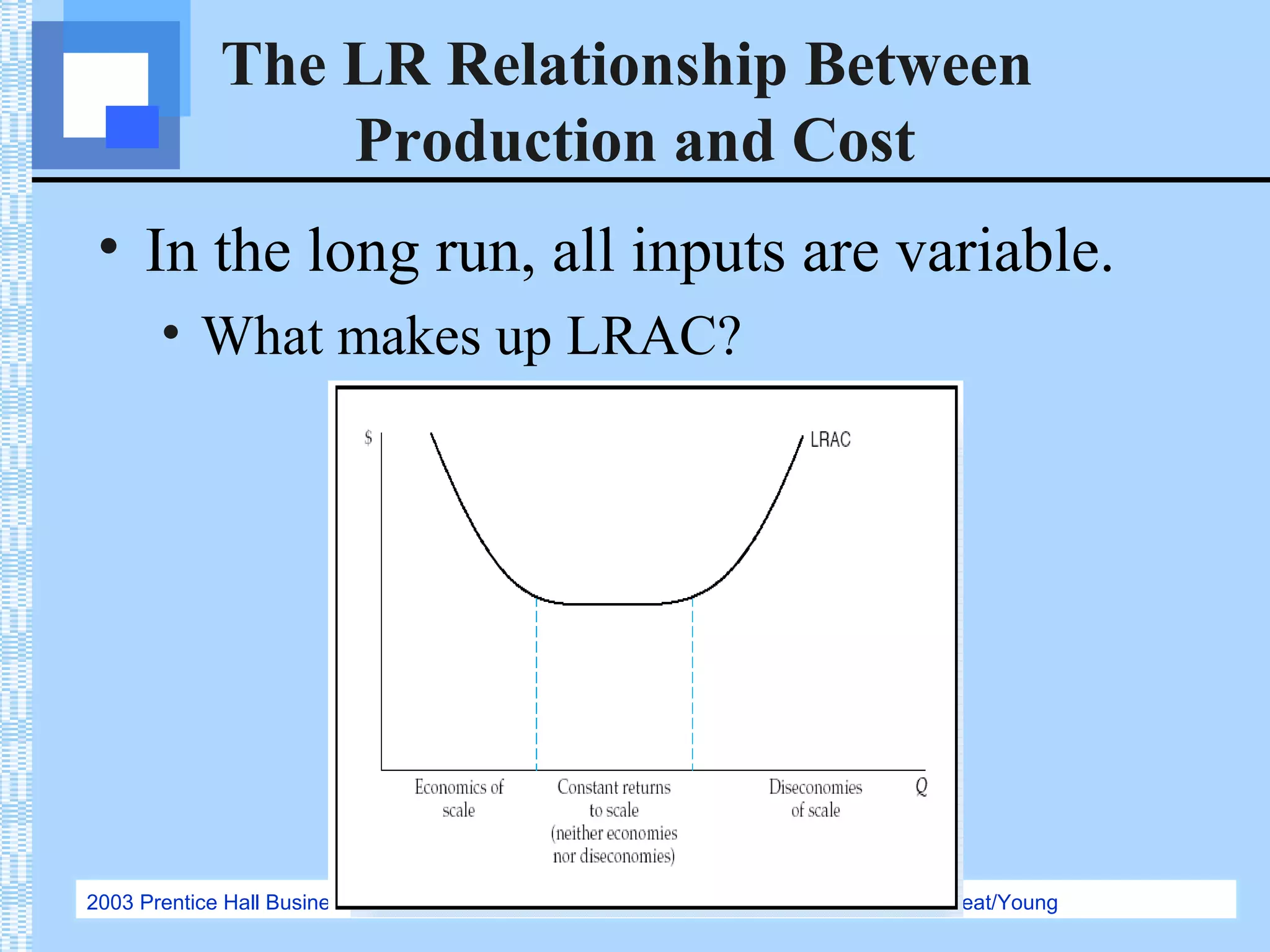

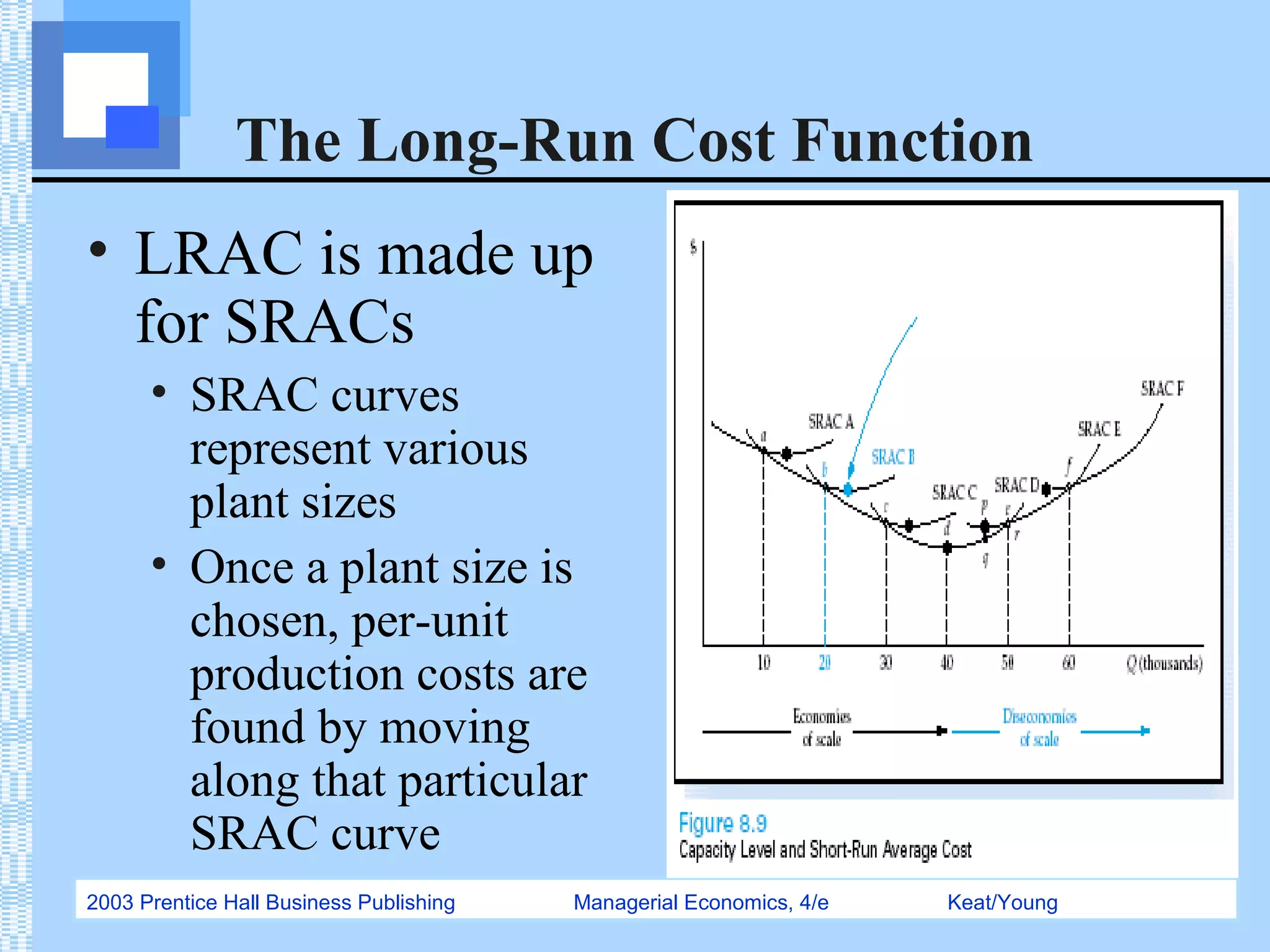

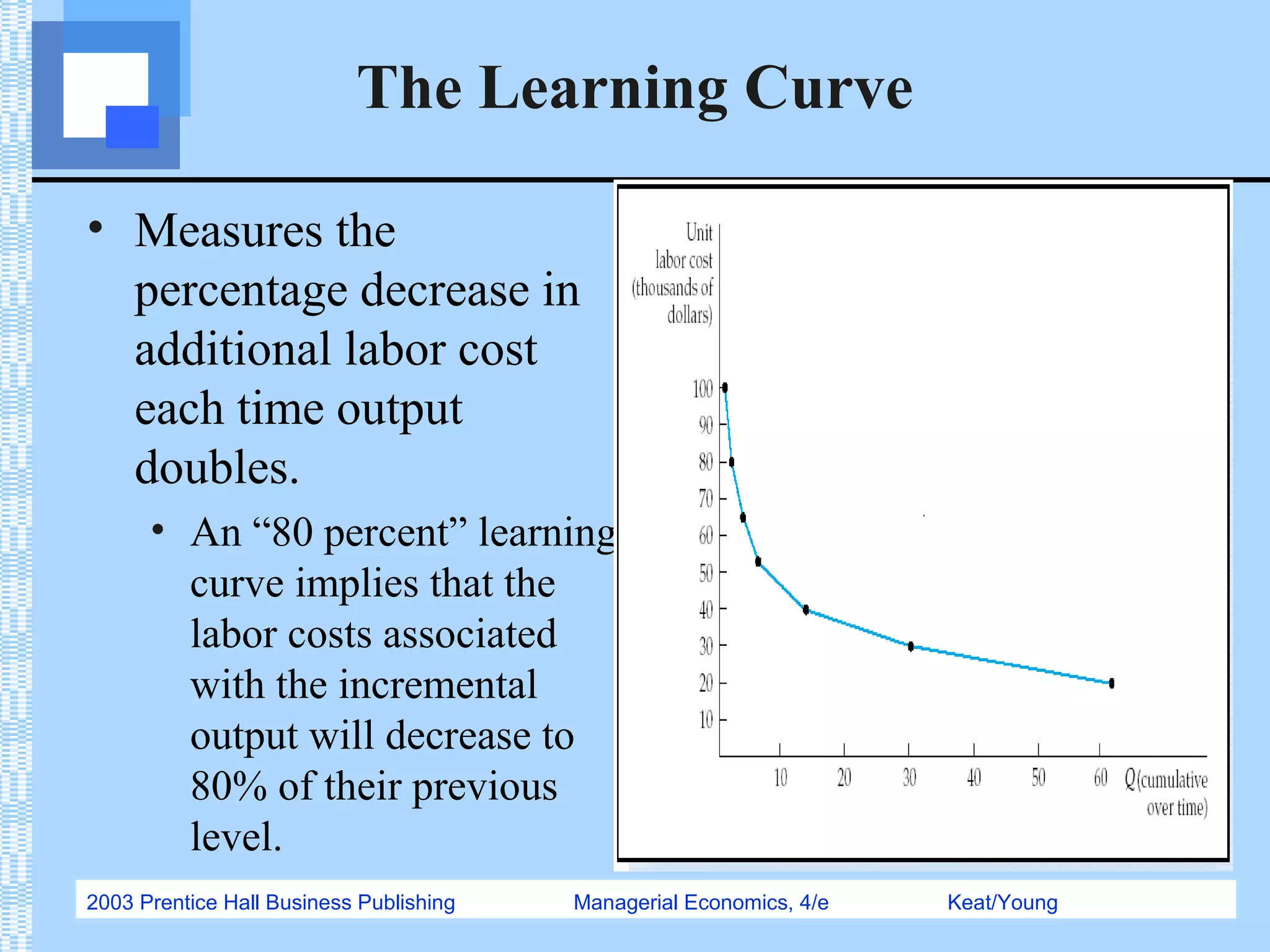

Chapter 8 discusses the theory and estimation of costs in managerial economics, covering definitions and types of costs, short-run and long-run relationships between production and costs, and the impact of input prices on cost curves. Key concepts include average total cost, marginal cost, and the learning curve, along with their significance in production cost analysis. The chapter highlights the importance of understanding cost structures for effective managerial decision-making.

![Chapter8[1]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter81-120304043835-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)