Downloaded 725 times

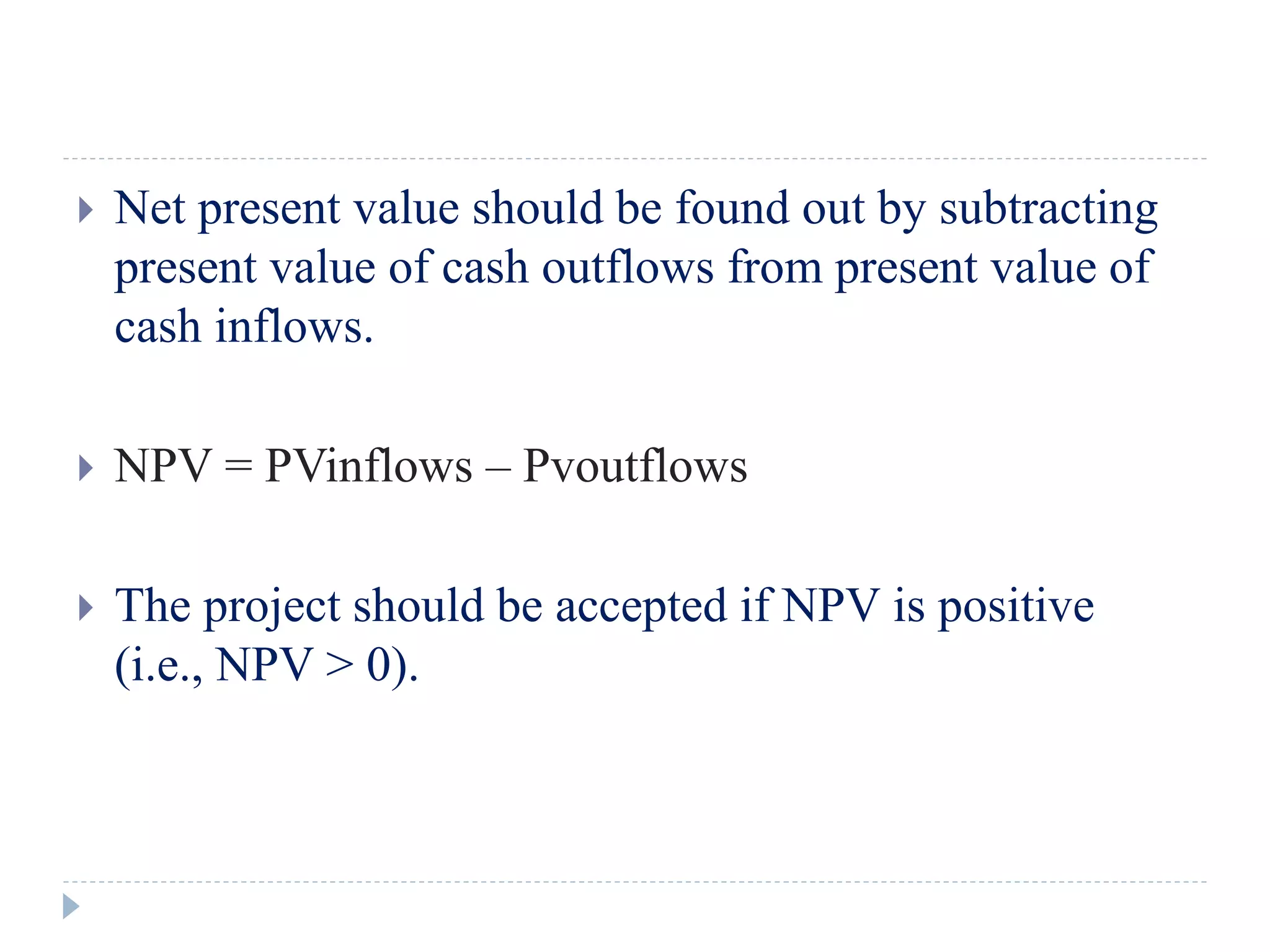

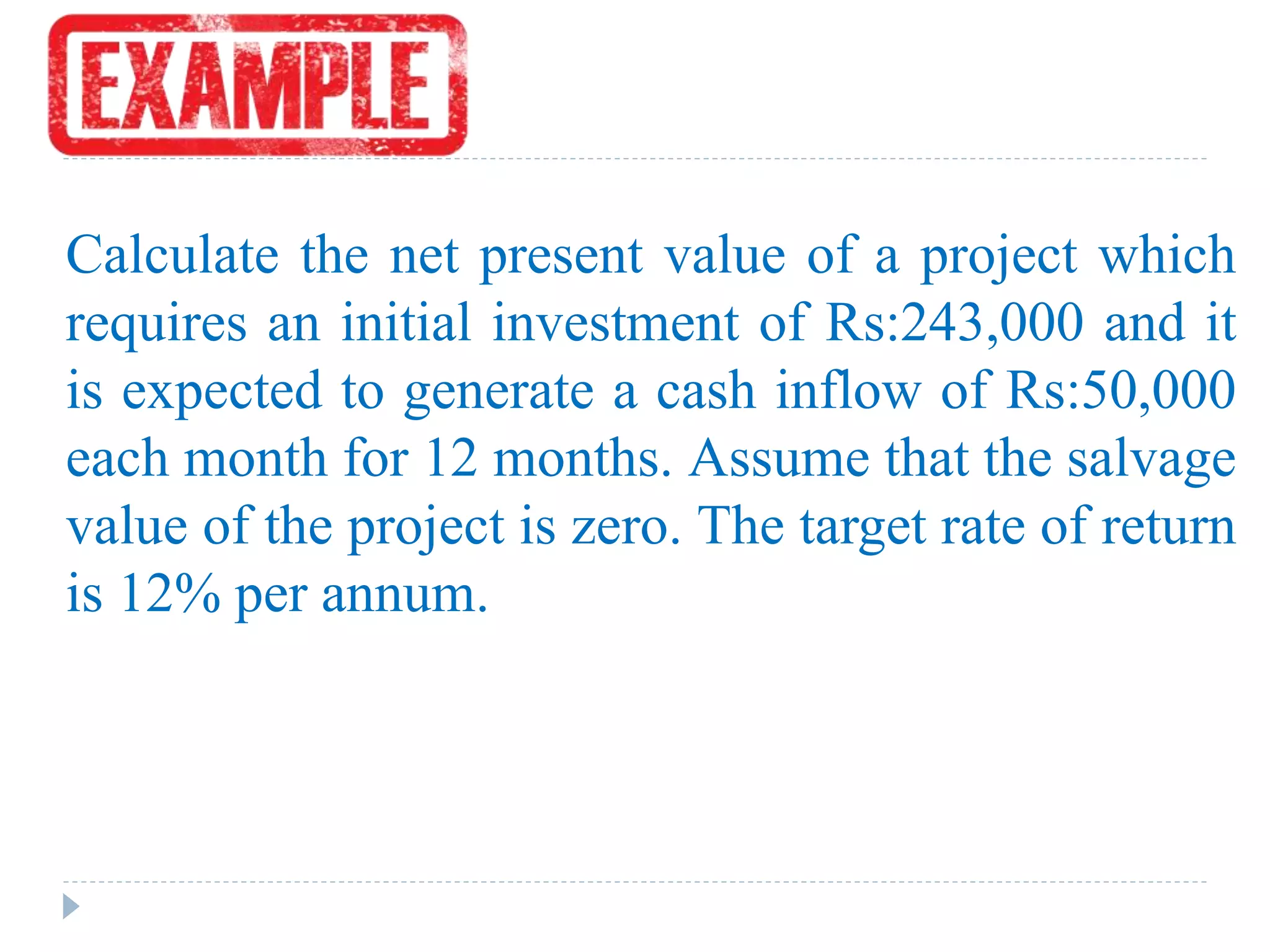

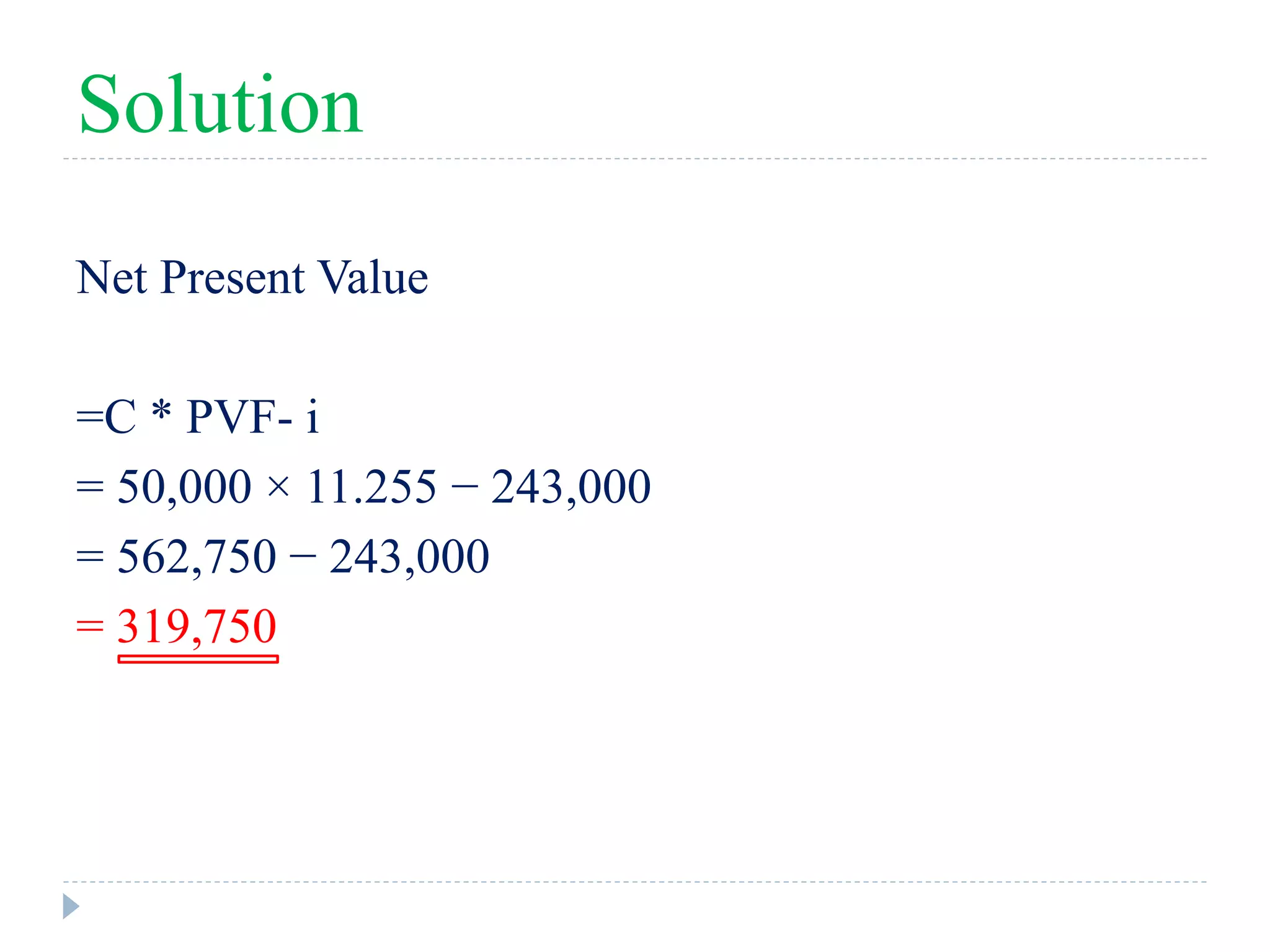

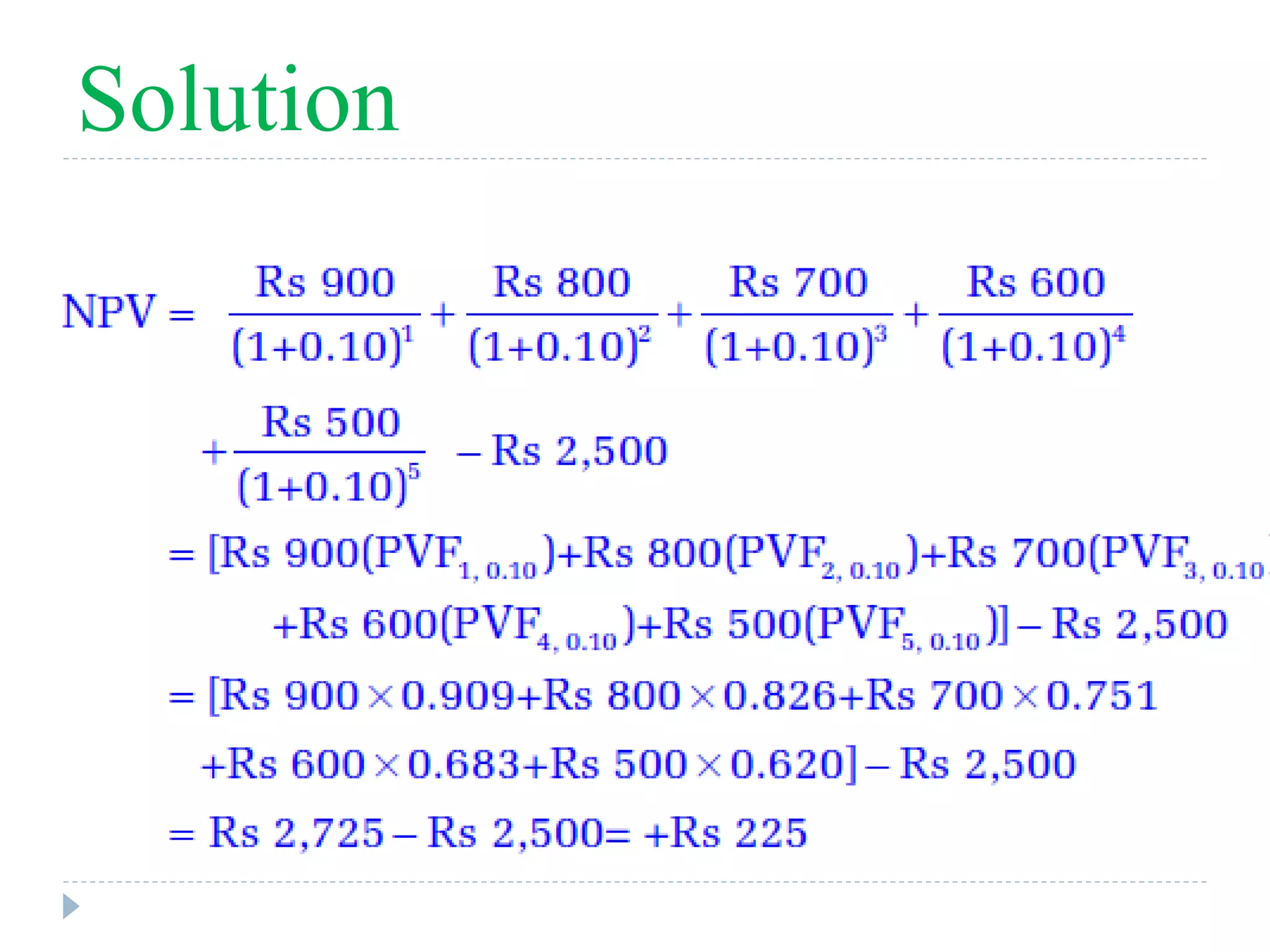

The document discusses capital budgeting methods, focusing on the net present value (NPV) method. It provides details on calculating NPV, including the formulas and acceptance rules. The key points are: 1) Capital budgeting is the process of evaluating long-term investments and NPV is a discounted cash flow method used. 2) With NPV, future cash flows of a project are discounted to give their present value, and the project's NPV is calculated as the present value of cash inflows minus the initial investment. 3) A project should be accepted if it has a positive NPV, as that means it is expected to increase shareholder value.