Downloaded 1,051 times

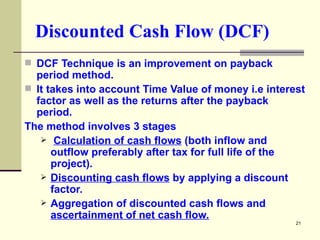

The document discusses various capital budgeting and investment appraisal methods used to evaluate long-term investment projects. It defines capital budgeting as the formal process of planning and acquiring capital assets and explains why it is important. Several evaluation techniques are covered, including payback period, net present value (NPV), internal rate of return (IRR), and accounting rate of return. The key criteria for accepting or rejecting projects using these methods are also provided.